The nature of Black Holes in astrophysics and quantum mechanics is still a mystery and an area of intense research and observation globally, but the nature of these massive interstellar gravitational masses still represents an unsolved mystery to mankind. The recent public discourse around the UK Fiscal deficits has been compared with too easy use of language to Black Holes and frankly, it doesn’t seem particularly wise to overlap economics and astrophysics terms, this creates only confusion. Through language transpires the forma-mentis of those that put forward ideas and comparisons, so to consider the UK Autumn Budget outcomes, in the aftermath can be argued the Exchequer and the OBR, still struggle to understand what is a Black Hole, in economic terms a Debt Black Hole, and still don’t realise the simple factual notion that the increased borrowing can only add to the mass of the Debt Black Hole making the “Black Hole” Bigger. From Economics to Astrophysics the Exchequer and the OBR seem not to have grasped the basic concepts of what they pretended to present with the Autumn Budget, if not a dull Accounting Exercise, which sums eventually only add up more GILTs issuance. Indeed, with plain silliness, depicting the UK Fiscal Deficits as a Black Hole, well that’s not a particularly brilliant comparison, because any intelligible market person can assume, the UK Exchequer’s Fiscal Deficits are inescapable and unserviceable and unsolvable. These idiosyncratic issues have become a feature of the UK since the dreaded word-salad BREXIT was spread and diffused from the mass media and demagogues politicians in the public discourse, the precursor signs of the unfolding UK chaos and Irrationality that anybody, globally, can observe, in that respect also markets, and the recent volatility of GILT yields has been of the same scale as the past October 2022 mini-budget disaster.

This seems to be how the Sovereign Debt market and large institutional investors have perceived this ill-conceived Black Hole misrepresentation of UK Fiscal Deficits, because this adds to the uncertainty of the UK Public Finances’ solidity and Fiscal position, thereby unleashing higher volatility of GILT yields while substantially increasing the cost of borrowing for the same UK Government, while also creating uncertainty also for the Bank of England that observes how markets have deprecated the Bank of England intentions and actions of decreasing Sterling Money Market rates benchmark.

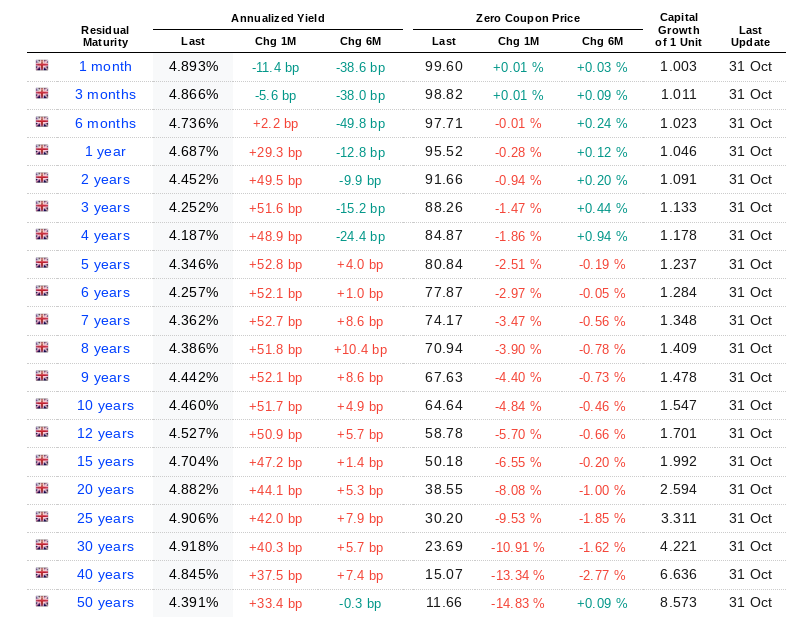

Intraday, on this Halloween market day, GILT Yields have jumped between 10bps to more than 20bps. The yields across different maturities show noticeable increases, with 1-year to 10-year GILTs rising significantly over the past month, and particularly notable increases in the mid-term range (2–10 years), where yields have jumped between 50 and 52 basis points (bp). For longer-term GILTs, such as those maturing in 20 to 50 years, the yields have also risen by about 33 to 44 basis points. However, yields in the 50-year range show a smaller increase of +33.4 bp over the last month, with a relatively minor change over six months, which equates to the amount of interest rate cut brought forward by the Bank of England, which aim should be to align interest rates to a decreasing and normalising Inflation rate.

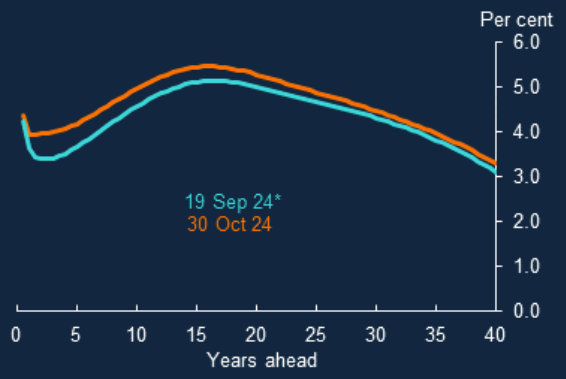

Bank of England chart for the UK instantaneous nominal forward curve (gilts), incorporated a widening spread between September and October, in the forward yield curve sign of Sovereign Debt market investors, discounting a higher term premium in the run-up to the Autumn Budget. This yield curve volatility has been foreseen and justifiable, considering that the 10Y GILT yield of 4.53% is higher by 21bps(0.21%) than the peak of the October 2022 mini-budget 4.32%

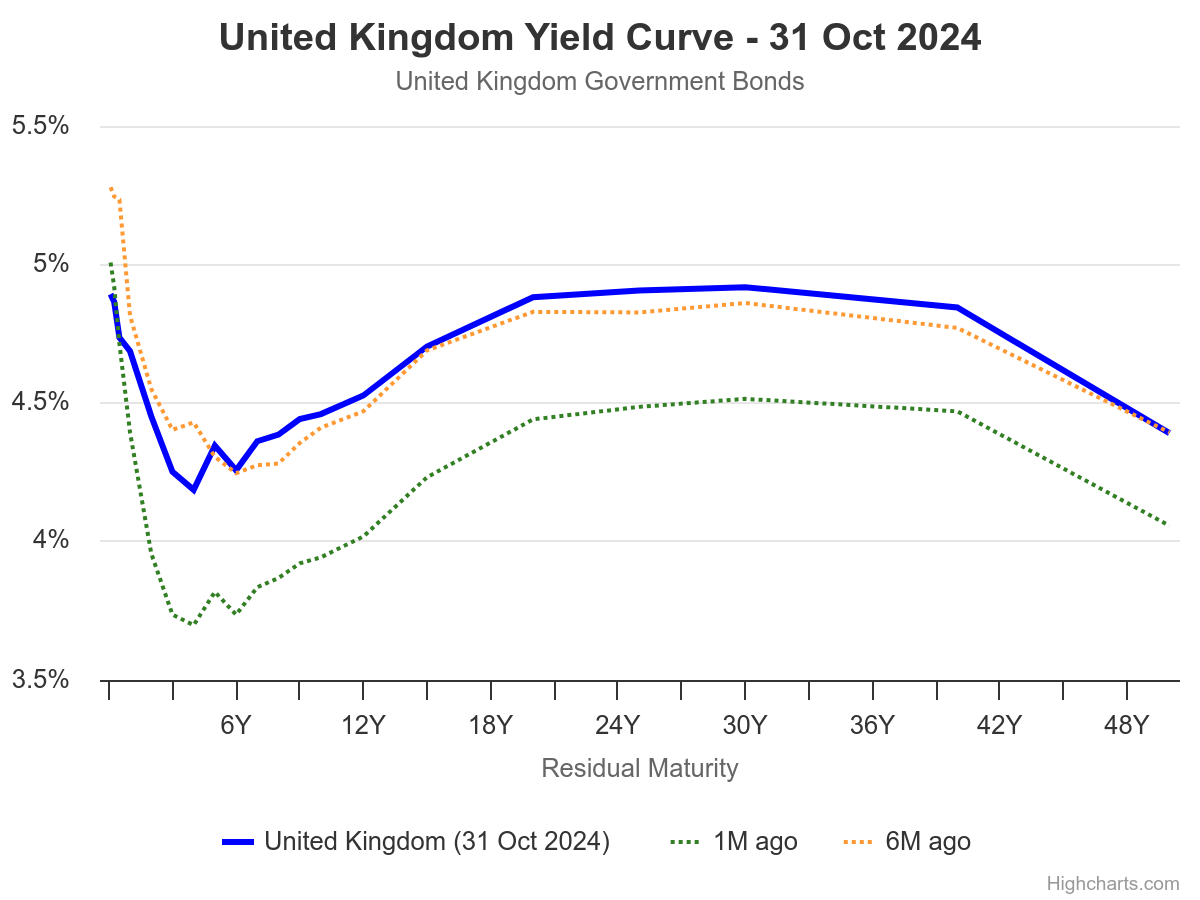

From the chart below and intraday GILT market volatility could be possible to see higher volatility of GILT yields, the 10Y GILT Yield 4.55%, intraday, as the benchmark seems going to drift higher to 5% | 5.5% in a volatility shock, considering the very large amount of borrowing, bond market investors and institutional investors seem to aim for higher term premium given the interest rate risk and price sensitivity of holding longer duration bonds.

Factors unleashing GILT market volatility

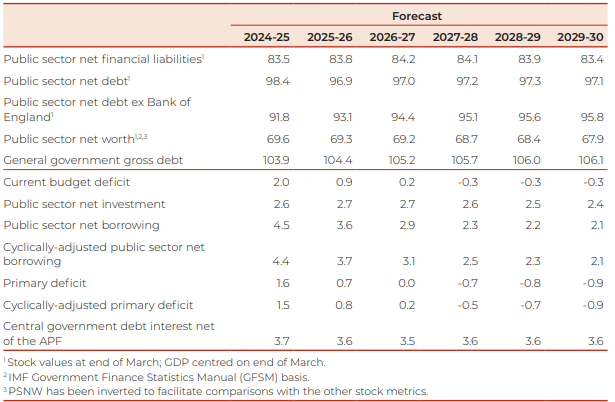

The Autumn Budget forecasted a budget deficit of £55.5 billion for 2024-25, marking an increase over previous estimates. With PSNB (Public Sector Net Borrowing) expected to peak at £127.5 billion (4.5% of GDP) in 2024-25, there is a significant upward adjustment in borrowing needs. This increased borrowing has directly impacted the yield environment, as investors demand higher returns to compensate for the perceived rise in risk associated with the government’s fiscal position and the expectation of more substantial bond issuance to finance this deficit. Short-term volatility in GILT yields reflects market concerns over the sustainability of inflation control, with yields on shorter maturities rising as the MPC’s actions to raise rates are anticipated to impact the short-term end of the yield curve.

Debt Management Office (DMO) increasing Financing Requirements:

With the DMO’s financing requirement rising to £299.9 billion for 2024-25, largely through gilt sales, the resulting higher supply of GILTs has put additional pressure on yields to rise, especially as investors adjust to increased issuance. The capital growth figures for each maturity (i.e., capital loss for holders) illustrate the impact, with steep price declines across maturities, particularly in longer-term bonds, which have a higher sensitivity to rate changes (as shown by 30-year GILT prices falling nearly 11% in the past month). Interest rate risk becomes a concern as the UK’s borrowing needs increase amid an environment of elevated and potentially rising yields. When interest rates rise, the market value of existing gilts decreases, resulting in marked-to-market losses for investors holding these bonds at previously lower rates. This price sensitivity is especially pronounced for longer-duration gilts, which are more vulnerable to interest rate shifts. As the Autumn Budget reveals higher borrowing projections, investors may anticipate additional rate hikes, either by the Bank of England to curb inflation or as a market response to increased debt supply, further amplifying volatility.

The volatility in UK GILT yields, driven by heightened borrowing and fiscal pressures, raises the risk of volatility across global bond markets, particularly those in developed economies with similar debt profiles. As yields rise in the UK, international investors may adjust their portfolios in response to perceived risks, selling off UK bonds and reallocating to safer assets or other markets. This shift could amplify volatility across other sovereign debt markets, especially in Europe and the United States, where similar fiscal challenges exist due to post-pandemic recovery spending and inflationary pressures. Furthermore, the rapid adjustments in UK GILT yields could influence the broader interest rate environment, as markets reassess the creditworthiness of government debt in light of rising deficits and inflation control uncertainties. Should this trend continue, it could lead to higher borrowing costs globally, impacting both public and corporate debt. Emerging markets, often sensitive to shifts in global interest rates, may also face heightened borrowing costs and capital outflows as investors seek higher yields in perceived “safe haven” assets, exacerbating fiscal and inflationary challenges in those economies.