Dynamic Interactions Between Macroeconomic Variables: Evidence from VAR Forecasting Models

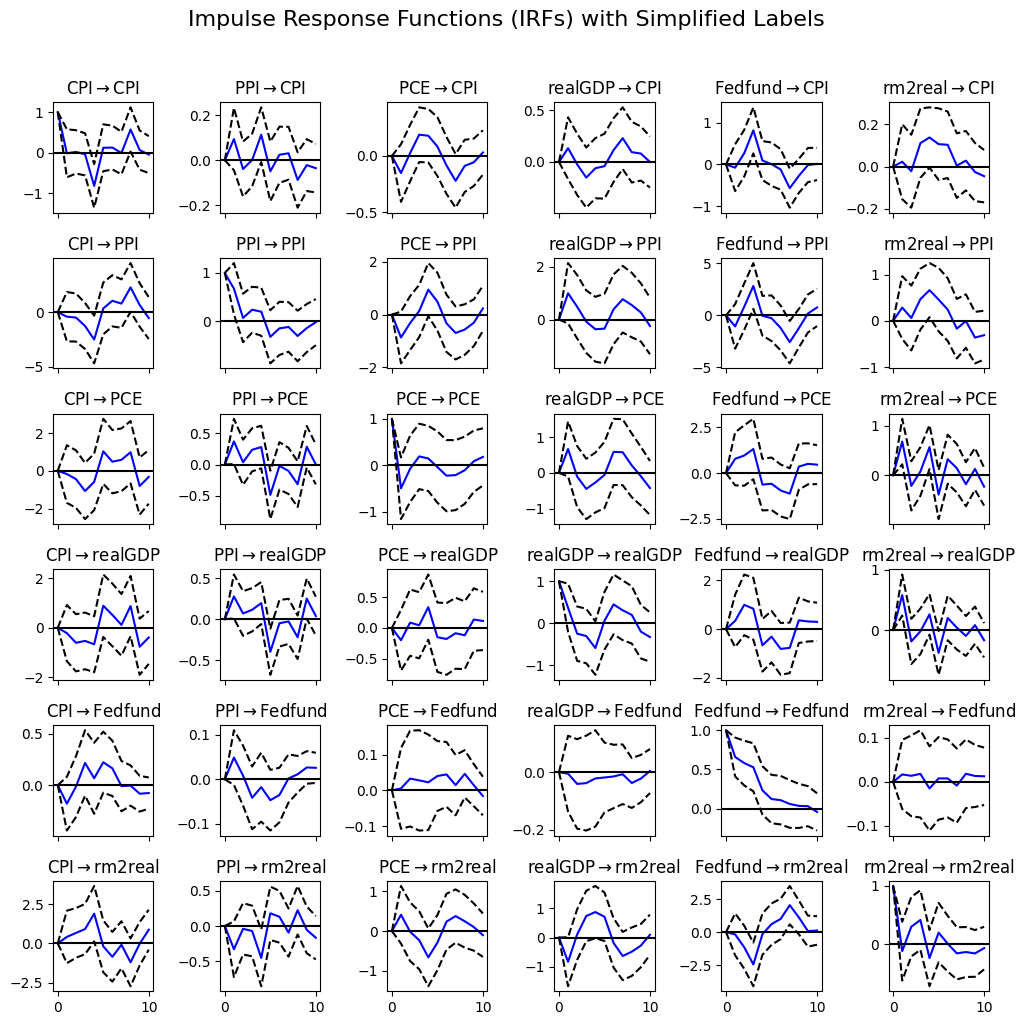

In this article the readers can find theoretical econometric research about the dynamic relationships between macroeconomic indicators, including inflation, interest rates, and real GDP, using Vector Autoregression (VAR) models and ARIMA forecasts. Through impulse response functions (IRFs) and forecast error…

Econometrics research of CPIH Volatility Inference with Interest Rate Volatility

The British economy, as well as many other developed economies, has structural inflation issues that are not correlated to wages, quite the opposite, average annual incomes in the past 34 years haven’t kept pace with inflation, making real income unable…

How the USA economy could perform in the coming quarters ?

Latest Q1 data from the USA economy have seen a decrease in the rate of GDP expansion in Q1 correlated with a decrease in PCE, consumer spending, while Inflation data have slightly increased with Initial Jobless claims also increasing as…