Economic data for the euro area presents a mixed picture, with inflation proving stickier than anticipated while growth remains fragile. Key member states like Spain, Germany, and Italy reported figures that highlight the ongoing challenges faced by the European Central Bank (ECB) and national governments.

Spain’s Inflation Accelerates Beyond Forecasts

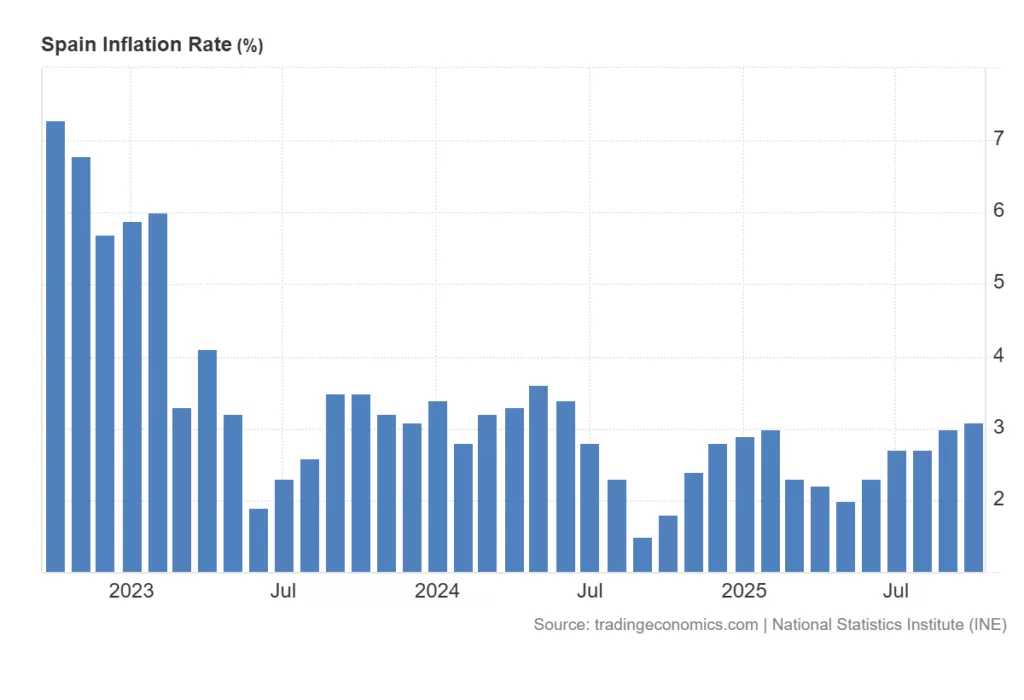

Spain’s preliminary inflation data surprised markets on the upside, the annual inflation rate (YoY) rose to 3.1% in October, up from 3% in September and exceeding market estimates of 2.9% . On a monthly basis (MoM), consumer prices jumped 0.7%, a significant rebound from the 0.3% decrease in September. The core inflation rate, which excludes volatile food and energy prices, accelerated to 2.5% year-on-year, its highest level in ten months . This suggests that inflationary pressures are becoming more broad-based.

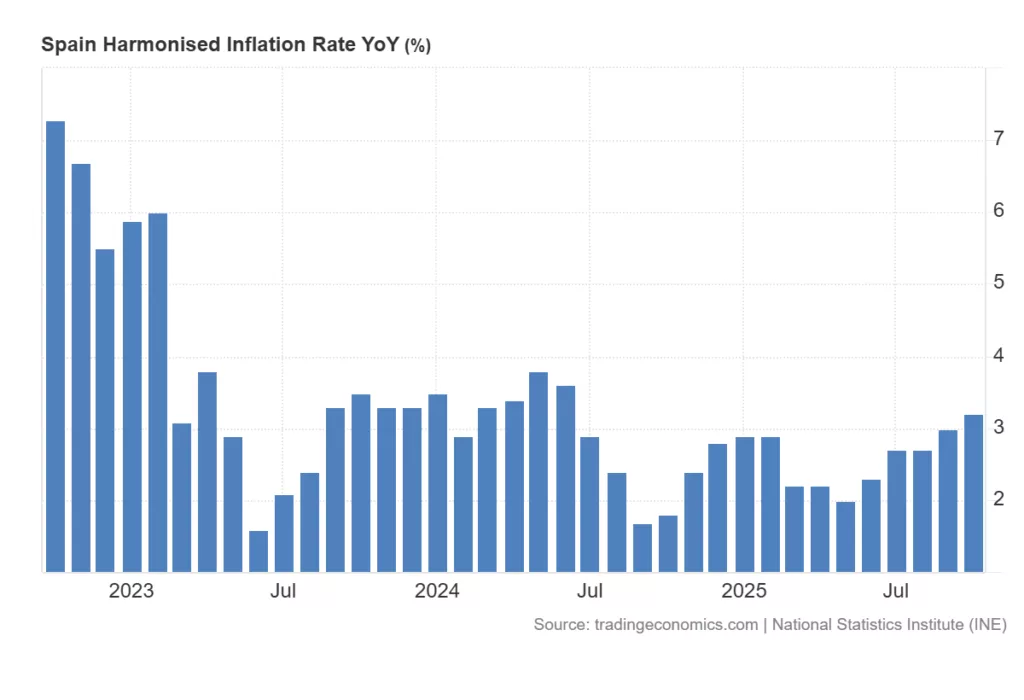

The EU-harmonised inflation rate (HICP) came in at 3.2% year-on-year, also above forecasts . The main drivers were stronger increases in electricity prices compared to October 2024 and higher transport costs .

Germany’s Stagnant Growth and Stable Labour Market

Latest data from Europe’s largest economy paints a picture of an economy stuck in neutral, but with underlying strengths that are preventing a deeper downturn. Germany’s economy narrowly avoided a technical recession in the third quarter, posting precisely 0.0% quarter-on-quarter growth, a marginal improvement from the -0.2% contraction in Q2. Year-on-year, growth remained an anemic 0.3%. This stagnation, however, is set against a surprisingly robust labor market, which continues to be a key pillar of stability. The unemployment rate held firm at 6.3% in October, with the number of unemployed persons dipping slightly to 2.973 million and the unemployment change figure showing a modest decline of -1K, defying expectations for an increase. On the inflation front, there were signs of continued moderation as the preliminary annual inflation rate (YoY) for October eased to 2.3%, down from 2.4% in September and aligning with the ECB’s target. The harmonised index (HICP) also came in at 2.3%. This disinflationary trend was consistent across major states like Baden Wuerttemberg (YoY 2.3%), Bavaria (2.2%), and North Rhine Westphalia (2.3%), indicating that price pressures, while persistent, are broadly cooling. In summary, Germany presents a dual narrative: a stagnant macroeconomic engine unable to find forward momentum, yet underpinned by a tight labor market and inflation that is gradually returning to target, leaving policymakers balancing fragility against resilience.

France Emerges as Eurozone’s Surprise Performer in Q3

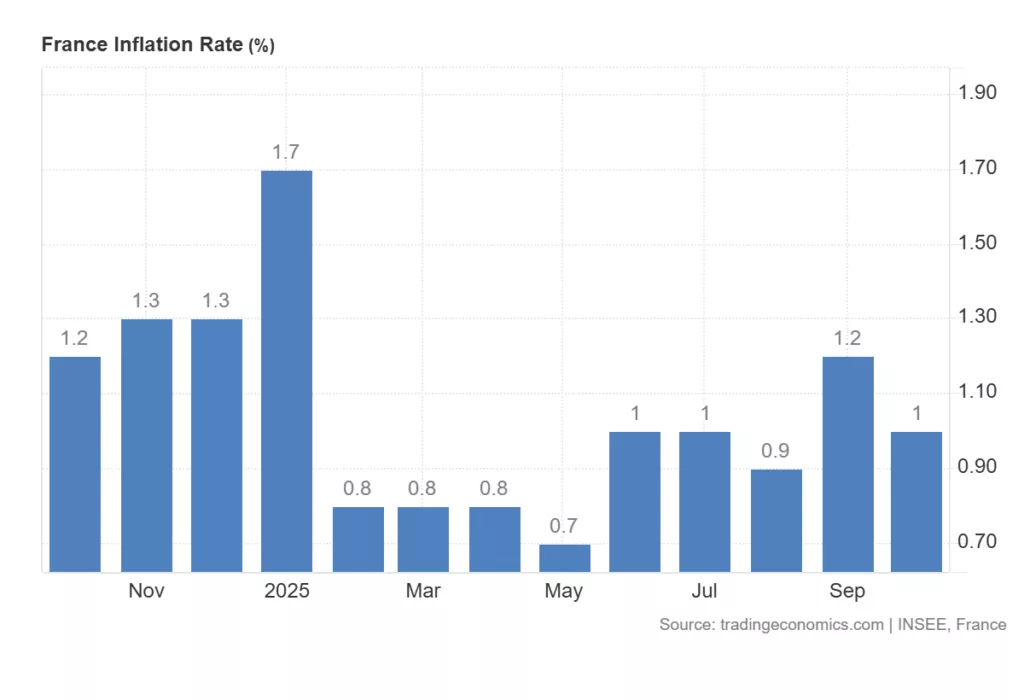

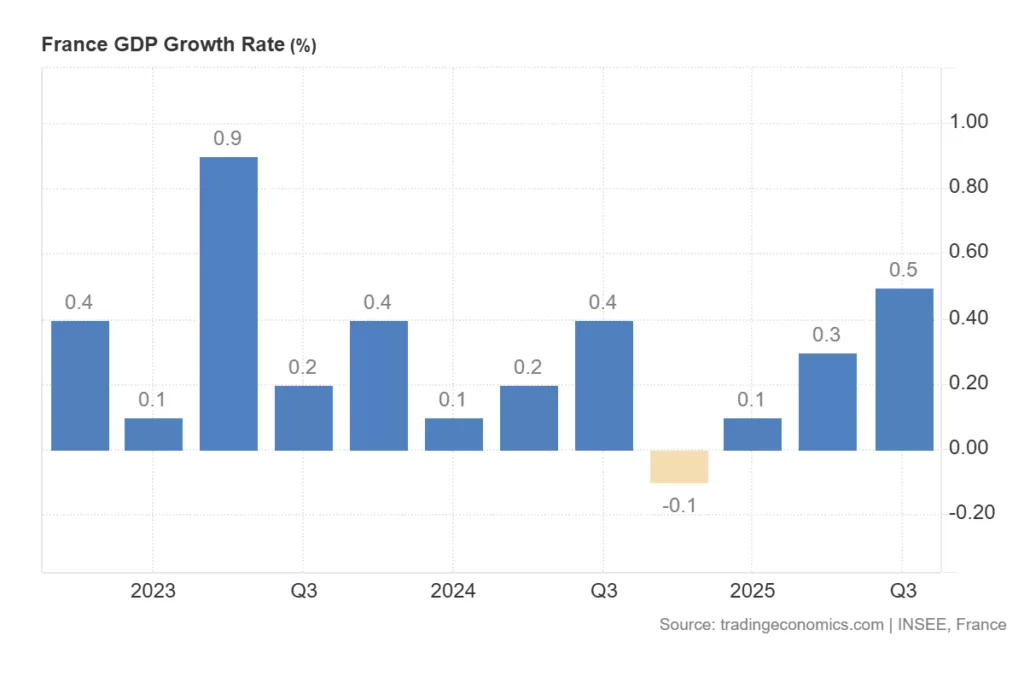

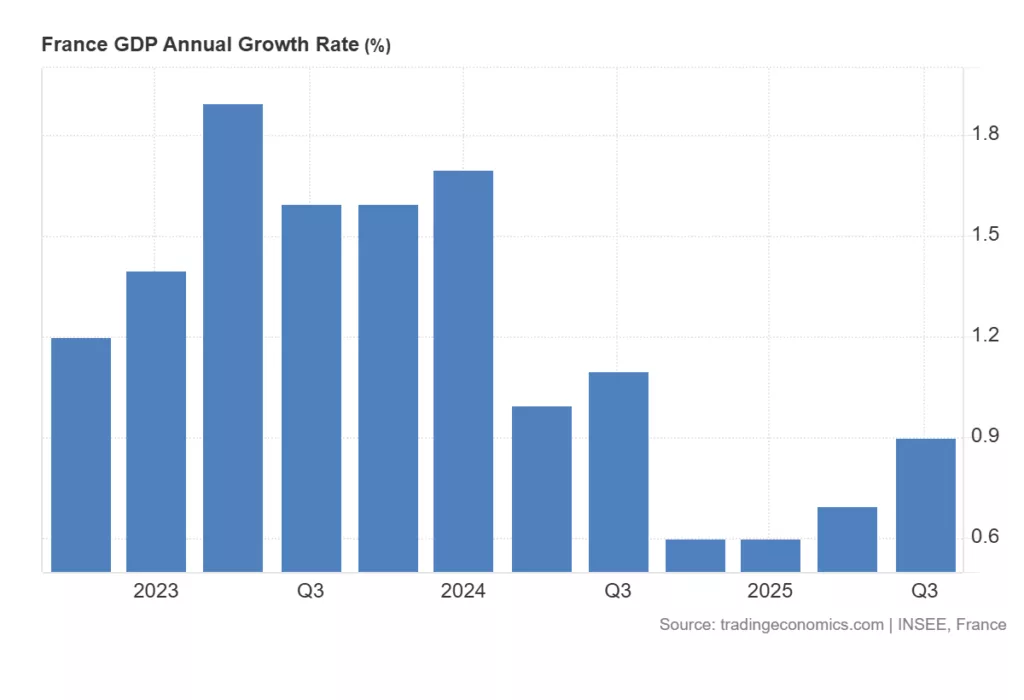

While its larger neighbour Germany stagnates, France delivered a surprisingly robust economic performance in the third quarter, effectively acting as the eurozone’s growth engine. Preliminary data shows GDP expanded by a strong 0.5% quarter-on-quarter, significantly outperforming both the previous quarter’s 0.3% and market expectations of a mere 0.1%. Year-on-year, growth accelerated to 0.9%, further confirming the positive momentum. This growth appears to be supported by a resilient consumer, with household consumption rising 0.3% month-on-month in September, beating forecasts. The positive growth story is coupled with a remarkably benign inflation environment. France’s annual inflation rate (YoY) cooled to 1.0% in October, falling below expectations and solidifying its position well below the eurozone average. This disinflation is further evidenced by weak producer prices, with the PPI remaining flat on an annual basis at 0.1% in September. This combination of robust growth and cooling price pressures presents a favourable and somewhat unique economic picture within the euro area, suggesting domestic demand is holding up without fueling inflationary fires.

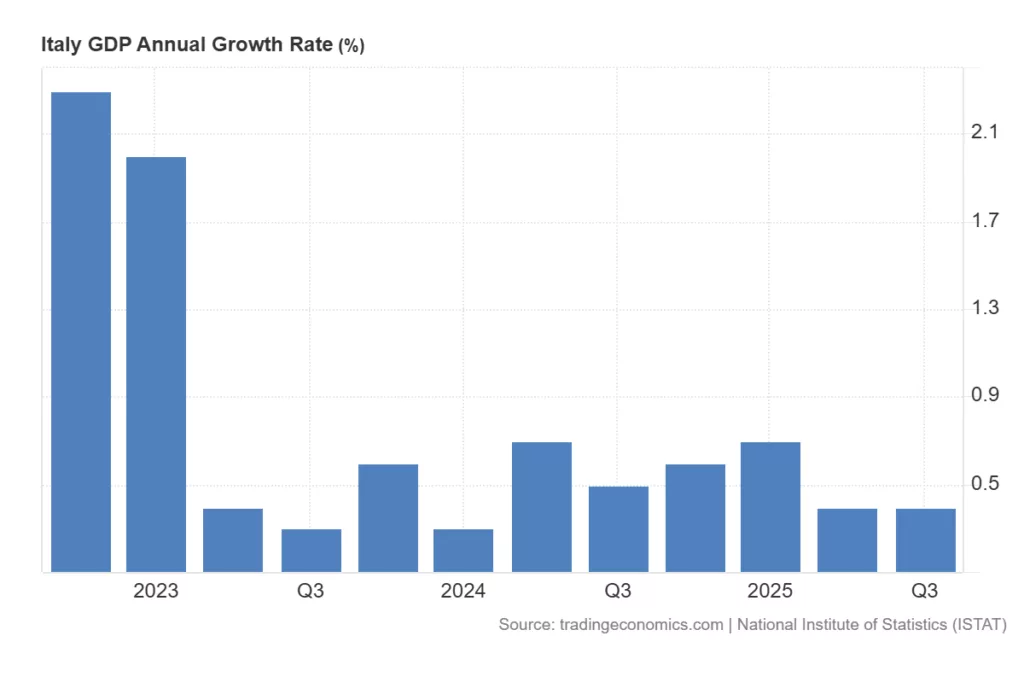

Italy’s Economy Flatlines as Industrial Sales Fall

Italy’s economy showed little momentum in the third quarter, while earlier data pointed to weakness in industrial activity, the economy registered 0.0% growth quarter-on-quarter in the advanced estimate for Q3. Year-on-year growth was 0.4%. Industrial sales in August fell 0.7% from the previous month, reversing a 0.4% gain in July. On a yearly basis, sales edged down 0.1%.

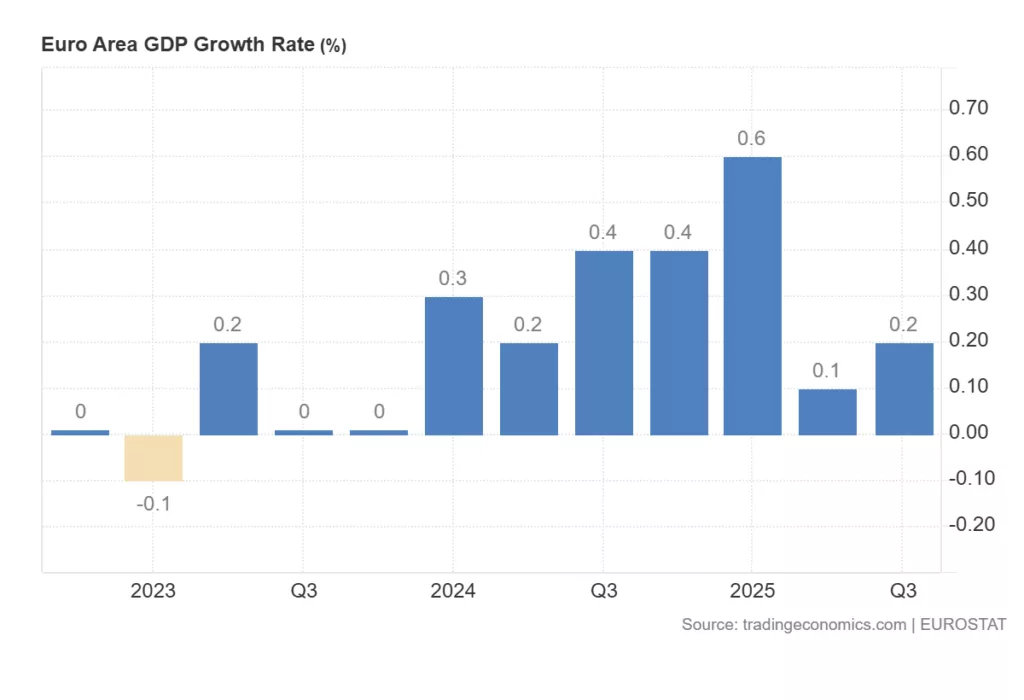

Euro Area Macro-Data Estimates

According to the flash estimates, the euro area economy grew by 0.2% in the third quarter of 2025, showing unexpected resilience by slightly beating expectations . This growth was uneven, driven by strong performances in some major economies while others stalled.

| Economic Indicator | Reference Period | Actual Result | Previous Period | Forecast |

|---|---|---|---|---|

| GDP Growth (QoQ) | Q3 2025 | 0.2% | 0.1% | 0.1% |

| GDP Growth (YoY) | Q3 2025 | 1.3% | 1.5% | 1.2% |

| Economic Sentiment | October 2025 | 96.8 | 95.6 | 95.7 |

| Unemployment Rate | September 2025 | 6.3% | 6.3% | 6.3% |

| Consumer Confidence | October 2025 | -14.2 | -14.9 | -14.2 |

| Industrial Sentiment | October 2025 | -8.2 | -10.1 | -10.0 |

| Services Sentiment | October 2025 | 4.0 | 3.7 | 3.3 |

| Selling Price Expectations | October 2025 | 7.5 | 7.1 | N/A |

| Consumer Inflation Expectations | October 2025 | 21.9 | 24.0 | N/A |

The 0.2% quarterly growth for the euro area and 1.3% GDP growth Year-on-Year, was bolstered by strong performances in several member states, though the recovery remains uneven, the wider European Union (EU27), GDP grew by 0.3% in the third quarter. The better-than-expected GDP figure, alongside improving business activity data, points to underlying economic resilience, reinforcing the European Central Bank’s (ECB) decision to pause its rate-cutting cycle. The ECB kept interest rates unchanged, with its key deposit facility rate at 2% . Analysts at Ebury suggest that “the ECB’s rate cutting cycle appears to be over, at least for now” .