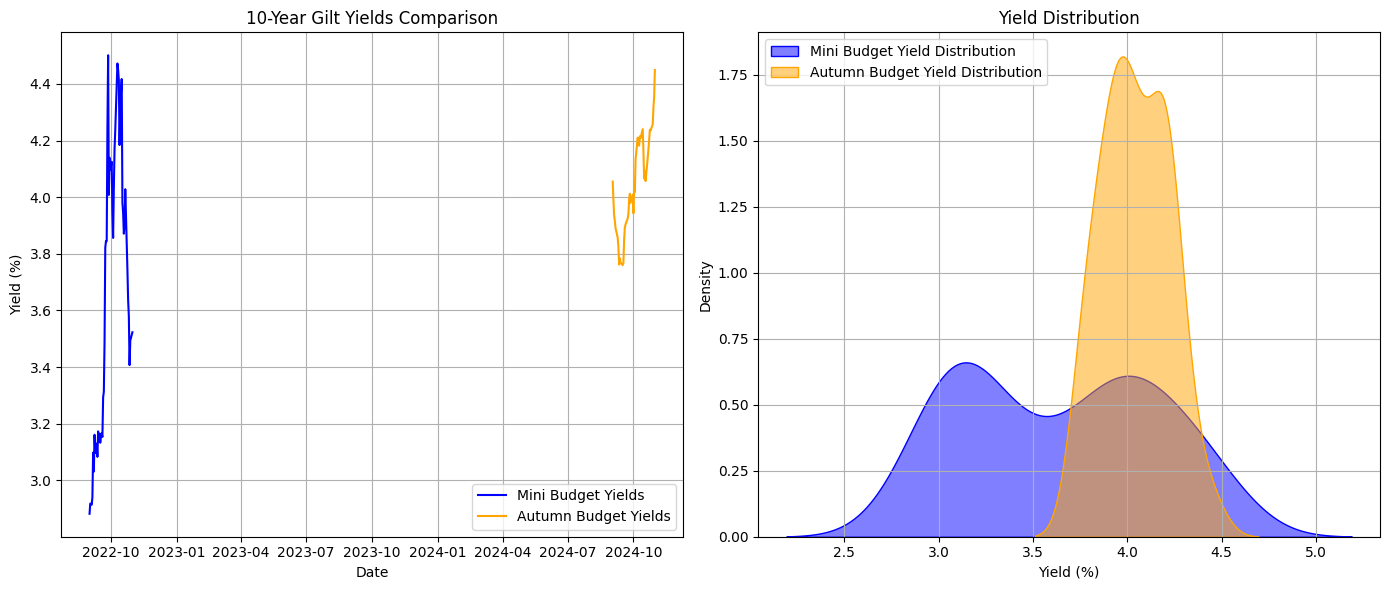

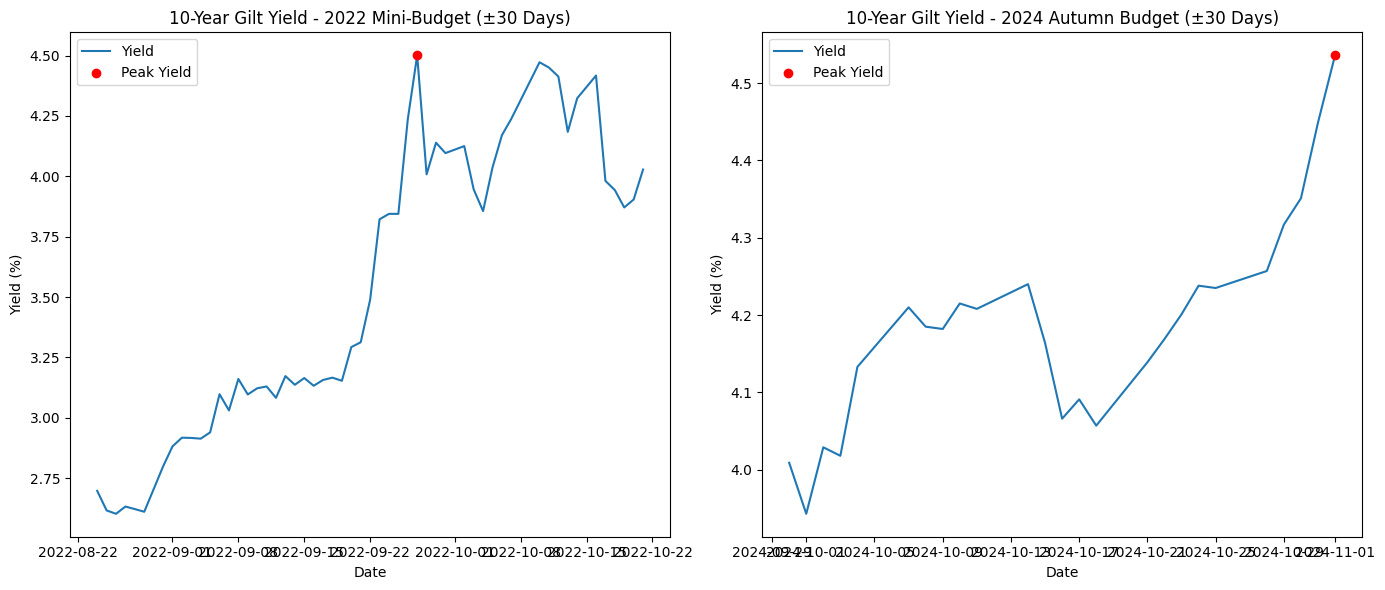

From a technical standpoint, the bond market reaction function to the Autumn Budget 2024 has been similar to the mini-budget 2022, indeed making the 10Y GILT yield increase to 4.54% above the 2022 of 4.32%, while the scale of change comparing both fiscal announcements saw a larger increase in yields for the 2022 budget, considering the GILT yield curve started to steepen from a lower basis. The facts and data to take into consideration are the repeated high volatility approaching UK Fiscal policy decisions and Fiscal deficit announcements, mechanically these are volatility risk factors and patterns that are repeating as a mechanical GILT Market signal of distress and Institutional investor concerns. Nevertheless, this idiosyncratic interest rate volatility risk of the GILT yield curve is a determinant factor for UK public finance, while the underlying structural issue in the UK’s debt stock hasn’t been confronted. The structural weaknesses of outstanding UK public debt in issue sits in a remote closet called INDEX-LINKED GILTS, a bad idea initiated by the oncoming 2010 Conservative Government that has accrued a total outstanding amount in issue of £387.43 Billion Pound (nominal amount) that has become Inflated with the Inflation Index Linked Uplift Premium to an amount of £615.84 Billion setting the UK Exchequer with a (£228.417 Billion Pound) funding need to service only a portion of the overall UK public debt, while the Inflation-Indexed-Link premium has inflated 59% on top of the total nominal amount of GILT in issue, and the UK Inflation measure is directly entangled with the Housing Price Index part of the overall RPI Inflation Index on which are based the premium uplift of Index-Linked-GILT, in a vicious loophole where constantly inflating Housing Market prices will continue to produce Inflationary pressure on the overall RPI Inflation Index and thereby sustaining the broadening cost of Index-Linked-GILT Inflation Premium to the Exchequer and to taxpayers. This underlying structural issue to sort out in the outstanding UK stock of GILT in issue does make any Fiscal policy budget a very difficult moment, in fact, Sovereign Debt Market Institutional Investors do sell off UK GILT when the Exchequer announces additional borrowing on top of what could be already a very difficult fiscal position in the medium to long term and this causes concerns to Institutional Investors about the ability of the UK to fund their future Public Debt liabilities, while more debt gets issued. Thereby, Debt Markets and Institutional Investors are concerned about the sustainability in the medium to long term of the UK Public Debt, considering that the country could have to be forced into larger public spending cuts and recession, in the future, to balance the additional spending, or that the Fiscal position could become unsustainable and the IMF could have to step in.

Could GILT Yields continue to Increase and drift higher?

The recent Halloween GILT Market volatility in the aftermath of the 2024 Autumn budget announced by the Exchequer, has been reminiscent of the 2022 UK mini-budget another important stepping stone of the UK Fiscal policy instability and unsustainability.

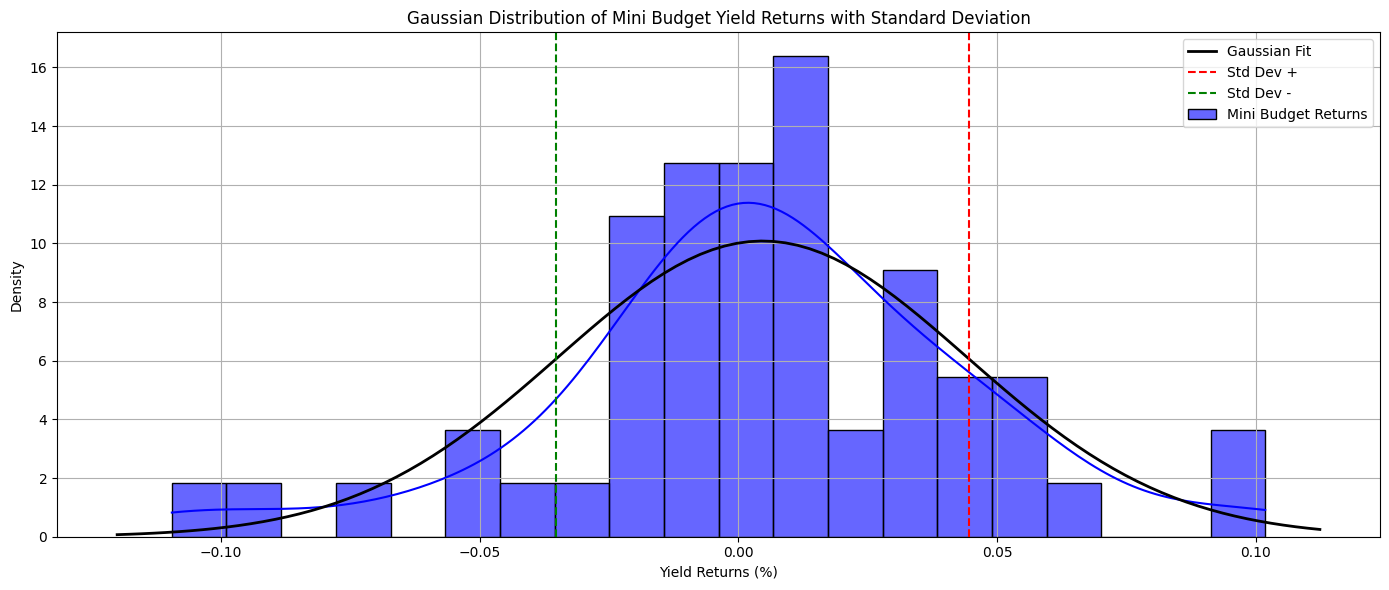

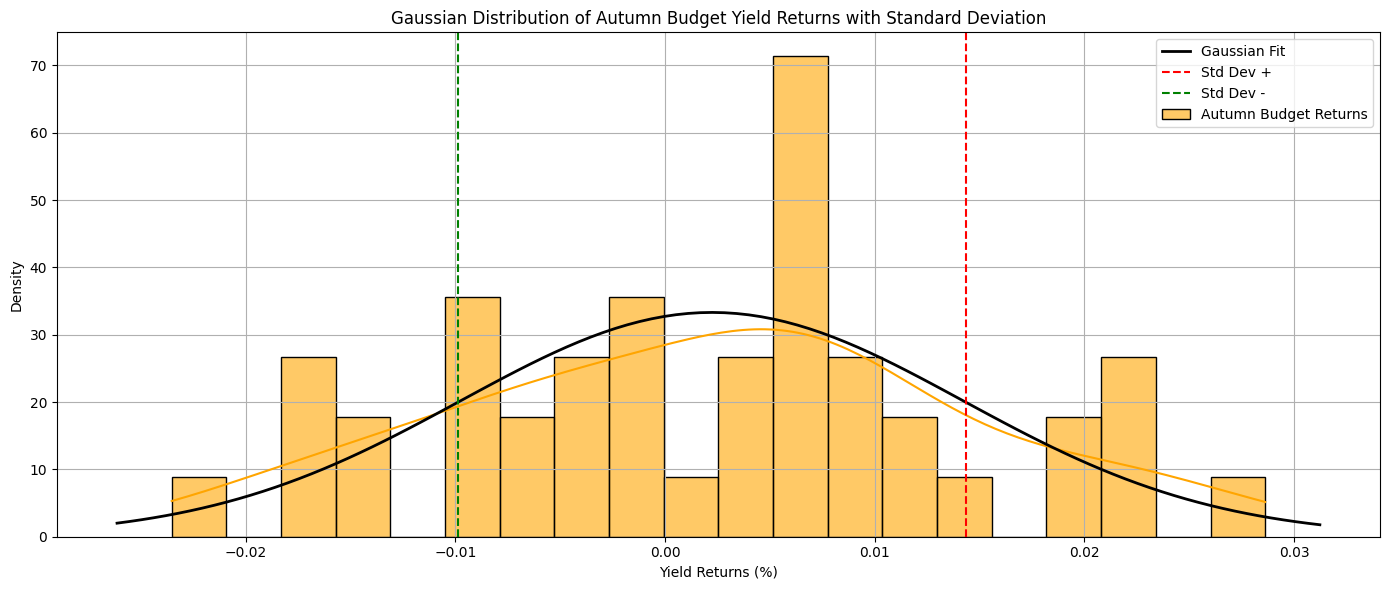

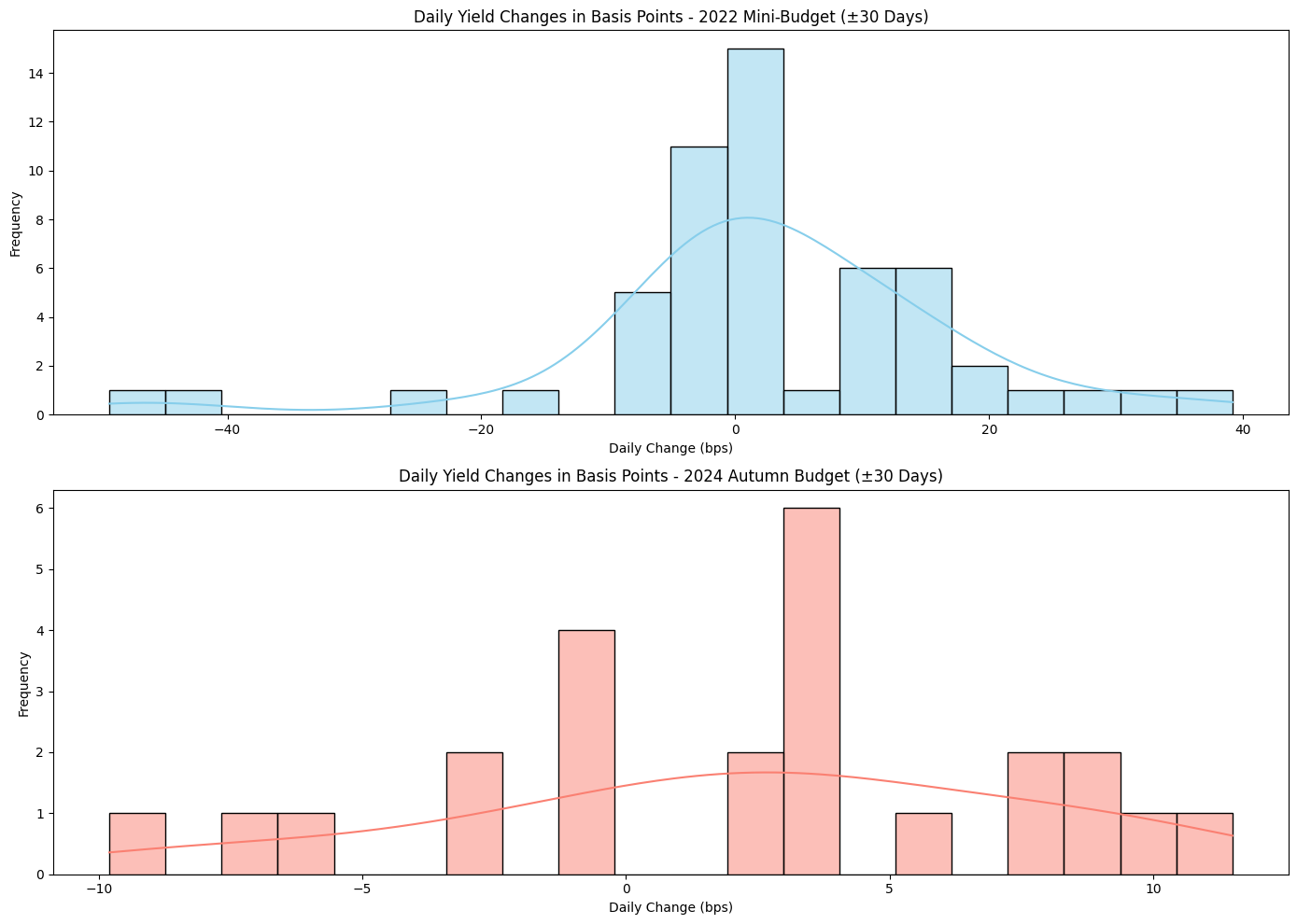

In this chart have been elaborated the histogram of Basis Points distribution changes comparing the 2022 mini-budget with the 2024 Autumn Budget, and we can observe that both display a Gaussian distribution, where the mini-budget chart highlights higher density in larger standard deviation moves while the 2024 Autumn Budget seems modestly skewed to the right side of the distribution. However, as of Halloween 31st October 2024, the 10Y GILT yield of 4.54% has closed above the mini-budget yield of 3.82% and above the mini-budget peak yield of 4.32% | 4.5%.

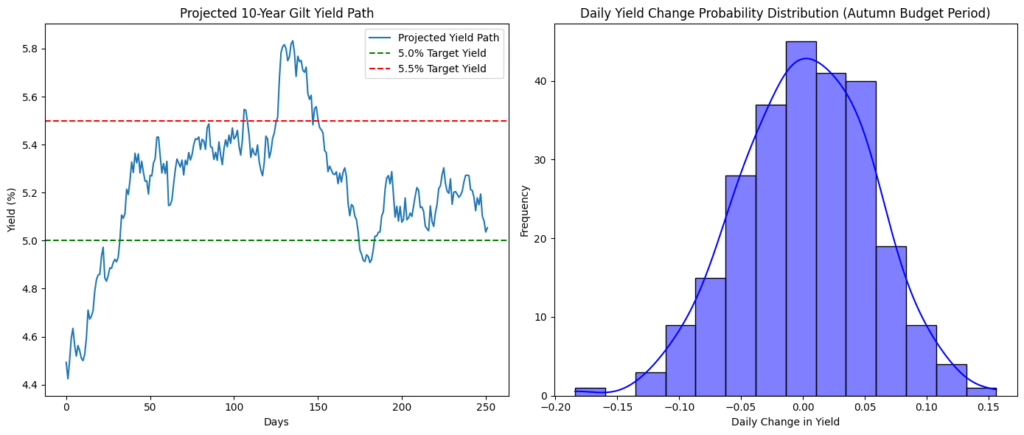

Probability Estimation techniques have been implemented to estimate the risk of rising yields

Probability test techniques have been utilised to estimate the likelihood of GILT Yield increases, in this case only the 10Y GILT Yield time series has been analysed to estimate a scenario of sustained volatility due to interest rate risk and Fiscal deficits. In the first instance, a simple Historical Volatility method has been implemented to estimate the probability of the 10Y GILT Yield rising to 5% and 5.5%, as a scenario forecast analysis. The results have been consistent with the framework highlighting a 30% Probability of the Yield reaching 5% within 1 year and a 14% Probability of the Yield reaching 5,5% within 1 Year. The graphical forecast of a higher yield volatility scenario and the probability distribution of outcomes have been derived incorporating also Autumn Budget volatility injected into the GILT market.

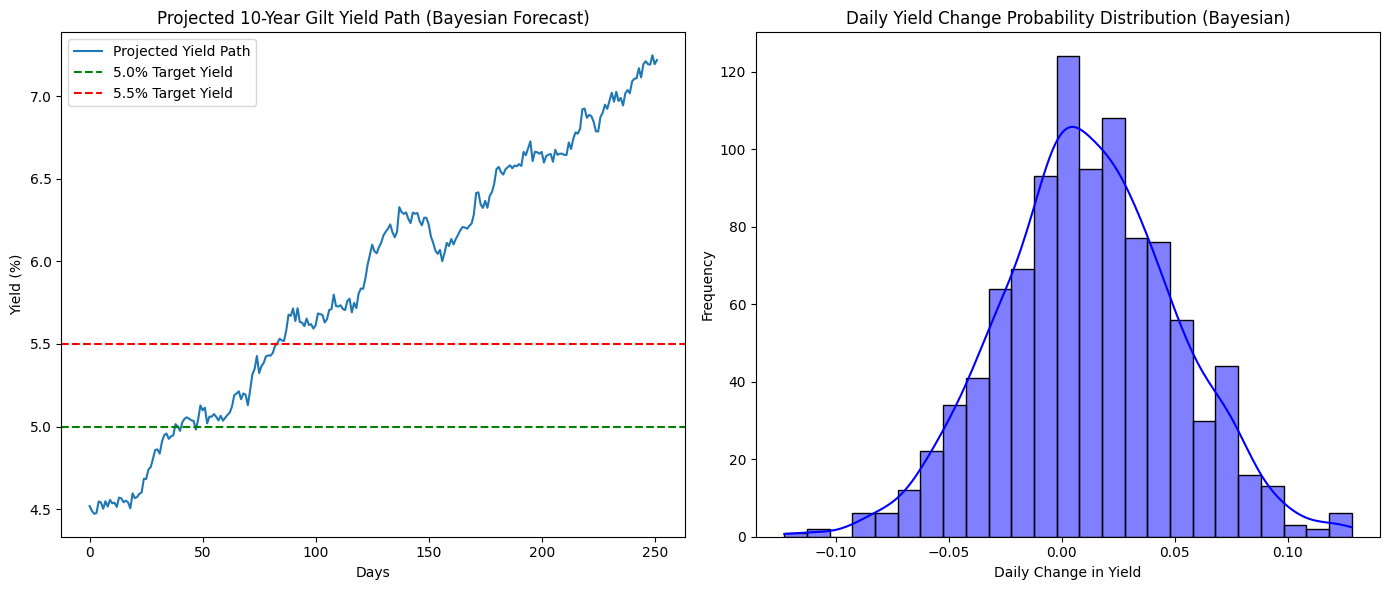

An additional Bayesian Inference method has been implemented to estimate the likelihood of rising yields and the statistical results have been quite interesting, in fact, the Posterior mean change per day= 0.017098, the Posterior Standard Deviation per Day = 0.03952, which resulted in a 99.9% Probability of Yield Reaching 5% and 99,8% Probability of Yield reaching 5.5%. Hence, the Bayesian Inference technique of estimating posterior distribution has assigned a very high probability scenario to the 10Y GILT Yield reaching 5% and even 5.5% in the next 12 months. Withstanding the high-probability scenario, the projected 10-year Gilt Yield path graph doesn’t seem to reflect a concrete market outcome.

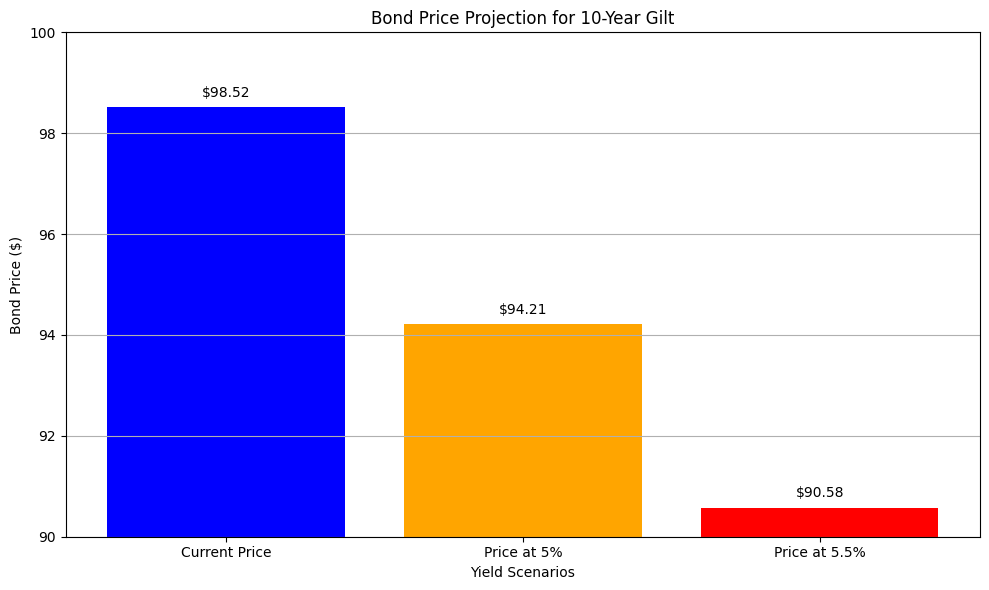

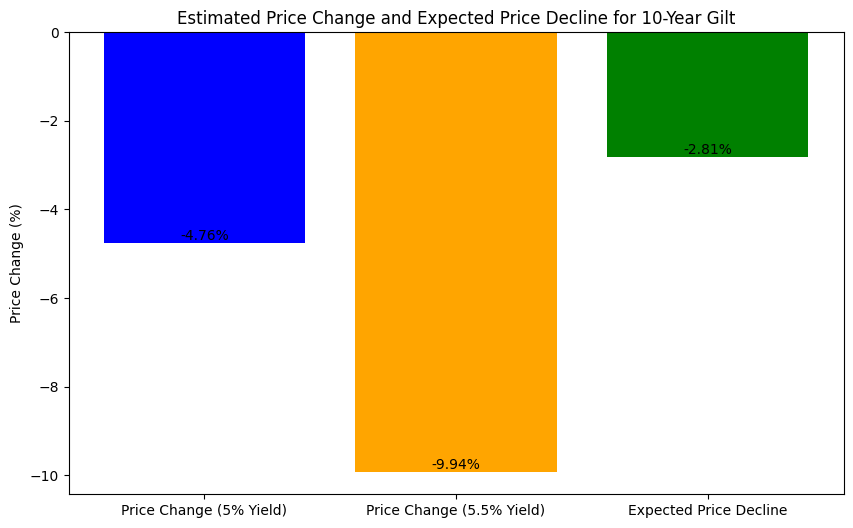

Furthermore, modified duration and price sensitivity estimation have been implemented to understand and forecast the implied change in price, whenever the 10Y GILT yield would increase to 5% and 5.5%. The data have been extracted from the most recent issuance. The calculations regarding present value (PV), future value (FV), modified duration, and price sensitivity underscore the significant impact of yield fluctuations on bond prices. The modified duration of 7.9760 years suggests that for every 1% change in yield, the bond’s price is expected to change by approximately 7.98%. This is a critical measure for understanding interest rate risk, as it quantifies the sensitivity of the bond’s price to changes in interest rates. In this context, a yield increase of 10 basis points (bps) is projected to decrease the bond’s price by approximately 0.7976%, resulting in a new price of $97.73. Conversely, if the yield decreases by 10 bps, the bond’s price is expected to rise to $99.31. These price sensitivity estimates demonstrate the bond’s reactive nature to yield changes, indicating that even small fluctuations in interest rates can lead to significant impacts on bond valuations. The projected new prices of the gilt securities in response to increases in yield reflect the significant impact of interest rate fluctuations on bond valuations. If the yield rises to 5%, the price is expected to adjust to $94.21, representing a notable decrease from the original price. This decline of approximately 4.76% illustrates the bond’s sensitivity to interest rate changes, as indicated by its modified duration of 10.35. Furthermore, should the yield increase further to 5.5%, the bond’s price would drop to $90.58, a more pronounced decrease of about 9.94%

Present Value (PV): $98.17 Future Value (FV): $100.00 Modified Duration: 7.9760 years Price Sensitivity to a 10 bps yield change: -0.7976% New Price if yield increases by 10 bps: $97.73 New Price if yield decreases by 10 bps: $99.31

New Price if yield increases to 5%: $94.21

New Price if yield increases to 5.5%: $90.58