In this article the readers can find theoretical econometric research about the dynamic relationships between macroeconomic indicators, including inflation, interest rates, and real GDP, using Vector Autoregression (VAR) models and ARIMA forecasts. Through impulse response functions (IRFs) and forecast error variance decompositions (FEVD), the study provides insights into short-term economic adjustments to shocks. Forecasting through VAR models complements the analysis, offering future predictions for key variables. The findings contribute to understanding economic resilience and policymaking strategies.

In this article, I have tried to highlight the importance of understanding macroeconomic interdependencies, while observing how shocks propagate among variables and forecast their behaviour, meanwhile implementing well-known econometrics methods such as VAR for dynamic interactions and ARIMA for predictive modelling. Indeed, the variables that have been studied through this procedure: CPI (Consumer Price Index), PPI (Producer Price Index), PCE (Personal Consumption Expenditures), real GDP, Federal Funds Rate, and M2 Real, Quarterly data, spanning the year 2000 to 2024q3.

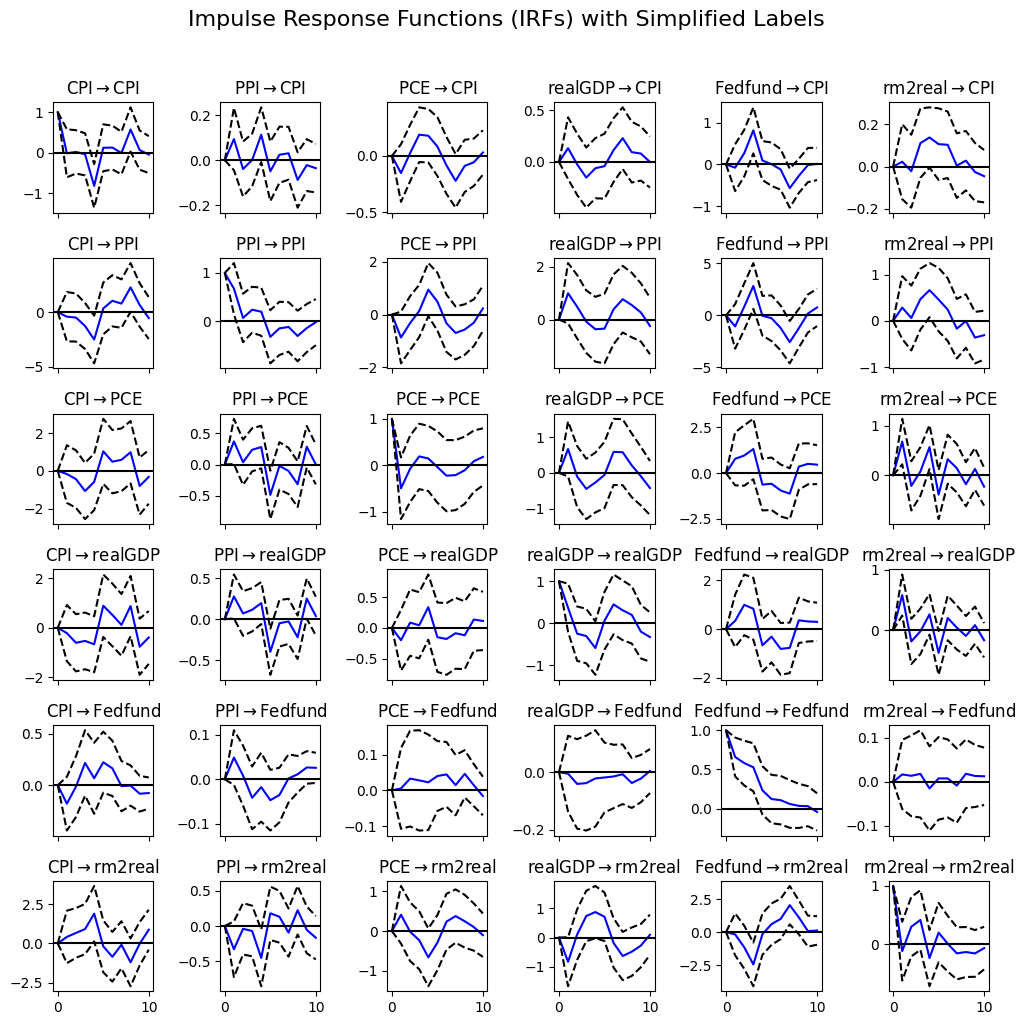

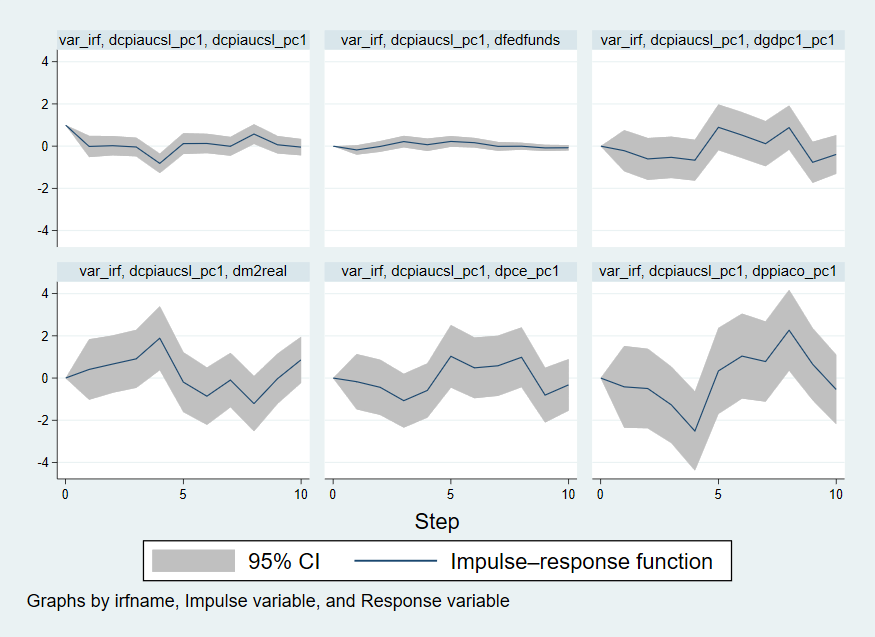

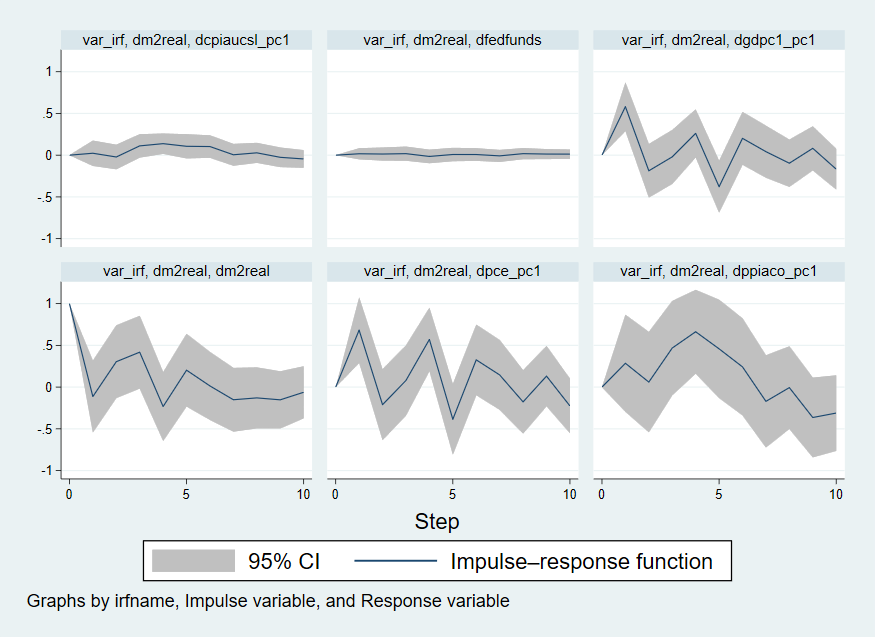

The VAR model is employed to analyze interdependencies among variables without imposing strong theoretical restrictions. IRFs are used to trace the response of a variable to a one-unit shock in another variable, while FEVD quantifies the contributions of shocks to forecast error variance over time. The IRFs reveal significant dynamics between variables. For instance: M2 Real exhibits a delayed but persistent response to Federal Funds Rate shocks, underscoring the liquidity effect. A shock to the Federal Funds Rate leads to a decline in real GDP, with effects peaking after two quarters before gradually dissipating. CPI responds positively to a shock in PPI, reflecting cost-push inflation mechanisms.

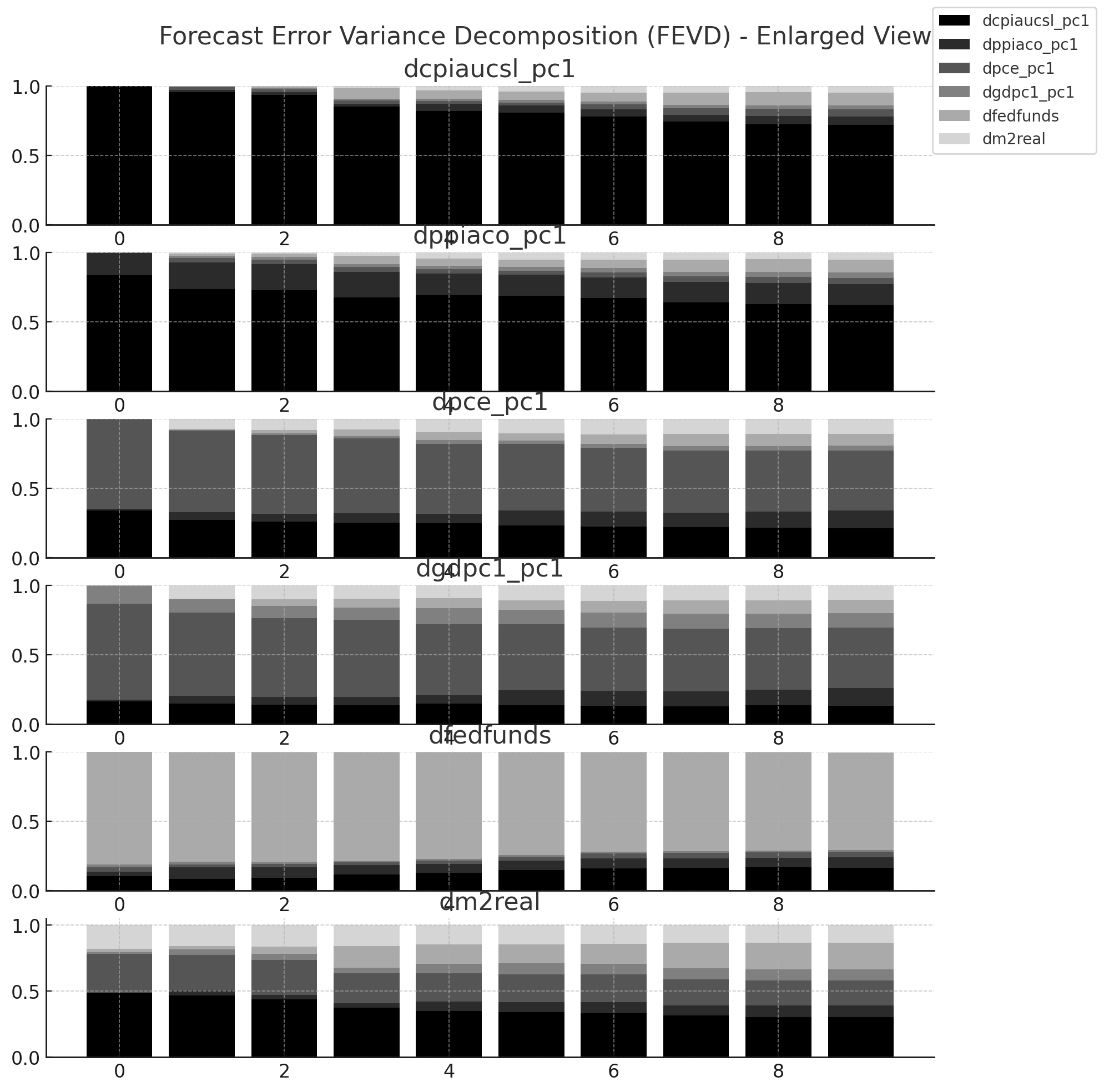

FEVD quantifies the contribution of each variable’s shocks to the forecast error variance of another variable over a specified time horizon. FEVD results show that: Real GDP variance is heavily influenced by its own shocks in the short term but increasingly attributed to Federal Funds Rate shocks over longer horizons. CPI variance is significantly explained by PPI shocks, accounting for up to 40% of the variance at a four-quarter horizon. M2 Real is predominantly influenced by its own innovations, although monetary policy shocks contribute moderately. The results underscore the importance of a balanced monetary policy. The strong influence of Federal Funds Rate shocks on real GDP and inflation highlights the need for cautious interest rate adjustments. Policymakers should also monitor supply-side factors, as evidenced by the significant role of PPI in driving CPI dynamics. The IRF graphs provide evidence of monetary policy transmission mechanisms, where changes in the Federal Funds Rate influence inflation (CPI, PPI) and economic activity (PCE, real GDP). The effects of shocks are generally short-lived, dissipating within 5-10 periods, highlighting the adjustment mechanisms in the economy. Shocks to real GDP and Federal Funds Rate have the most significant spillover effects, emphasizing their central role in macroeconomic stability. The strong response of CPI and PPI to monetary shocks underscores the importance ofthe Federal Funds Rate in controlling inflation. Policymakers should prioritize stabilizing inflation expectations to minimize adverse effects on consumption and GDP. Shocks to PCE have significant positive effects on real GDP, suggesting that policies encouraging consumer spending (e.g., tax cuts or subsidies) can stimulate economic growth during downturns. The interplay between M2 Real and other variables highlights the importance of monitoring money supply dynamics alongside interest rate policies to manage inflation and growth effectively. The rapid dissipation of shocks in IRFs suggests that the economy adjusts relatively quickly to disturbances. Policies should aim to enhance this resilience by improving market flexibility and ensuring robust financial systems.

This study demonstrates the interconnectedness of key macroeconomic variables through FEVD and IRF analyses, highlighting the importance of monetary policy in stabilizing inflation and promoting growth. Future research could explore: Structural VAR (SVAR) models to account for exogenous shocks like global crises. The outcome of fiscal policy variables, such as government spending and taxation, on the analyzed relationships. Extending the analysis to international variables, such as exchange rates and trade balances, to study spillover effects in an open economy.

Data sources: