The Gladstone bag is a type of large, rigid-sided travel bag or suitcase, typically made of leather or fabric, with a distinctive design that features a wide opening and two handles. It is named after British Prime Minister William Ewart Gladstone, who was known for using such bags during his travels in the 19th century. The design often includes a frame that allows the bag to open widely, making it easy to access the contents. Gladstone bags were popular in the Victorian era and are often associated with traditional travel and formal occasions.

Fiscal Strategy to Promote Green Logistics and Boost Tax Revenues: A $8.5 Million Tax Revenue Gain through Carbon Credits

In this draft paper, we’re going to explore a fiscal policy measure designed to promote a carbon-free logistics industry while maintaining fiscal discipline. Through sampling a $100Mln Zero-Coupon bond issuance at par, with a 3Y Duration, parametrised to a tax credit mechanism for green deliveries, it is projected that the government can achieve a surplus of $8.5 million over a three-year period. This strategy encourages logistics firms to offer a 20% discount on green deliveries and accumulate carbon credits, which are offset against corporate tax liabilities. The policy framework balances environmental objectives with fiscal sustainability.

The wider global supply chain and transportation industry have been facing rising costs due to fossil fuel price increases and geopolitical risks, meanwhile, the transportation market still exhibits an idiosyncratic mismatch of economic value between fossil fuel economic value transportation vis a vis renewable and EVs transportation vehicles which economic added value still is underpriced in markets. In this paper, the aim is to raise to parity the economic added value of logistics firms that provide EVs and zero-carbon footprint transportation, compared to traditional modes of transport based on diesel and other fossil fuel petrol vehicles, which convey inherent higher operational costs due to fossil fuel emission compliance rather than economic added value, and this extra-layer cost of running transportation on diesel fuel still is passed on to consumers as higher prices for logistics services, without generating added economic value, rather generating an economic disvalue, technically negative externalities, in proportion to environment pollution and adverse health-related outcomes for the wider population.

In order to provide an answer to the transportation market mismatch in pricing fossil fuel transportation costs compared to renewable energy and EV transportation, a strategy has been developed in terms of a balanced fiscal tool, with neutral weight on fiscal budgets, in order to incentivise greener logistics operations, accustom consumer behaviour in choosing greener and sustainable logistics supply-chain services such as EVs and Bicycle-powered last mile deliveries, rather than diesel van and petrol car transportation: first by filling the pricing gap mismatch between EVs and Bycicle powered delivery services compared to diesel-powered vehicle delivery prices, to then structure a tailored Fiscal incentive measure termed Carbon Credit, structured through the issuance of short-term 3Y Zero Coupon Bond, issued at par, that the Government can allocate to Transportation and logistics firms operating only with EVs and Bycicle-powered vehicles, within the form of Carbon Tax Credit compensation for Businesses Taxable Revenues. The measure should be aimed to provide liquidity to logistics and transportation firms, through the instrument of Zero-Coupon Bond issuance, utilized as a 20% discount, Carbon Credit offset, for Transportation and logistic services retail prices, made with EV and Bycicle powered vehicles with zero-carbon footprint pollution, in order to incentivise consumers to choose in the market the Greener option of delivery service, rather than the polluting diesel or motorbike van service, while a 20% Discount, Carbon Credit Offset, can be offered by Transportation and Logistics services businesses, financed through the form of Carbon Tax Credit. On this Fiscal measure, a preliminary study assessment has been performed to evaluate the Fiscal Budget cost/benefit to the Treasury Public Debt and to the economy’s GDP in terms of investment multiplier, providing thereof confidence that if the Fiscal tool is structured with the proper parameters could actually produce Tax Revenue gains, and generate a GDP multiplier on the investment, that could vary according to specific country, although the GDP multiplier on such fiscal measure could result to be at least 1.5 up to 3 in optimal conditions.

Mechanism of the Fiscal Strategy:

Bond Issuance:

- Three-Year Zero Coupon Bond at Par (100): The government issues a zero-coupon bond at par to raise $100 million, repaid at maturity with no interest but at par value.

- Bond Usage: The $100 million raised will serve as the basis for offering carbon credits to logistics firms, incentivizing them to price deliveries using electric vehicles and bike messengers competitively with diesel deliveries.

Customer Incentive:

- By offering a 20% discount on green deliveries, customers are more likely to choose eco-friendly options, leading to higher adoption of green logistics.

- Diesel deliveries remain more expensive, driving customer preference toward bike messenger and electric vehicle deliveries.

Tax Credit Mechanism:

- 20% Carbon Credit: Firms provide a 20% discount on delivery prices for green deliveries. The carbon credit accumulates for firms to offset their corporate tax liabilities, effectively lowering their corporate tax from 25% to 5% on green delivery revenues.

- Tax Credit vs. Refund: Unlike a tax refund, this credit lowers the effective tax rate, simplifying government expenditures while providing a fiscal incentive to logistics firms.

VAT and Multiplier Effects:

- VAT is still collected on all transactions (diesel or green deliveries), contributing to the government’s revenues.

- The investment multiplier from increased green logistics adoption stimulates broader economic activity, resulting in increased VAT and corporate tax revenues.

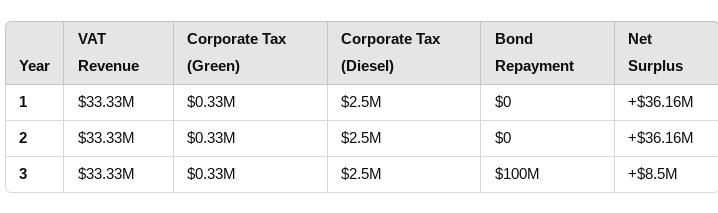

Revenue Projections:

Total Revenue from Economic Activity:

- Assume $500 million in total economic activity, with a standard 20% VAT applied.

- Projected VAT Revenue: V.A.T=0.20×500Mln=100Mln V.A.T = 0.20 \times 500Mln = 100Mln V.A.T.

Corporate Tax Revenue:

- From $50 million in total taxable income:

- Green Deliveries (40%, or $20 million), taxed at an effective 5%: CorporateTax(Green)=0.05×20Mln=1Mln Corporate Tax (Green) = 0.05 \times 20Mln = 1Mln CorporateTax(Green)

- Diesel Deliveries (60%, or $30 million), taxed at the standard 25%: CorporateTax(Diesel)=0.25×30Mln=7.5MlnCorporate Tax (Diesel)

- Total Corporate Tax Revenue: CorporateTax=7.5Mln+1Mln=8.5Mln Corporate Tax = 7.5Mln + 1Mln = 8.5Mln CorporateTax=7.5Mln+1Mln=8.5Mln

Bond Repayment:

- Repayment Obligation: $100 million after three years (par value). This is funded through VAT and corporate tax revenues.

Net Fiscal Outcome:

- Total Revenue: TotalRevenue=VAT(100M)+CorporateTax(8.5Mln)= 108.5Mln Total Revenue

- Bond Repayment: BondRepayment= Zero-Coupon 100Mln Bond Repayment

- Net Fiscal Surplus: NetFiscalSurplus=108.5Mln−100Mln=+8.5Mln Net Fiscal Surplus

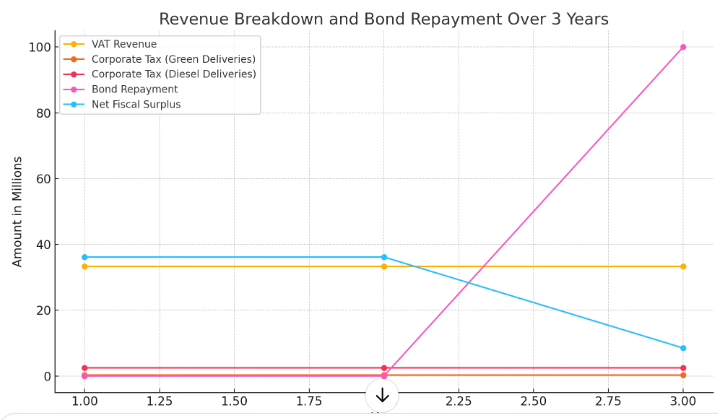

VAT Revenue: Consistently generated from economic activity.Corporate Tax on Green Deliveries: Reflecting the reduced corporate tax rate (5%).Corporate Tax on Diesel Deliveries: Higher due to the standard 25% corporate tax rate.Bond Repayment: Occurs fully in the third year. Fiscal Surplus: Generated over the three-year period, with a surplus of $8.5 million in the final year.

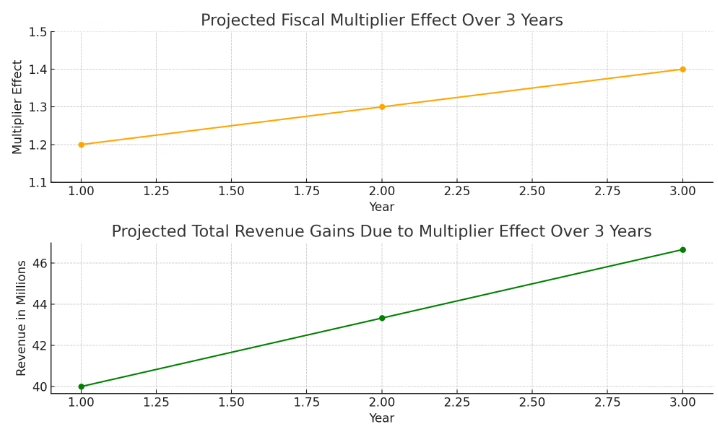

Projected Fiscal Multiplier Effect Over 3 Years: This graph shows the assumed fiscal multiplier for each year, reflecting how initial investments can lead to greater overall economic activity.

Projected Total Revenue Gains Due to Multiplier Effect: This graph illustrates the projected revenue gains based on the VAT revenue and the fiscal multiplier effect over the three years.

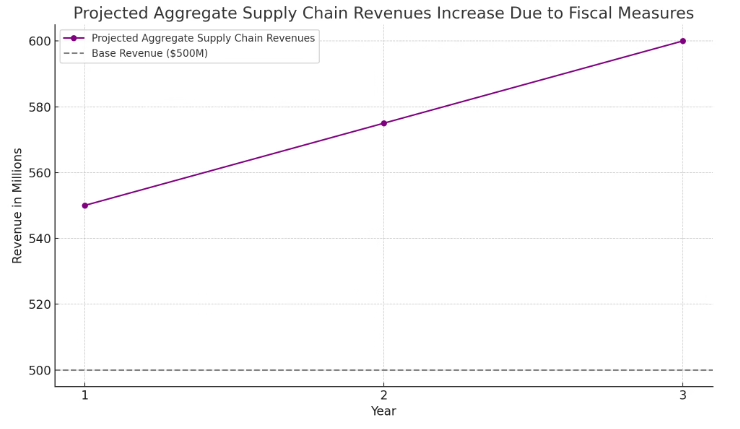

Projected Aggregate Supply Chain Revenues Increase Due to Fiscal Measures:

- The purple line represents the projected revenues over three years, considering the assumed percentage increases due to the fiscal measures implemented.

- The dashed grey line indicates the base revenue of $500 million for comparison

The multiplier effect for the logistics industry can vary based on various factors, including economic conditions, infrastructure investments, and overall demand for logistics services. While specific multipliers can differ, estimates for the logistics sector in the UK are generally around 1.5 to 2.0. Here are some insights:

- Research Studies: Some studies have suggested that for every £1 invested in logistics, there could be an economic return of approximately £1.50 to £2.00. This is due to the sector’s role in supporting other industries by facilitating trade and commerce.

- Government Reports: The UK government often provides data and analysis regarding the logistics industry, which sometimes includes estimates of the economic impact and multiplier effects. For example, the Department for Transport has noted that improvements in logistics efficiency can lead to broader economic benefits across various sectors.

- Sector-Specific Reports: Industry reports, such as those from the Logistics UK and other trade associations, frequently highlight the economic contribution of logistics, noting how investments in this sector can lead to job creation and enhanced productivity in the economy.

- General Economic Multipliers: In broader terms, multipliers for transportation and logistics can range from 1.5 to 3.0, depending on the context of the analysis.

Subscribe to our newsletter!

[newsletter_form type=”minimal”]

Read More:

https://www.sciencedirect.com/science/article/abs/pii/S0959652623018358

https://www.emerald.com/insight/content/doi/10.1108/IJCCSM-11-2019-0066/full/html

https://www.ieta.org/wp-content/uploads/2024/04/IETA_VCM-Guidelines.WEB-2.pdf

https://www.unep.org/topics/climate-action/climate-finance/carbon-markets

https://en.wikipedia.org/wiki/Carbon_offsets_and_credits