The question of how governments should deploy fiscal tools to stimulate economic growth or address crises has long been debated. Among the arsenal of fiscal policies, government wage shocks—significant increases in public sector wages—stand out as one of the least effective tools in the long term. While these measures may initially raise disposable incomes and improve short-term consumption, they risk becoming a fiscal trap. In the long run, they often lead to higher debt burdens without contributing meaningfully to potential output, undermining fiscal sustainability and economic stability.

What Are Government Wage Shocks?

Although these become a persistent feature in periods of high inflation, Government wage shocks involve increases in average public sector wages or significant expansion in nominal government compensation. Unlike other fiscal tools such as government purchases or public investment, wage shocks directly raise the nominal incomes of public sector workers without necessarily contributing to real government consumption or the productive capacity of the economy: also the rise of Government wages has very small disposable income effect when considered the direct Tax intake from the Government itself and especially when a Government wage impulse is accompanied by an Employer Tax increase. In this context, raising public sector wages directly increases nominal compensation but doesn’t expand the aggregate supply of Public sector services or investments to improve total factor productivity. On the other hand, it has been empirically determined that increasing Government Employment has a more direct effect on consumption and output.

What could be the short-term Benefits of a Government wage shock fiscal tool:

Disposable incomes for public sector workers and employee increases allow in part, net of direct tax intake, a boost to private consumption and eventually savings. In this vein, Tax Revenues could see a modest increase as higher wages result in higher income tax collections. The partial uplift in disposable income resulting in stimulated additional aggregate demand does generate inflationary pressure also considering the slightly higher unit labour costs, either because of Government wage shocks, or Employer Tax increases.

Medium-to-Long Term outcomes of Fiscal policy framework

However, these initial gains are deceptive. Over time, the structural weaknesses of government wage shocks become apparent, as highlighted in macroeconomic analyses like the ECB-BASE model: Minimal Impact on Potential Output: Unlike public investment, which enhances capital stock, wage shocks do not increase the economy’s productive capacity. They fail to stimulate innovation, productivity, or infrastructure development, all critical components of long-term economic growth. Real government consumption remains largely unchanged, meaning the fiscal expansion does little to improve public services or infrastructure.

Erosion of Disposable Income Gains:

Rising wages initially boost disposable income, but higher inflation driven by wage growth erodes these gains over time. As the cost of living increases, any real-term benefits to households diminish, limiting the impact on private consumption. Higher Unit Labor Costs and Reduced Competitiveness: Elevated public sector wages can spill over into the private sector, raising overall unit labor costs. This undermines the international competitiveness of domestic industries, potentially depressing exports and economic growth. A Growing Debt Burden: The most significant long-term consequence is the effect on public finances. Higher public sector wages contribute to persistent budget deficits without generating the additional tax revenues or economic growth needed to offset them. Over time, this dynamic leads to an escalating debt-to-GDP ratio, straining public finances and limiting the government’s capacity to respond to future crises.

Evidence from Fiscal Models

Empirical studies and models like the ECB-BASE reinforce these conclusions. A fiscal expansion equivalent to 1% of GDP through wage shocks typically requires a substantial increase in public sector wages—nearly 10% in some cases. However, the economic gains from such an expansion are fleeting. Rising nominal compensation has limited positive effects on real disposable income, as inflation and higher unit labor costs quickly offset the initial boost. Meanwhile, public debt rises steadily, as governments must finance the wage increase without reaping significant economic returns In contrast, fiscal tools like public investment or government purchases demonstrate far greater efficiency. These tools not only boost short-term demand but also enhance the economy’s productive capacity, contributing to sustained economic growth and improving the fiscal balance over the long term.

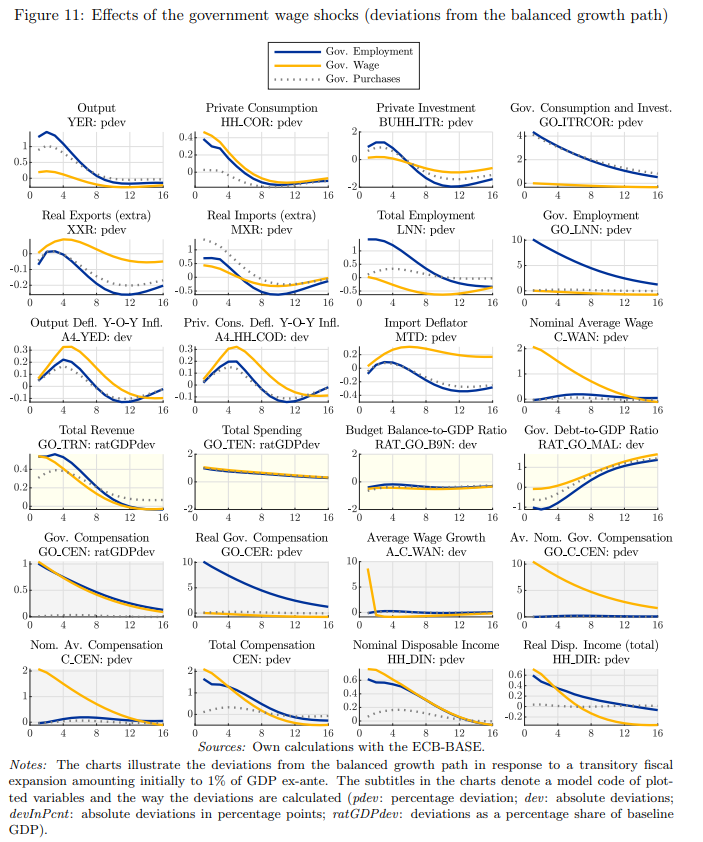

These charts illustrate the impulse response function of government employment, government wage (yellow line), government purchases, and government investment, based on deviations from a balanced growth path after a fiscal expansion of 1% of GDP. Empirical findings demonstrate that public sector wage shocks have minimal positive effect on output that declines in the following quarters. Instead, Government Investment empirically proves to have the strongest and most persistent effects, determining improvements both in short-term demand and long-term productive capacity, indeed, proving pillar Keynesian concepts that Investments become the profits and wages of other entrepreneurs and workers, which then should also be utilised for investment, rather than consumption, in a virtuous economic cycle.

Observing charts in the top row, Government Wage Shock in fact doesn’t generate necessary private investment

Wage Shock: Limited increase in private consumption due to higher disposable income from nominal wage increases, but this is offset by inflation. Private investment does not improve significantly. Comparison: Employment shocks stimulate both consumption and investment more effectively than wage shocks. Investment and purchases provide more robust and sustained increases in private consumption and investment due to broader economic benefits.

In terms of additional employment (Second Row, 3rd Chart)

Wage Shock: No significant increase in employment, as wage adjustments do not involve hiring more workers.Comparison: Employment shocks directly increase the number of government jobs, significantly boosting total employment. Investment and purchases also contribute to job creation through increased demand.

Inflation metrics side effects (Third Row, 1st and 2nd Charts)

Government wage shock (amber line) can be conducive to additional inflationary pressures and inflation increases due to short-term impulse in aggregate demand and consumption, while also government wage shock can be inflationary considering the higher unit labor cost.

Debt-to-GDP Ratio and Budget Balance (Bottom Row, 2nd and 3rd Charts)

Wage Shock: Results in a substantial and persistent increase in the debt-to-GDP ratio because the wage increase does not improve output or the potential capacity to generate tax revenue.

Government Wage Shock (Amber):

Offers minimal economic benefits. Its limited output impact is quickly eroded by inflation and rising labor costs. Government wage shocks are the least effective form of fiscal expansion among the four categories in terms of promoting economic growth and sustainability, highlighting their limited usefulness in driving long-term economic improvements, resulting in a significant fiscal burden with long-term increases in the debt-to-GDP ratio. The findings underscore the need for caution when considering government wage shocks as a fiscal policy tool. While politically expedient, such measures are fiscally unsustainable and economically inefficient in the long term. Policymakers should instead focus on: Public investment, which strengthens infrastructure, education, and technological capacity. Targeted transfers to low-income households, which have higher marginal propensities to consume and can stimulate demand without creating long-term fiscal liabilities. Structural reforms enhance productivity and competitiveness, ensuring that wage growth aligns with economic fundamentals. Governments must resist the temptation to prioritize short-term gains over long-term sustainability. Wage shocks, while appealing at the moment, ultimately burden future generations with higher debt and slower growth.