In the quest for clues about how the global economy could perform in the coming quarters, additional econometrics research has been applied to some of the major macroeconomic United States variables. In this instance macroeconomic variables examined have been: Bank Prime Loan Rate, Consumer Loan Percentage Change, Core Inflation, Effective Federal Fund Rate, M1 Money Supply Percentage Change, PCE, Real PCE, Real Estate Loans Percentage Change, Unemployment Rate, all timeseries have been taken from 1970 up to date, considering the global shift to floating currencies market, in a format of month percentage change on the previous year.

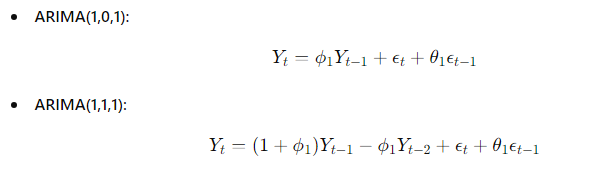

To examine the stationarity, autocorrelation of timeseries ARIMA(1,0,1) and ARIMA(1,1,1) have been applied to the macroeconomic variables, also to obtain 6 to 12 months plausible forecast output of macroeconomic variables. These macroeconomic variables have been chosen in this research in order to understand the probabilistic patterns of Money Supply, Bank Credit, Inflation, Unemployment and Interest Rate levels when intertwined. The forecast output was generated using an unconditional reference frame, which excludes the impact of any exogenous shocks or other variables that could potentially affect the time series predictions. This approach allows for a clearer understanding of the inherent trends and patterns within the macroeconomic variables under study.

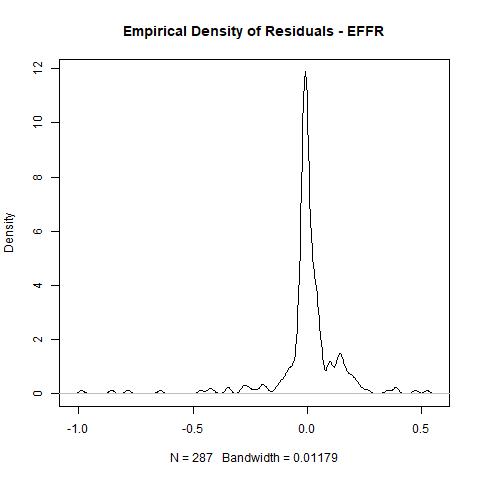

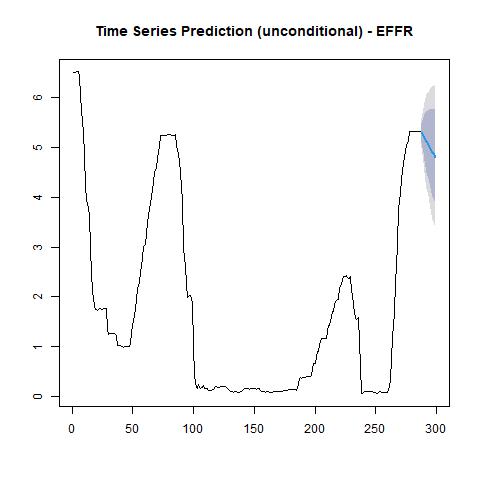

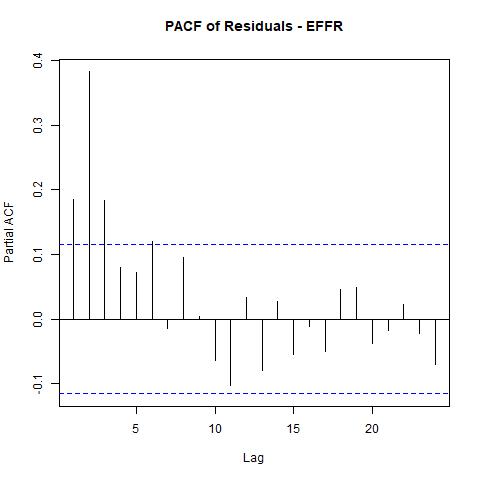

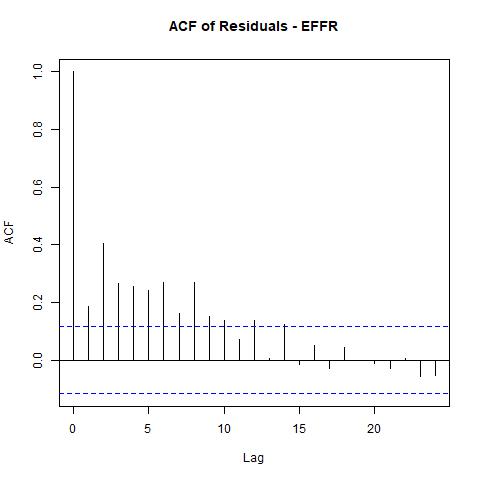

Examining the Effective Federal Fund Rate timeseries, we can see that the empirical density residual is centred very close to zero, indicating minimal bias, in the residual. Additionally, the PACF converges to stationarity more rapidly than ACF graphs, indicating a stronger indication of stationarity in the EFFR data. The unconditional forecast for the EFFR projects that the Federal Funds Rate is likely to decrease from its current level of 5.33%, but it is expected to remain above 4.25% over the next 6 to 12 months.

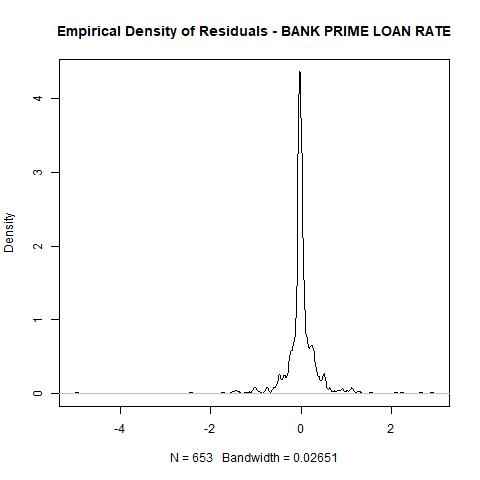

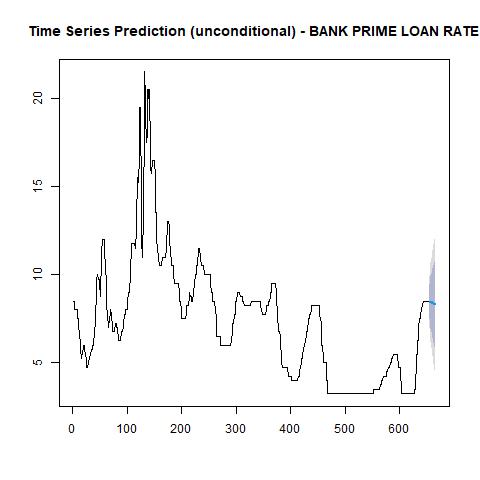

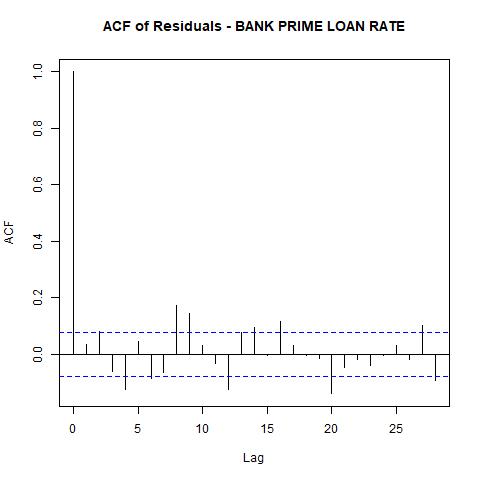

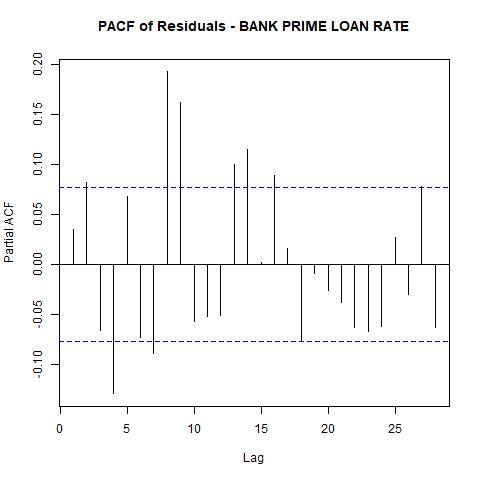

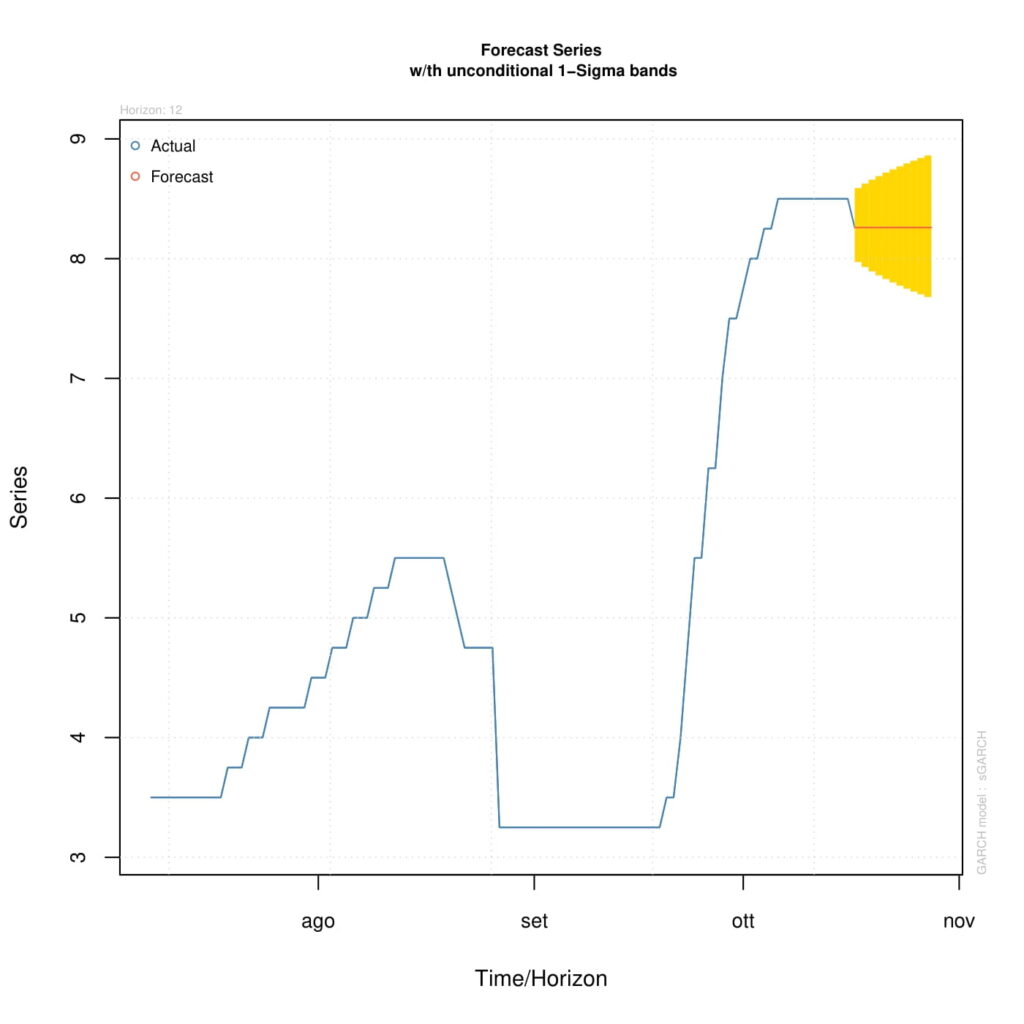

The average Prime Loan Rate of United States banks has recently been around 8.5%. In this research, we have observed a pattern in the Prime Loan Rate that evolves in line with the forecast for the Effective Federal Funds Rate (EFFR). The empirical density of the residuals is centred around zero, with a median of -0.92, suggesting minimal bias. Furthermore, the Autocorrelation Function (ACF) and Partial Autocorrelation Function (PACF) of the residuals indicate that the time series, once cleaned of residual errors, is stationary.

The unconditional forecast predicts a decline in the Bank Prime Loan Rate over the coming months, which is consistent with the anticipated decrease in the EFFR. This correlation underscores the interconnected nature of these key interest rates and supports the reliability of the forecasted trends.

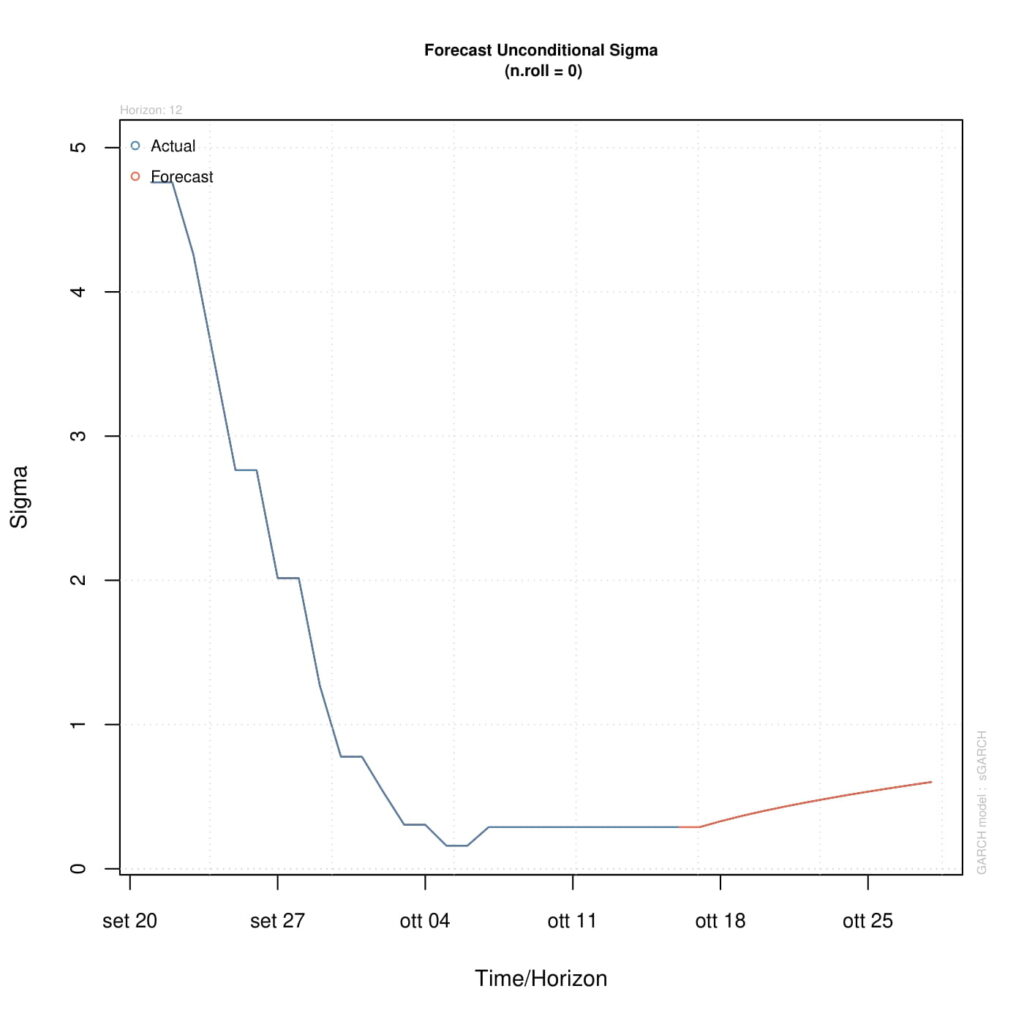

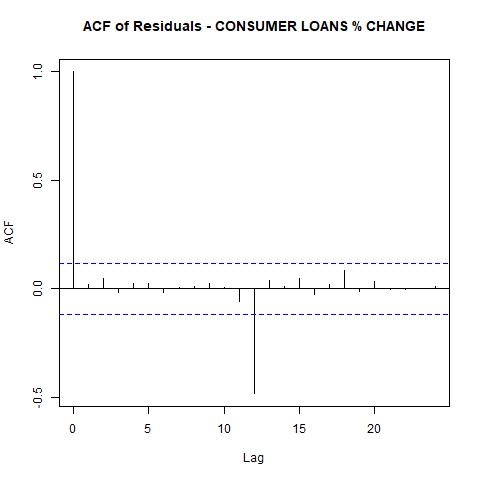

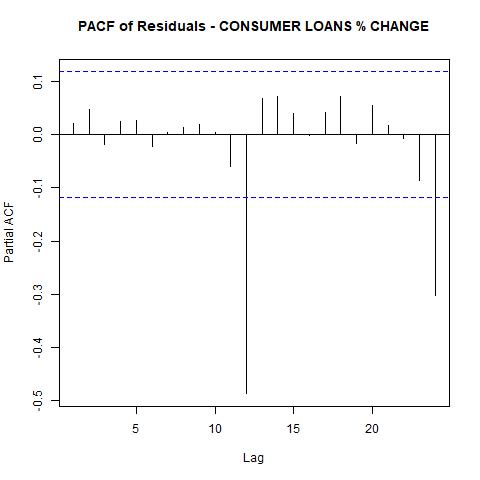

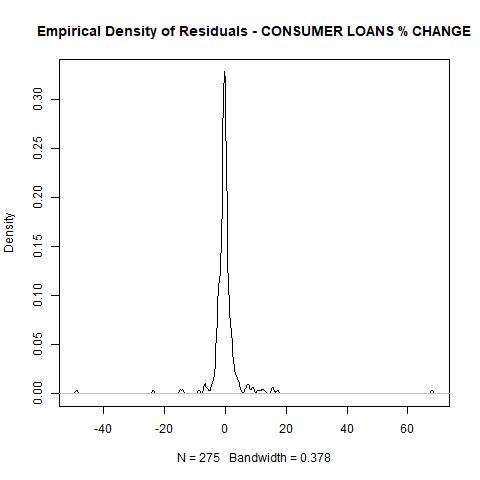

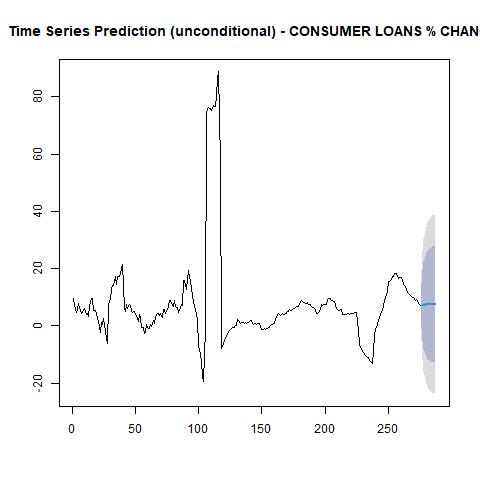

Upon examining the consumer loan trends, both the Autocorrelation Function (ACF) and Partial Autocorrelation Function (PACF) of the residuals suggest that the time series may be stationary. However, the PACF graph shows some significant spikes, which could indicate the presence of residual autocorrelation or other patterns not fully accounted for. Despite these anomalies, the unconditional forecast for the next 12 months suggests that there will be no significant change in consumer loan patterns. This implies that the model anticipates a continuation of the current trend without major deviations.

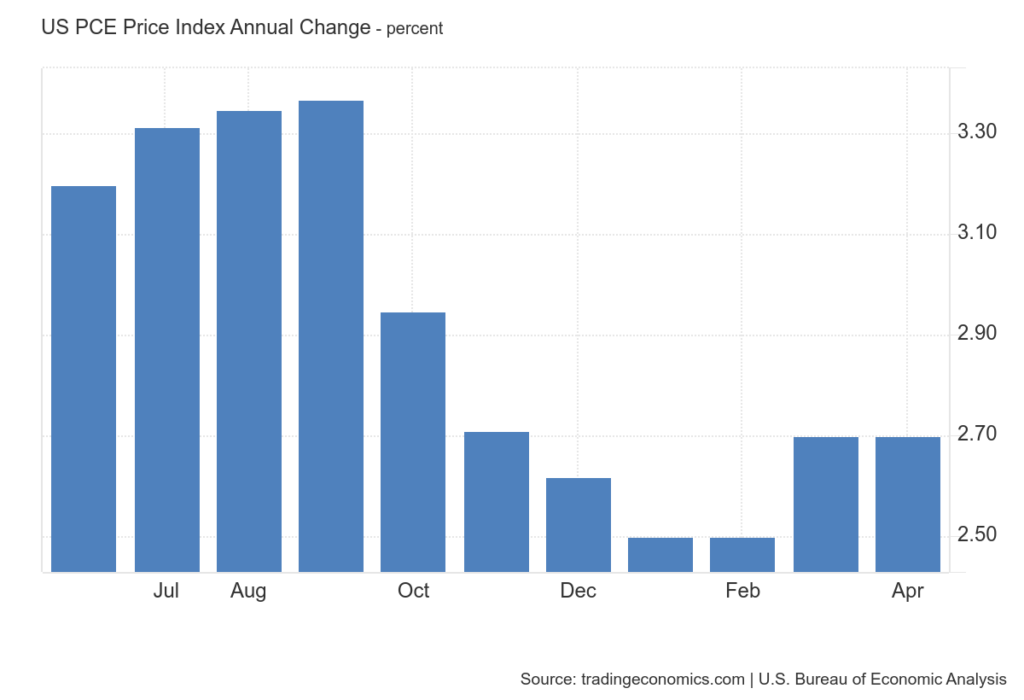

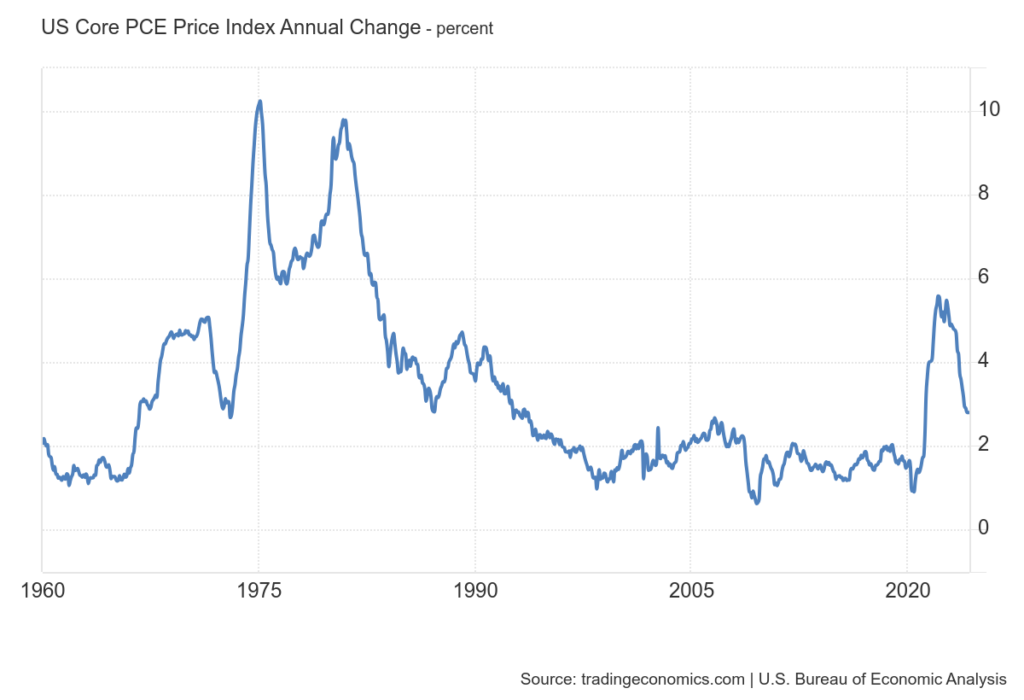

The annual PCE inflation rate in the US steadied at 2.7% in April 2024, pausing after an acceleration in March, and matching market forecasts. PCE Price Index Annual Change in the United States averaged 3.30% from 1960 until 2024, reaching an all-time high of 11.60% in March of 1980 and a record low of -1.47% in July of 2009.

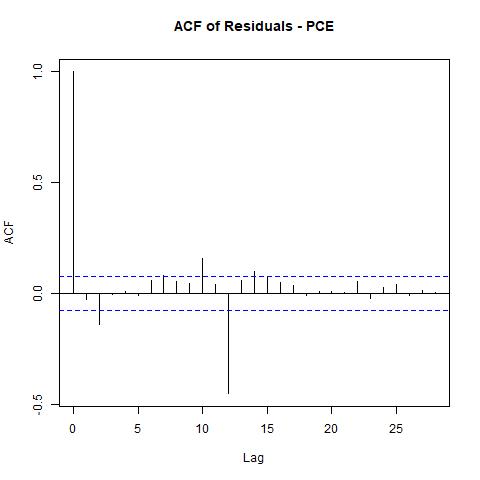

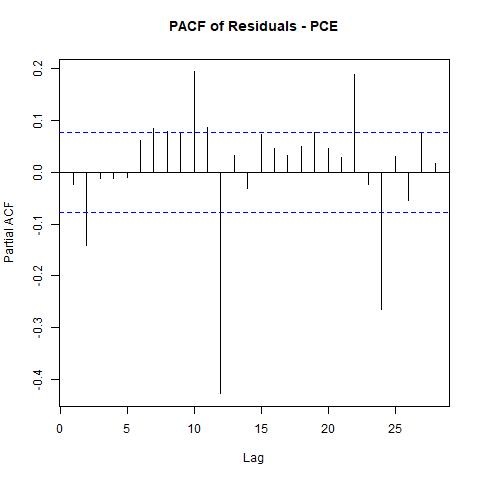

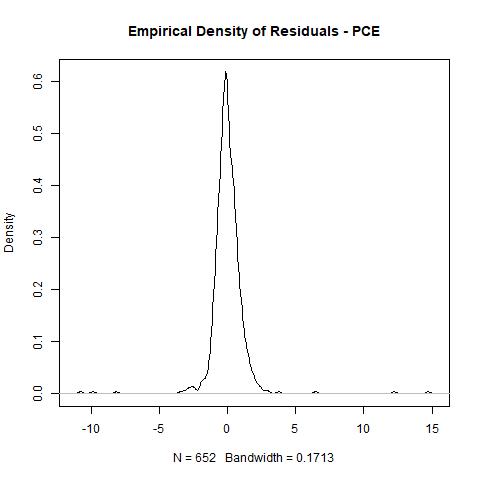

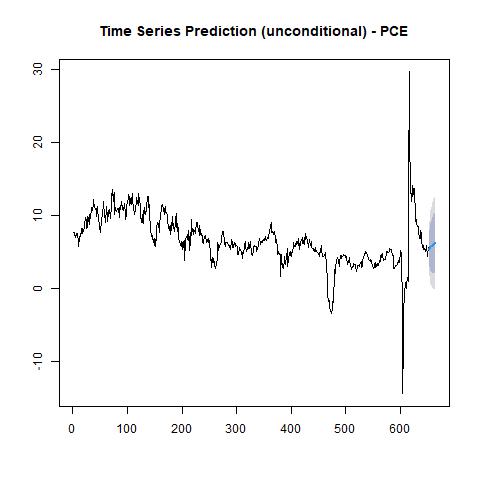

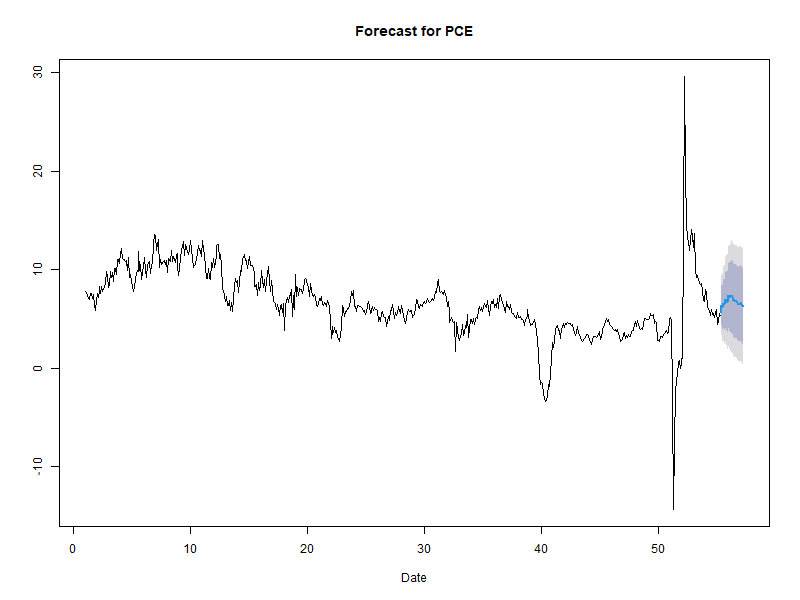

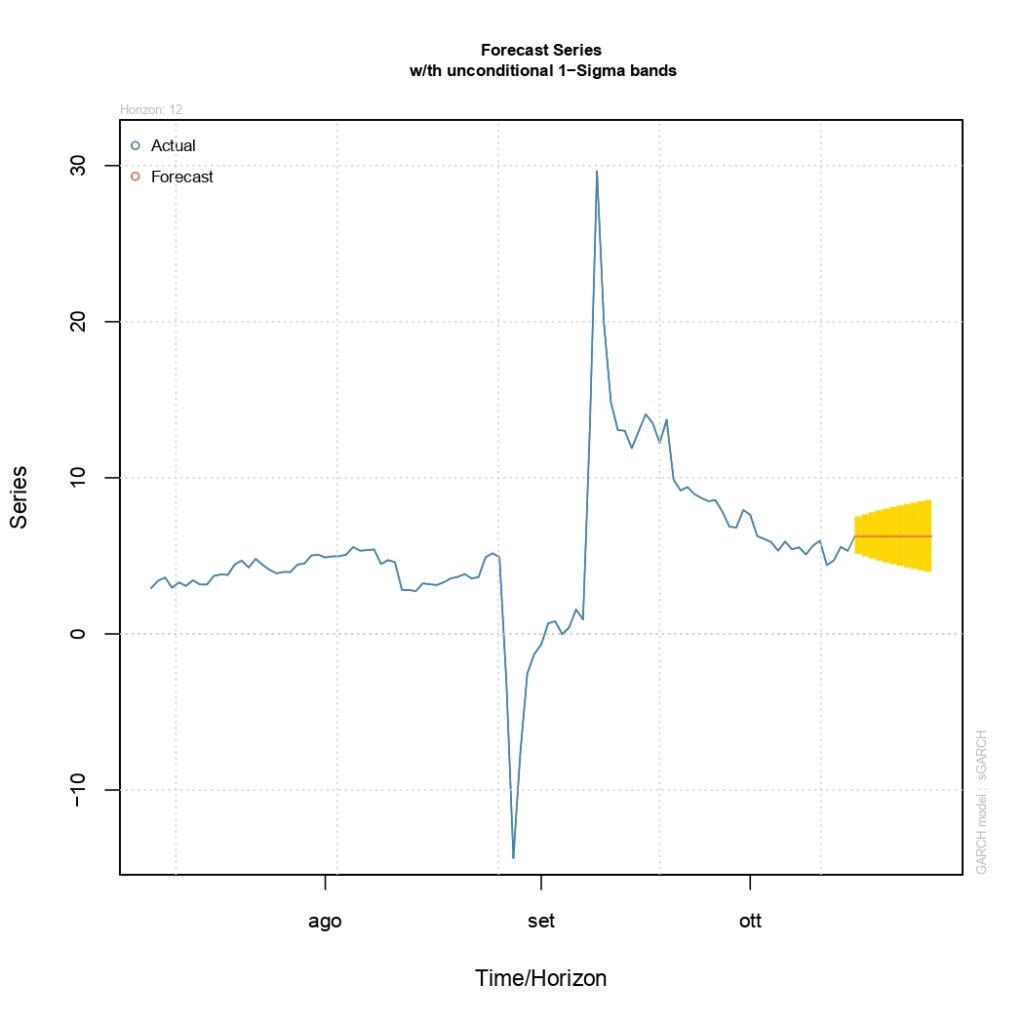

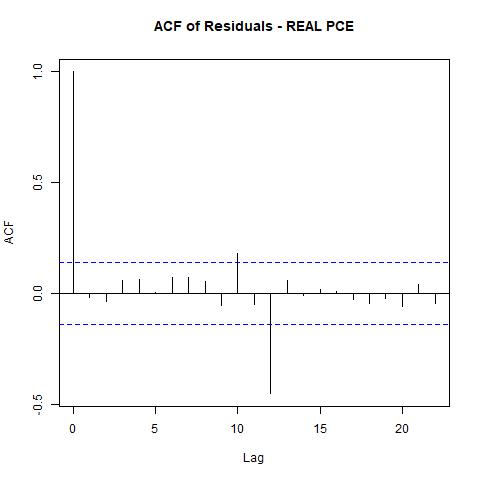

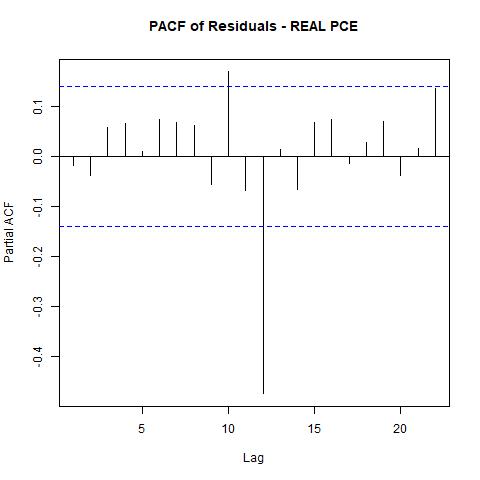

PCE, Personal Consumption Expenditure, timeseries has been analysed in order to forecast future patterns of aggregate consumer spending behaviour based on empirical data. The ACF and PACF graphs hint at the stationarity of timeseries, with some out-of-range value after the 10 lags regression. The forecast for the PCE time series predicts possible increases in consumer spending over the next 12 months. This projected rise in PCE could be influenced by anticipated decreases in interest rates, which typically encourage higher consumer spending.

Indeed, an ARIMA(1,0,1) interpolation of PCE timeseries with 24-month forecasts has elaborated indeed for an increase in the coming months and then a decline in PCE.

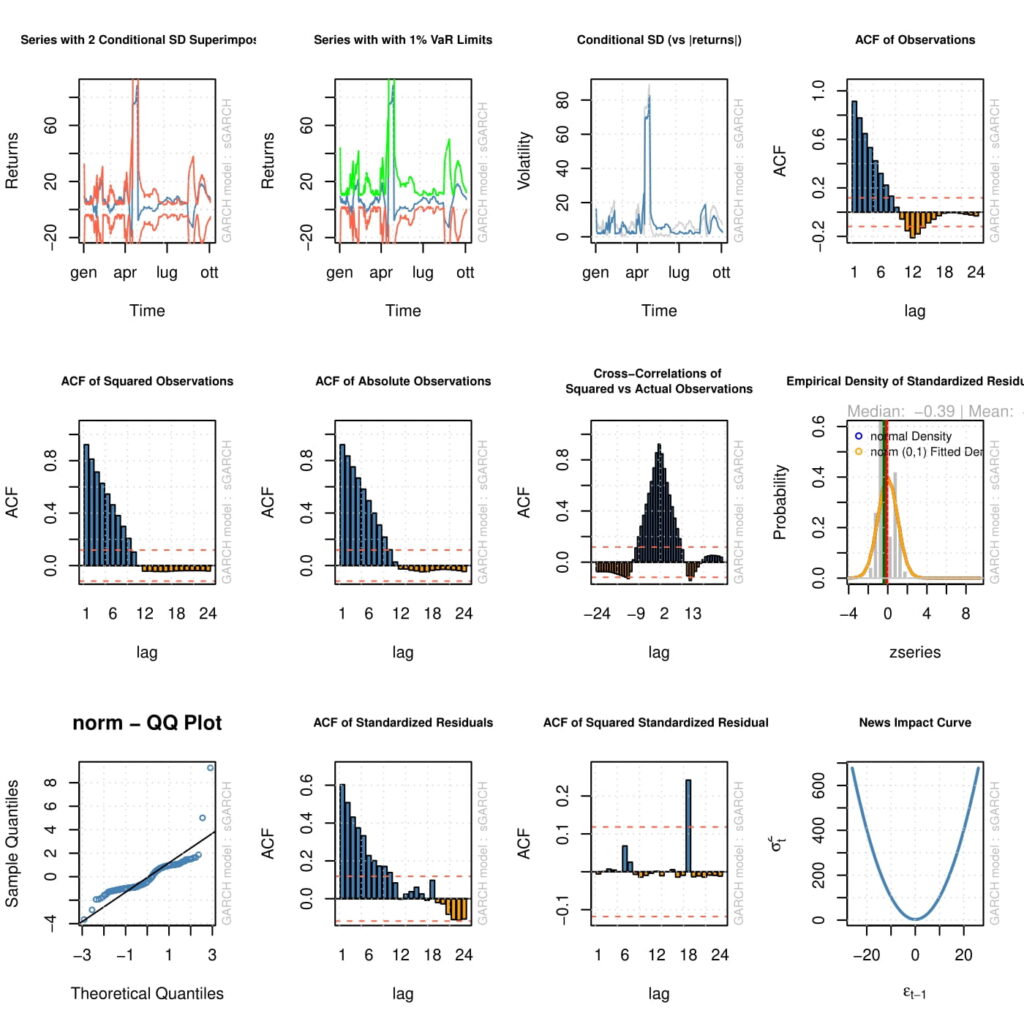

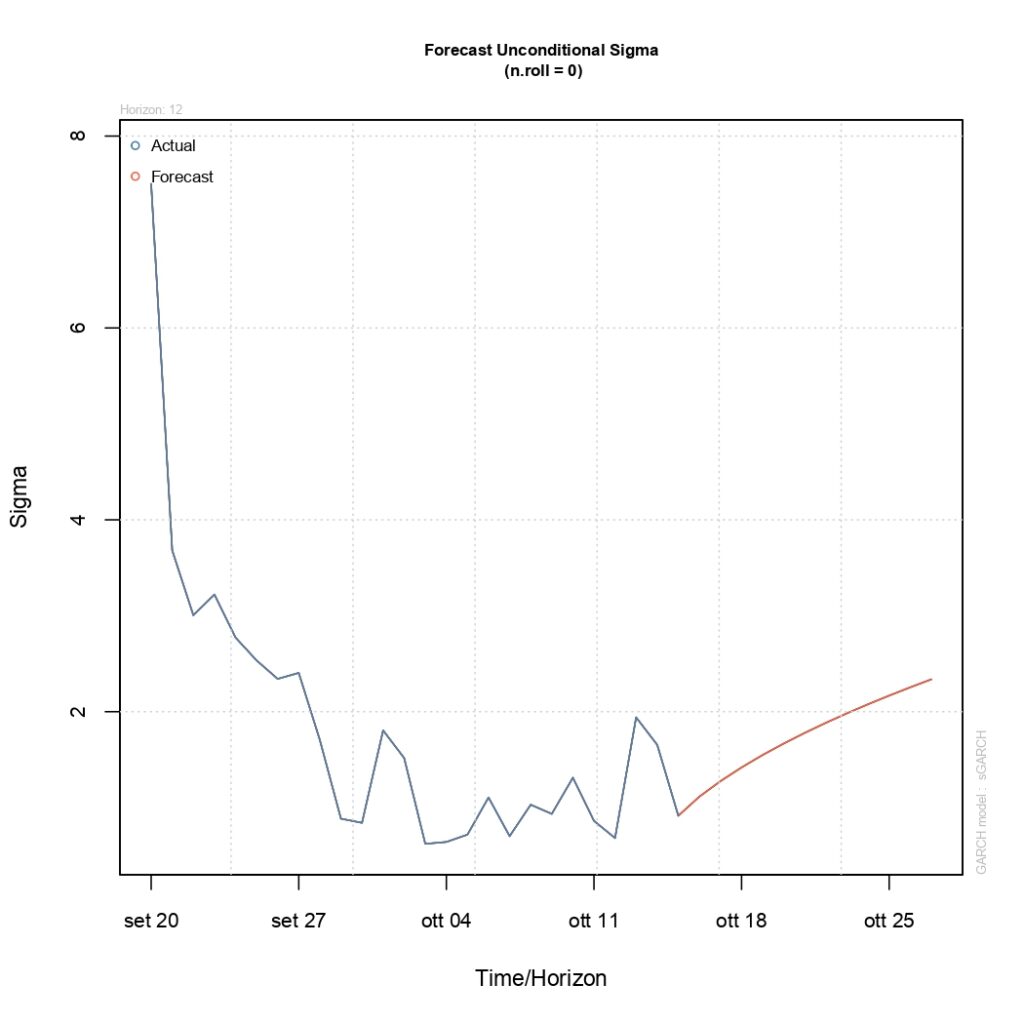

To understand the volatility of the Personal Consumption Expenditure (PCE) time series, a standard GARCH(1,1) model with a mean equation and a variance equation has been applied. This model helps capture the time-varying volatility in the data.

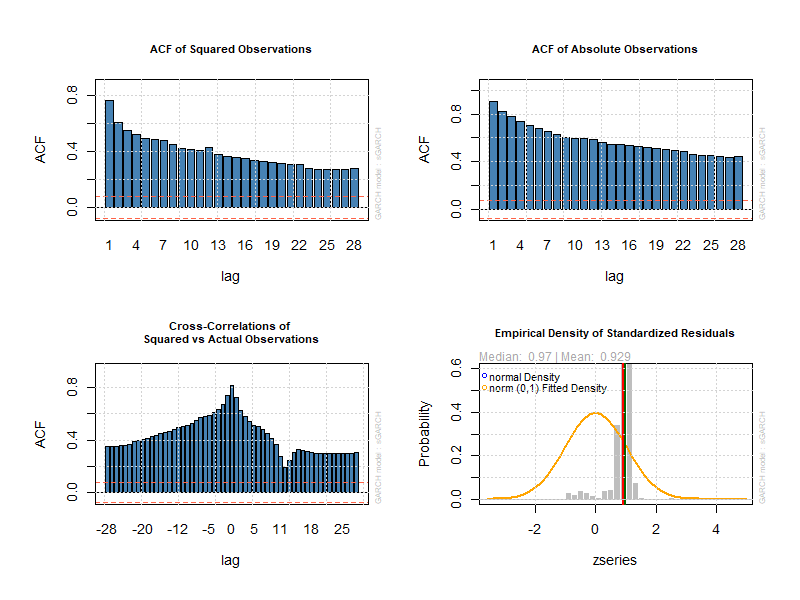

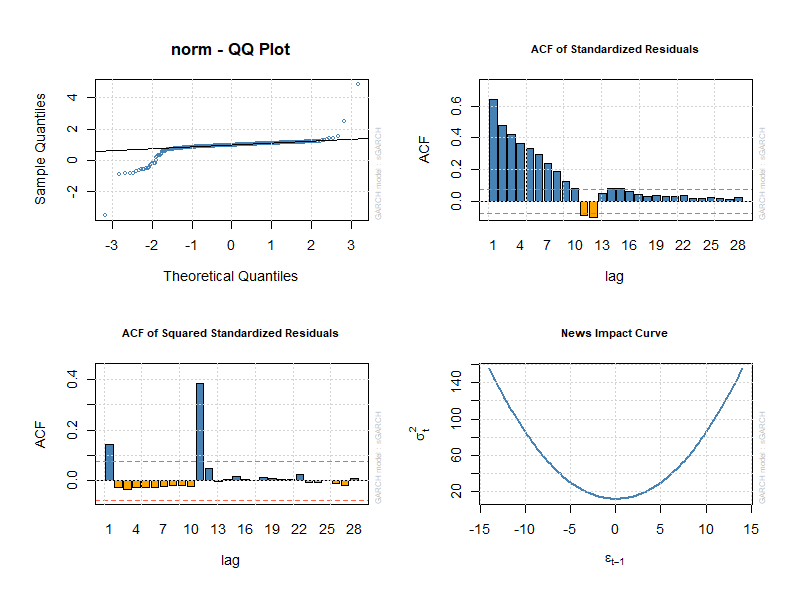

A Standard GARCH(1,1) model has been applied to the PCE timseries in order to understand the volatility of the timeseries. The distribution of the PCE timeseries hints at a slightly tailed distribution that can have a standard deviation range (2, -2), also the ACF confirms volatility of standardized residuals after the (Yt-10) | (Yt-15), 10th | 15th, lag periods. To confirm the potential volatility within the PCE Inflation measures the empirical density of standardised residuals elaborate a positive median of 0.97 that indicates that standardised residuals tend to be positive, implying residuals of PCE Inflation carrying a positive skewness toward higher values, this helps us with the empirical assumption that PCE Inflation timeseries are most of the time made of positive values that can easily deviate above the 2.0% monetary policy price stability target. Indeed, also the mean 0.92 implies the possibility of heavier standard deviation tails, as in fact the norm QQ Plot derives the possibility of heavier tails in a range of (2 |-2) standard deviation from the mean.

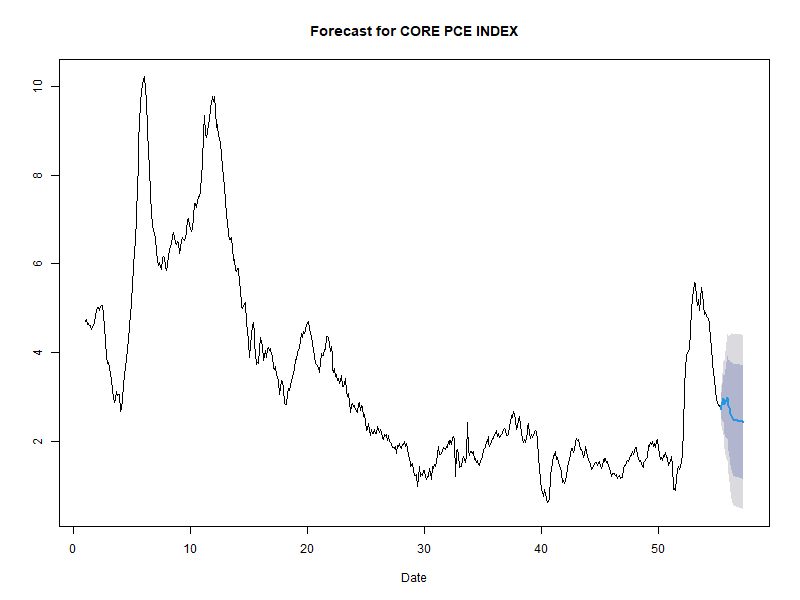

The CORE PCE Index timeseries also has been analysed with an ARIMA(1,0,1) 12-month forecast, which seems in line with the actual trend, predicting an increase also in CORE PCE before converging toward the 2.0% level in the coming 12 months.

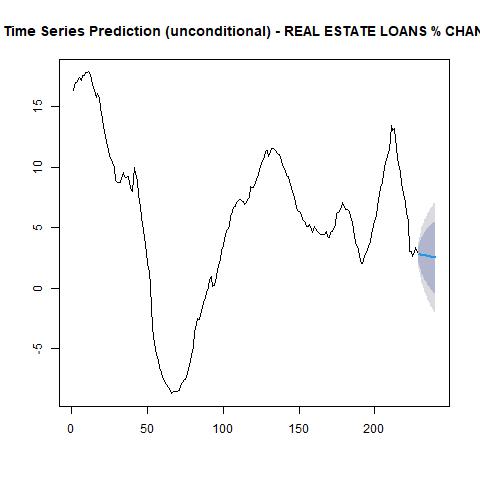

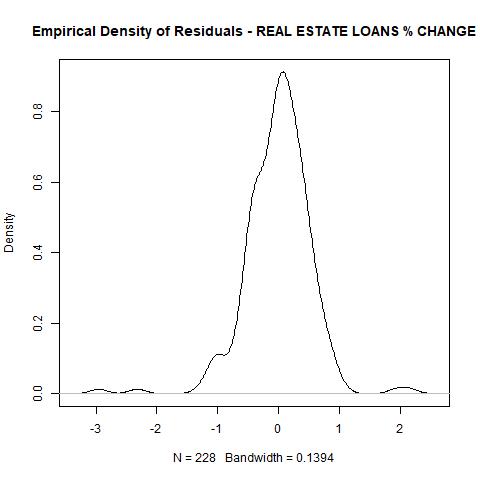

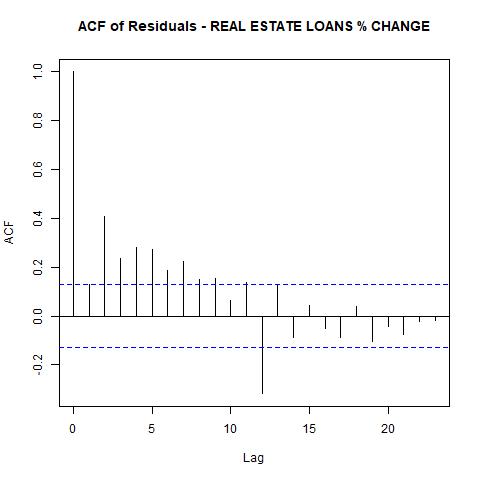

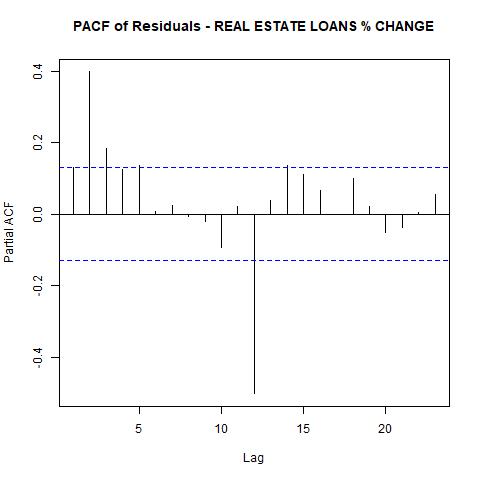

Another bank credit variable has been examined with the Real Estate Loans percentage change timeseries and the timeseries prediction hints at a decline in Real Estate Loans originations issued by U.S. banks, consistent with the past week’s data of a declining trend in housing market activities and constructions. ACF and PACF graphs hint at the lagged stationarity of residuals.

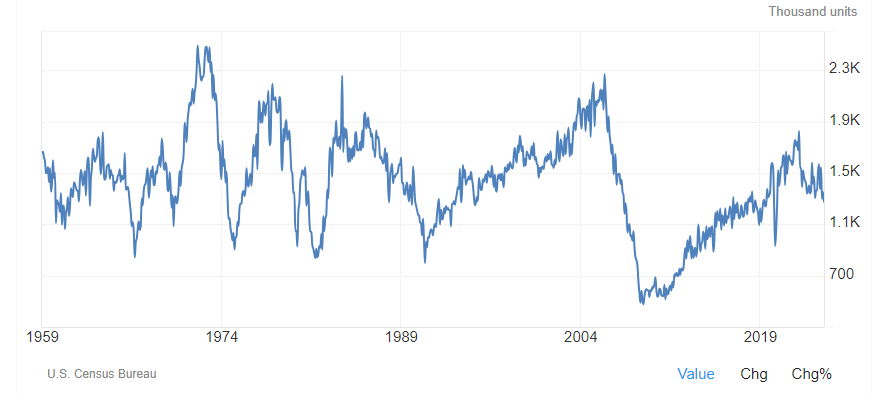

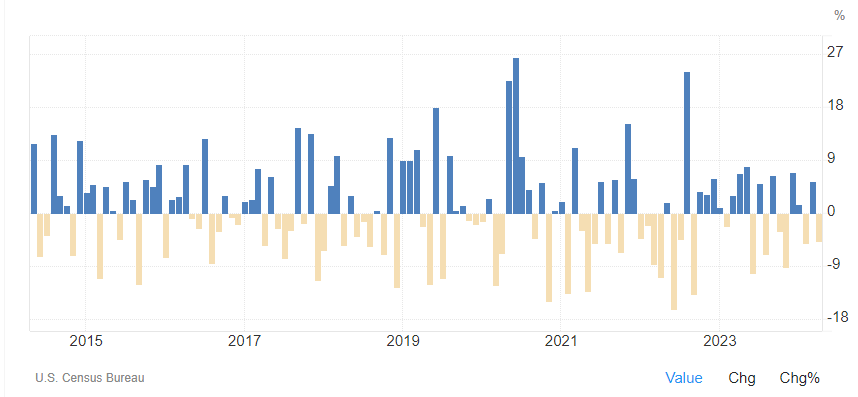

Housing starts in the US fell 5.5% to an annualized rate of 1.277 million in May 2024, the lowest since July 2020.

Sales of new single-family houses in the United States declined 4.7% month-over-month to a seasonally adjusted annualized rate of 634K in April 2024, as high prices and mortgage rates weighed on buyers’ affordability. It follows a downwardly revised 5.4% increase in March.

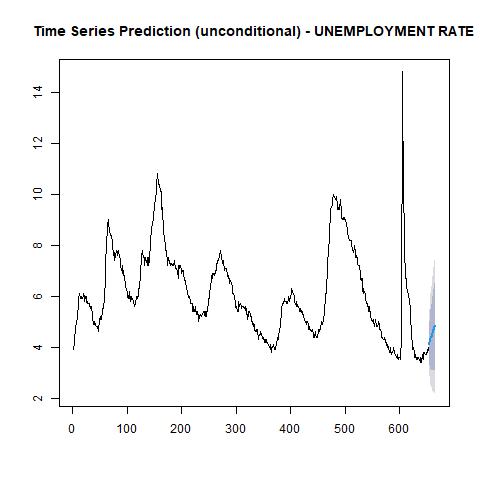

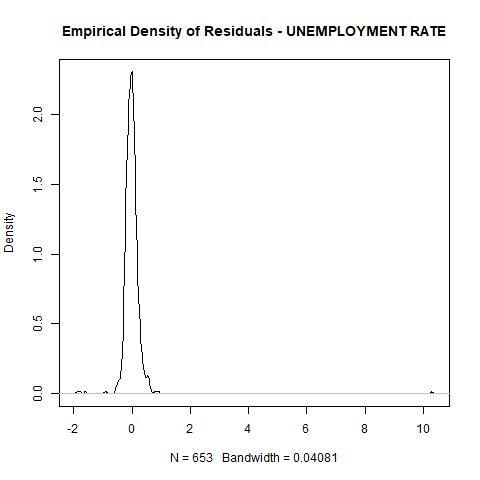

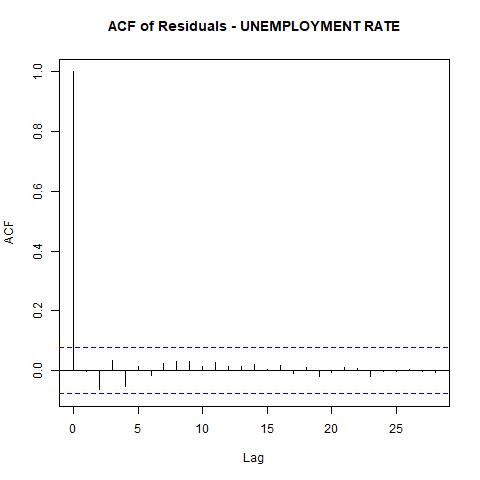

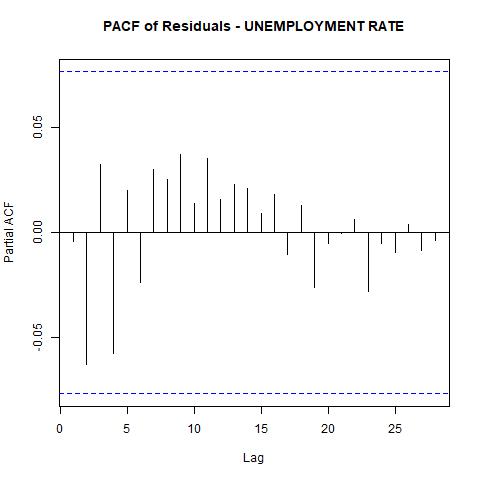

To understand the United States labour market the Unemployment rate timeseries has been examined by applying an ARIMA(1,0,1) model that has elaborated a prediction forecast of an increasing Unemployment Rate in the next 6 to 12 months, that could be consistent with declining activities in the housing market sector and construction industry. The ACF and PACF graphs hint at consistent stationarity in the residuals.

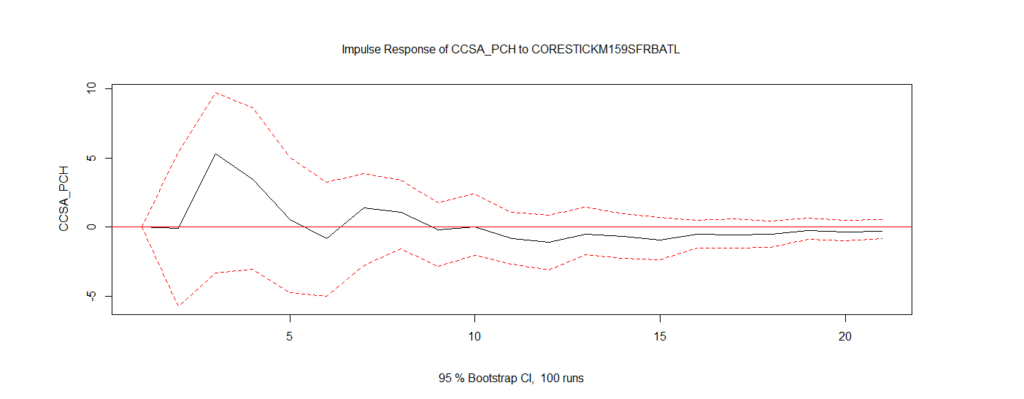

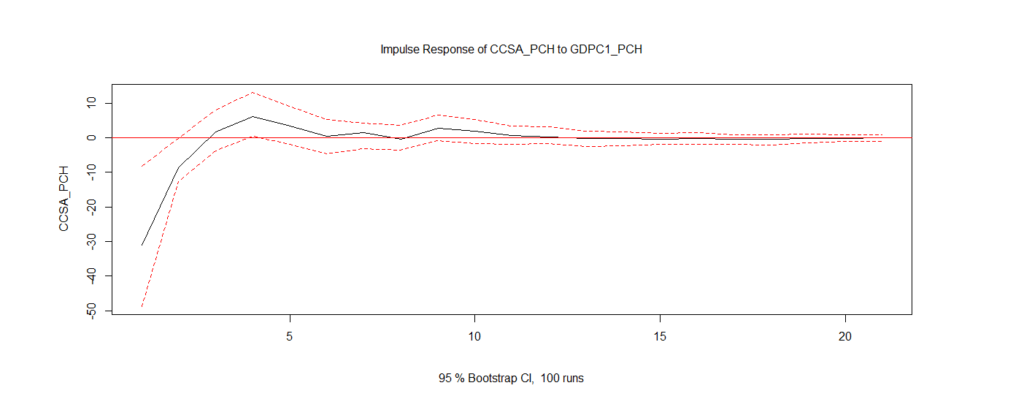

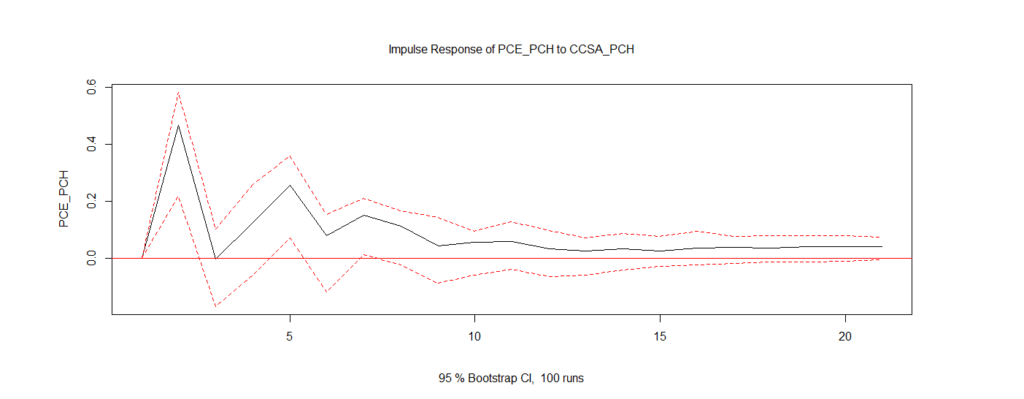

In another econometric research, a VAR(1/4) lags with 8 quarters forecast

has been applied to take as impulse variable the United States’ 4weeks average jobless claims timeseries, while observing the response of the PCE Chained Index and REAL PCE, it’s possible to theorise consistency with ARIMA(1,0,1) prediction of the same timeseries, indicating a slight increase of PCE, in line with the rising trend of 4weeks average jobless claims, before a decline takes place.

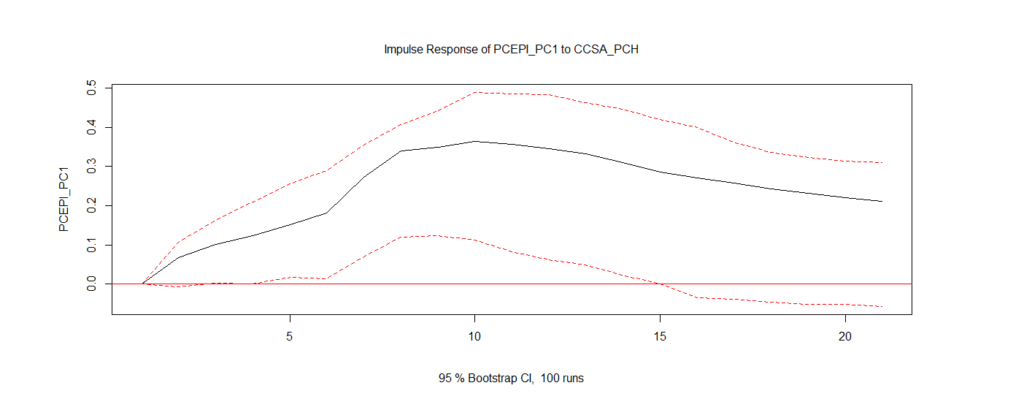

4-week average jobless claims also signal a 5 standard deviation impulse that could spark an increase in CORE Inflation metrics before declining in the next 5 quarters. Overall we could be observing a trend of slightly rising jobless claims increases in the United States economy, in the coming months and quarters, which could hold up various Inflation measures, until then will become a deceleration in USA GDP economic growth