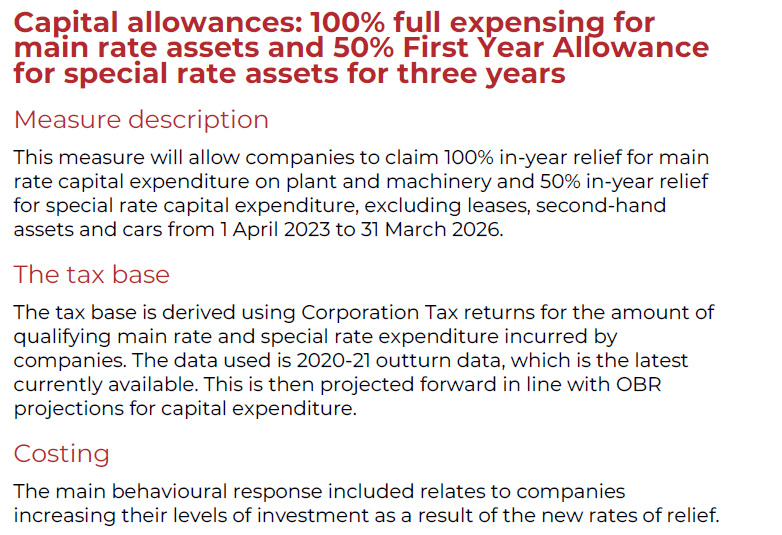

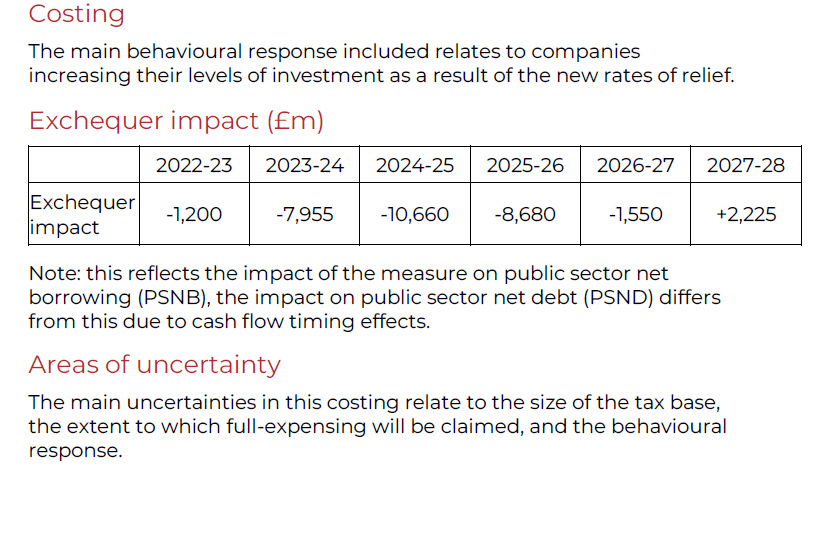

The big idea coming from the UK Exchequer Spring Budget, it’s a rough measure of Capex that won’t produce what’s hoped, but rather accounting tricks to inflate capex expenditure so as to evade the raise in Corporate Tax. The measure doesn’t consider a stagflationary economy and the credit constraints in the economy determined by the banking industry fallout, in other words, the global economy will be sleepwalking into a stagflationary recession where Capex will be shrinking if not very limited, the economic conjuncture wouldn’t see industries and SMEs having spare cash to spend on machinery and Capex investments, but rather it’s very probable to see Industries and SMEs starting to cut costs by laying off redundant personnel, already underway in Tech.

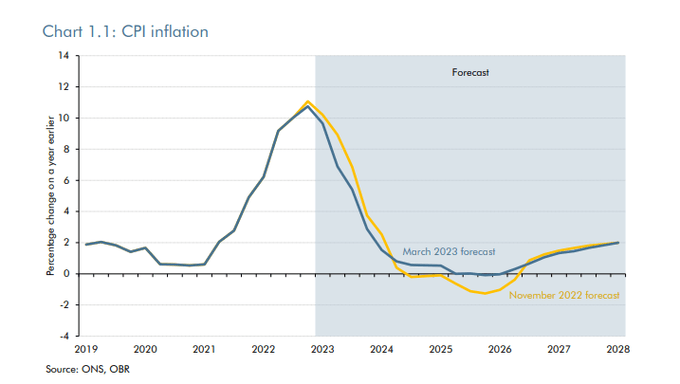

The slides indeed are a rough estimate of the feasible costs to the Exchequer in terms of Revenues, however, there’s nowhere to see the point estimates of the multiplier effect and economic growth estimates. Considering the UK Government takes as holy water the OBR CPI forecast of Inflation decreasing to 2.9% by Q4 2023, the graph it’s a simple standardized Gaussian statistical forecast. The Decrease from 12% CPI, 16.1% Food inflation to 2.9% on aggregate in the space of 12 months,such a rapid decrease in vertical fall in the rate of CPI Inflation does apply to RECESSIONARY ECONOMIC PERIODS. In other words, It’s very hard to see a 10% points decrease in Inflation in 12 months without a consistent ECONOMIC RECESSION AND CREDIT CONTRACTION.

During periods of Economic output contractions and Credit contractions, would be hard for any SMEs and large industries to figure out where, how, when, y and on what to invest, by acquiring machinery and doing CAPEX expenditure. Very simple: RECESSION= CUTTING COSTS, CREDIT SHRINKING, ECONOMIC UNCERTAINTY ECONOMIC EXPANSION= CREDIT ACCESS EASING, CAPEX INVESTMENTS, HIRING STAFF. Basically that simple. The UK Exchequer has made the basic mistake of presuming that a decrease in CPI Inflation from 12% to 2.9%, will be possible by also avoiding RECESSION. Never seen such a thing, maybe only in the UK. Anyhow, the headline UK CPI INFLATION METRIC by Q4 2023 will probably be higher than 2.9%, it’s almost sure that the OBR and the Government have assumed the wrong forecast. Time will tell. nobody’s perfect.

The rise in Corporate Tax to a 22.5%<CT<25% band scaled on gross revenues, could have been accompanied by a relative cut across the economy in V.A.T. to 17.5%, which would guarantee a deflating effect on retail prices. The reduction in V.A.T. to 17.5% would sustain consumption, The economy would benefit from a reduction in V.A.T., in particular with high Inflation, that would feed through SMEs and Corporates that could see volumes of sales modestly increase-> Revenues increase- cost of sales(17.5% V.A.T.)= slightly larger Operating Profit. the marginal propensity to invest derives from the ratio of the improvement in Income to the value of Investment. If SMEs and corporates know that Corporate Tax would increase to 22.5%, 25% depending on Gross Revenue thresholds, but V.A.T. decreases to 17.5%,that could be a “balanced” Fiscal approach to sustain aggregate demand and SMEs Revenues, during Recessionary economic periods. Of course, it wouldn’t be that simple and a decrease to 17,5% of V.A.T. would cost much more to the UK Exchequer Revenues. However, the consumption and multiplier effects in the economy would likely in part compensate for the reduction in Fiscal Revenues from indirect taxation on consumption. All considered, Stagflationary and Inflationary pressures in the economy are in part exogenous constraints determined by supply chain constraints and aggregate supply constraints. Thereby reducing V.A.T. can help aggregate demand, “decrease” prices, while SMEs could see smaller costs and pressure on their operating profit margins.

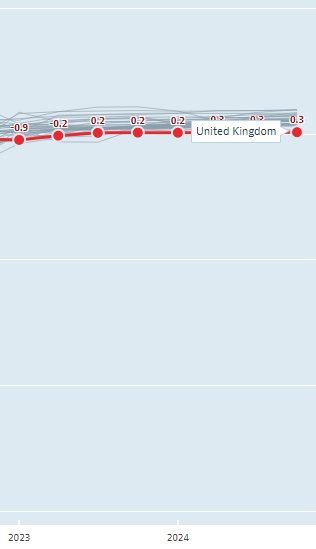

UK 2023 and 2024 forecast economic growth