The UK financial industry in 2023 through LSEG post-trade clearing LCH, has cleared record volumes in Euro Derivatives contracts as follows: EUR IRS (Euribor) volume €51 trillion in 2023 and €50.9 trillion in 2022, EUR OIS volume €116.6 trillion in 2023 and €81.7 trillion in 2022, record highs were seen with €304.9 trillion in nominal cleared across Euro-denominated swaps, CDSClear (Euro Credit Derivatives):€4.76 trillion

The European financial system and its EuroBond market will have to confront a pivotal moment as it strives for deeper integration and resilience in the face of global economic shifts and post-Brexit realignments. A fully realized Capital Markets Union (CMU) is crucial for the European Union to enhance financial stability, promote economic growth, and ensure its competitive edge in global markets. While focusing on liquidity within the European financial industry, euro area debt sharing, euro bond market liquidity, and the strategic relocation of euro clearing and related activities within the eurozone under European jurisdiction.

Capital Markets Union: A Cornerstone for European Financial Stability

The Capital Markets Union (CMU) aims to integrate and unify capital markets across EU member states. Despite progress, fragmentation persists due to regulatory discrepancies, cultural differences, and varying levels of market development. A fully integrated CMU would provide businesses with broader access to finance, reduce reliance on bank lending, and bolster cross-border investments. The deepening of liquidity in Euronext and other European financial markets is vital for achieving this goal. Euronext, as a multi-national stock exchange, represents a cornerstone for European equity trading. Enhanced liquidity in these markets would lower transaction costs, increase efficiency, and attract global investors, strengthening the EU’s position as a financial hub. Additionally, harmonizing financial regulations and fostering an ecosystem of innovation could further amplify the CMU’s benefits.

Euro Area Debt Sharing and Bond Market Liquidity

The euro area has long grappled with asymmetric fiscal policies among member states. The introduction of mechanisms for debt sharing, such as joint euro area bonds, is essential to reinforce the monetary union. A more integrated bond market would allow member states to access funding on equal terms, enhancing fiscal stability across the bloc. Shared debt instruments, like Eurobonds, would also deepen market liquidity, reducing borrowing costs and providing a robust buffer against economic shocks. Moreover, improved liquidity in the euro bond market can serve as a foundation for collateral posting. In the European Central Bank’s (ECB) monetary operations and wider financial markets, high-quality collateral is crucial for maintaining liquidity and facilitating fiscal spending. By fostering a liquid and deep bond market, the euro area can ensure a smoother transmission of monetary policy and greater financial stability.

Relocating Euro Clearing and Financial Activities to the Eurozone

Brexit has fundamentally altered the financial relationship between the European Union and the United Kingdom. The clearing of euro-denominated derivatives—a critical aspect of financial markets—remains predominantly handled in London. This situation poses a strategic vulnerability to the eurozone, as it outsources a vital financial function to a non-EU jurisdiction. To safeguard its monetary sovereignty and mitigate systemic risks, the EU must repatriate all euro-clearing activities to clearing houses within the eurozone, under European jurisdiction. Such a move would ensure compliance with EU financial regulations, reduce dependence on the UK, and provide the ECB with greater oversight of systemic financial activities. Beyond derivatives, the European Investment Bank (EIB) and other banking activities related to euro-area financial stability should also be fully integrated within the eurozone. These measures would consolidate the EU’s financial autonomy and fortify its global standing.

Passporting Rights for UK Financial Services are not a given, but a privilege.

Safeguarding EuroArea Financial Stability Risks

The United Kingdom’s vast financial footprint, with external debt exceeding £7 trillion in financial assets, poses significant risks to the European financial system, as the UK Private Pension Funds crisis in 2022 exposed highly leveraged balance sheet exposures of Investment Funds operating from the UK Financial system. This external debt—one of the largest globally relative to GDP—raises systemic concerns, particularly in the context of the UK’s undercapitalized banking sector. A failure within the UK financial system could propagate instability across the eurozone, given the interconnectedness of global markets. This underscores the necessity of revising the residual passporting rights of UK-based financial services to protect the integrity of the euro area’s financial stability and clearing systems. Access to Euro Area financial services and passporting rights for UK Banks and other financial entities are not a given, but a privilege, and the undercapitalization of UK banks, many of which are leveraged to an extent that heightens exposure to external shocks, is a particular concern. In a crisis scenario, these vulnerabilities could lead to cascading defaults, disrupting not only the UK economy but also the broader European financial ecosystem. By continuing to allow UK financial institutions to operate under insufficient oversight and regulatory alignment, the EU exposes itself to systemic risks that could compromise the functioning of its monetary and financial infrastructure. Euro clearing involves the settlement of trades in euro-denominated derivatives and other financial instruments, a market valued in trillions of euros annually. The continued reliance on London for euro-clearing activities represents a strategic vulnerability for the euro area. Revenues, commissions, and jobs generated by this activity—rightfully belonging to the eurozone financial services industry—are effectively “extorted” by the UK. This arrangement deprives the EU of valuable economic activity, undermines the development of its own financial services sector, diminishes the potential of jobs, growth and integration of the Euro Area financial services and denies European citizens wider access to fairly paid employment and opportunities.

Bringing euro clearing and related activities into the eurozone would address these economic and systemic imbalances. Such a move would ensure that the economic benefits of clearing euro-denominated instruments—such as job creation, increased tax revenues, and the growth of domestic financial expertise—are retained within the EU. It would also eliminate the dependence on an external jurisdiction for critical financial infrastructure, thereby reinforcing the eurozone’s sovereignty and resilience. Moreover, relocating these activities would enable the European Central Bank (ECB) and other EU regulatory authorities to exercise direct oversight over euro-denominated transactions. This would not only enhance regulatory coherence but also ensure alignment with EU financial stability objectives, reducing the risks associated with external disruptions. The argument for reviewing passporting rights also extends to the principle of economic justice. European taxpayers and citizens have a vested interest in seeing the financial services industry—an essential pillar of the modern economy—develop within their borders. Allowing the UK to continue reaping the economic benefits of euro clearing and other financial activities without full alignment with EU regulations amounts to an economic leakage that undermines the EU’s strategic ambitions. Reviewing passporting rights for UK financial institutions could become a necessary step to mitigate systemic risks, repatriate critical economic activities, and foster the development of a robust and integrated financial services industry within the EU. These measures would not only protect the euro area’s stability but also ensure that its economic benefits are equitably shared among its member states and citizens.

Broader Implications for European Independence and Economic Growth

The integration of financial markets and institutions within the eurozone is not merely a technical or economic necessity. In deepening its financial architecture, the EU can better manage systemic risks, respond effectively to crises, and drive sustainable economic growth. A unified approach to financial regulation and market development would also support the EU’s broader geopolitical ambitions, enabling it to compete with other major economic powers like the United States and China. A fully realized Capital Markets Union, coupled with deeper integration of liquidity and euro area debt markets, is essential for the EU’s financial and economic resilience. Repatriating euro clearing and related financial activities from the UK, alongside a reevaluation of UK financial passporting rights, would consolidate the eurozone’s autonomy and regulatory oversight. These steps are vital not only for fostering economic stability but also for securing the EU’s position as a global financial industry leader.

READ MORE:

https://www.ecb.europa.eu/press/fie/box/html/ecb.fiebox202406_02.en.html

https://www.eib.org/en/index.htm

https://www.euroclear.com/en.html

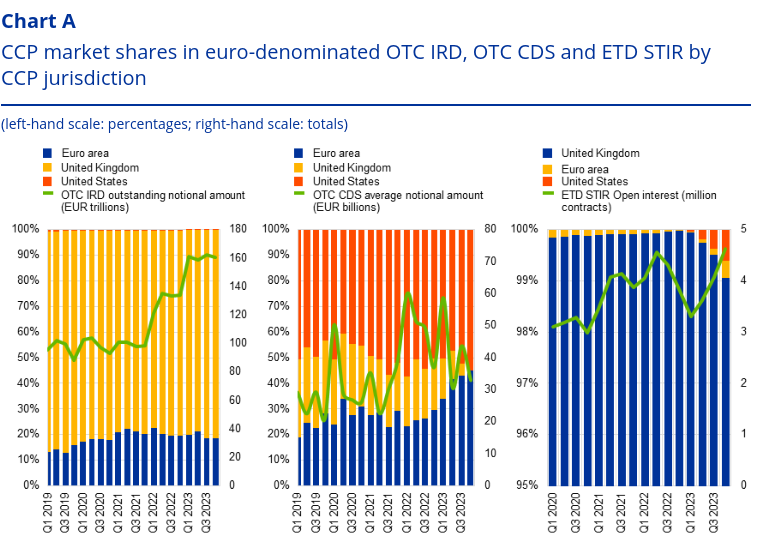

“Although the market share of euro area CCPs has increased over time, the over-reliance of euro area market participants on non-euro area clearing services persists. Over the period from 2019 to 2023, euro-area clearing members and clients reduced their use of UK CCPs across all euro-denominated OTC derivatives, primarily to the benefit of euro-area CCPs, while their use of CCPs in other jurisdictions remained stable (Chart C).[12] Nevertheless, following the initial surge in relocation activities at the time of heightened uncertainty about major Brexit-related decisions, the decrease in the market share of UK CCPs levelled off in 2021 for euro area clearing members and in 2022 for clearing clients.

https://www.ecb.europa.eu/press/fie/box/html/ecb.fiebox202406_02.en.html

The continued over-reliance on UK clearing services could have serious implications for the financial stability of the EU, especially under stressed market conditions. In such circumstances, difficult risk management decisions may have to be taken in order to contain losses, either at the discretion of the CCP or upon instruction by the home authority.[13] Such decisions could include margin increases or changes to eligible collateral or collateral haircuts, which could lead to further market stress or deepen financial difficulties for EU counterparties or the EU financial market as a whole. From a monetary policy perspective, disruptions in critical derivatives markets could hamper the effective implementation of monetary policy decisions.[14],[15] While EMIR grants ESMA direct supervisory powers over systemically important third-country CCPs, these are not as stringent as those of the EU authorities with regard to EU CCPs. In addition, such third-country CCPs are also expected to follow applicable directives of their home authority, whose priorities may not be aligned with those of ESMA in an emergency situation.[16],[17]

Reducing the size of EU counterparties’ exposures to those UK clearing services remains a priority for EU policymakers from a financial stability perspective, together with building well-integrated, resilient clearing markets in the EU. Looking ahead, the development of the EU clearing landscape will be impacted by the EMIR review (“EMIR 3”).[18] EMIR 3 foresees several measures to streamline the supervisory process, to strengthen EU CCP supervision and the requirement for EU clearing participants to clear some OTC IRD and STIR trades through an active account at an EU CCP (“active account requirement”). These measures could contribute to increasing the integration of EU centrally cleared financial markets, boosting competitiveness, reducing reliance on UK CCPs for critical clearing services and improving the resilience of EU CCPs. The active account requirement could benefit euro area CCPs active in the OTC IRD and STIR market, and further foster market-driven initiatives to attract more clearing business to euro area CCPs.[19] The European Commission may take further measures, following an assessment by ESMA of the effectiveness of the active account requirement in terms of substantially reducing reliance on UK CCPs for these clearing services.”