Latest Q1 data from the USA economy have seen a decrease in the rate of GDP expansion in Q1 correlated with a decrease in PCE, consumer spending, while Inflation data have slightly increased with Initial Jobless claims also increasing as a sign of an economy that has expanded and overheated during 2023, and 2024 economic year shows sign of Consumer Spending deceleration while Inflation trends above the 2.0% Federal Reserve price stability aim.

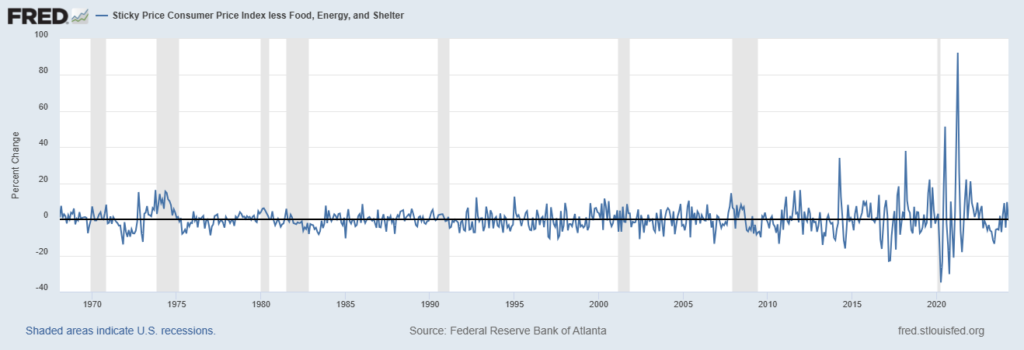

In Q1, the first three months of 2024, the United States economy has grown by 1.3%, decreasing the rate of expansion from 3.4% in Q4 2023. Observing Inflation data there are signs of an overheating economy that has expanded mainly with the growth of prices, Inflated, in 2024 Economic growth could be decreasing, while inflation in Q1 was 3.4%, Core Inflation 3.6%, Core PCE Prices 3.6% important inflation parameter for monetary policy decision-making, Core PCE Index 2.8%, PCE Prices 3.3%, overall Core PCE Prices growth sits in a range between 3.3%|3.6%, while consumer spending and Aggregate Demand could be growing at a pace less than prices. Another observed measure of Core Inflation, less volatile price components such as Food, Energy, and Shelter, jumped +9.5% month on month back in March and averaged 3.1% in April year on year, other data that signal prices for Core Services have been increasing in the United States above wage growth and demand could be slowly decreasing in 2024, considering also the Presidential election cycle as a transition year for the United States economy.

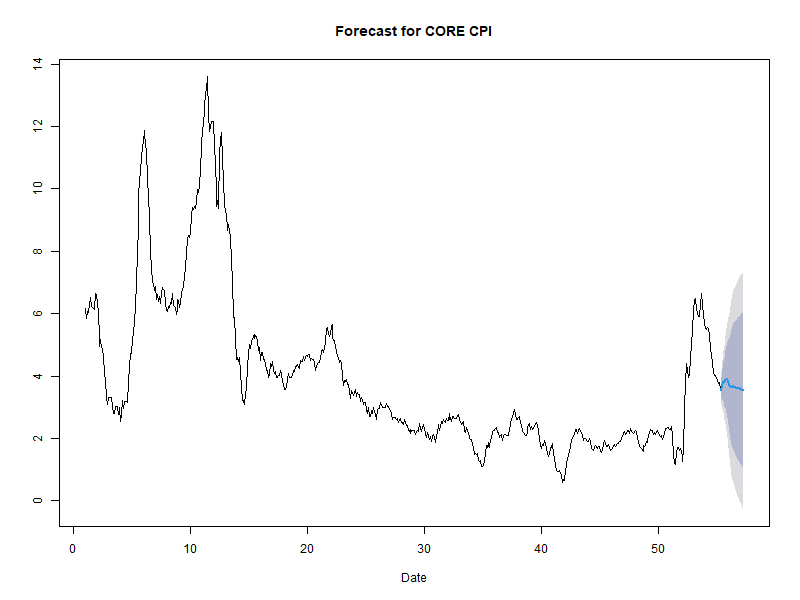

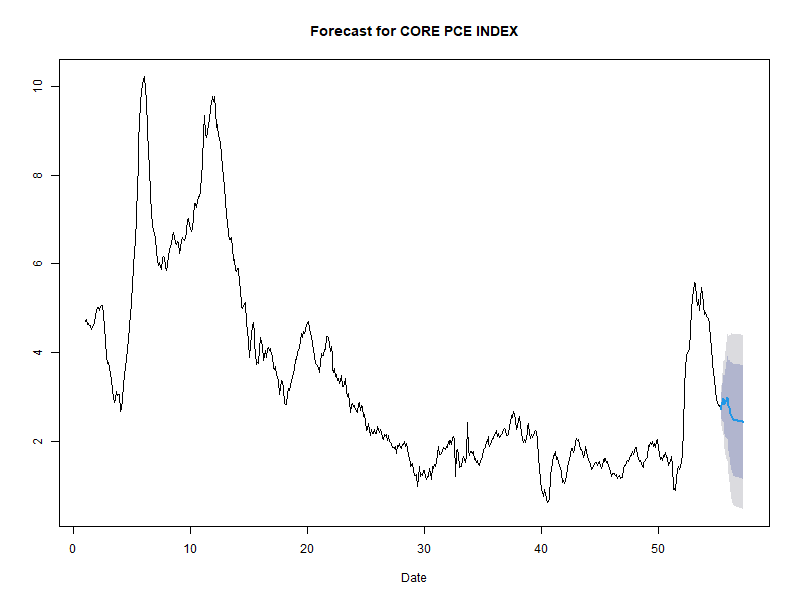

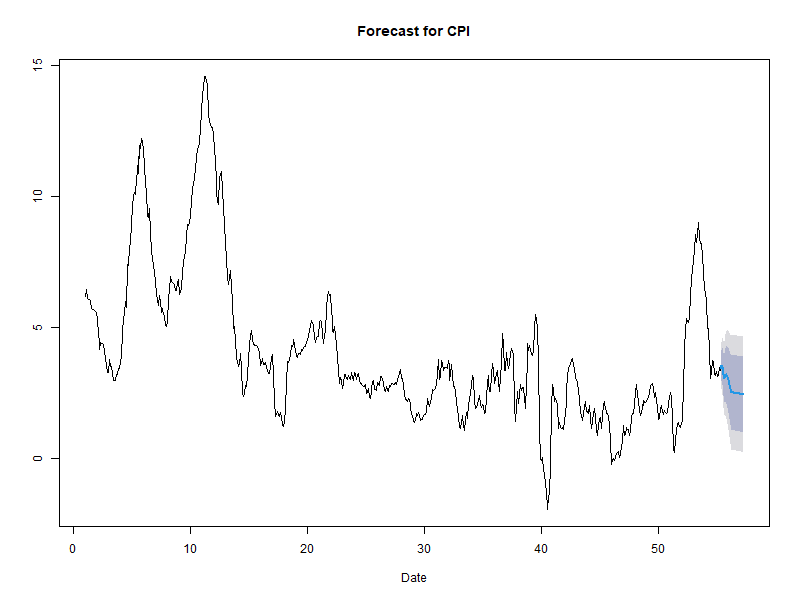

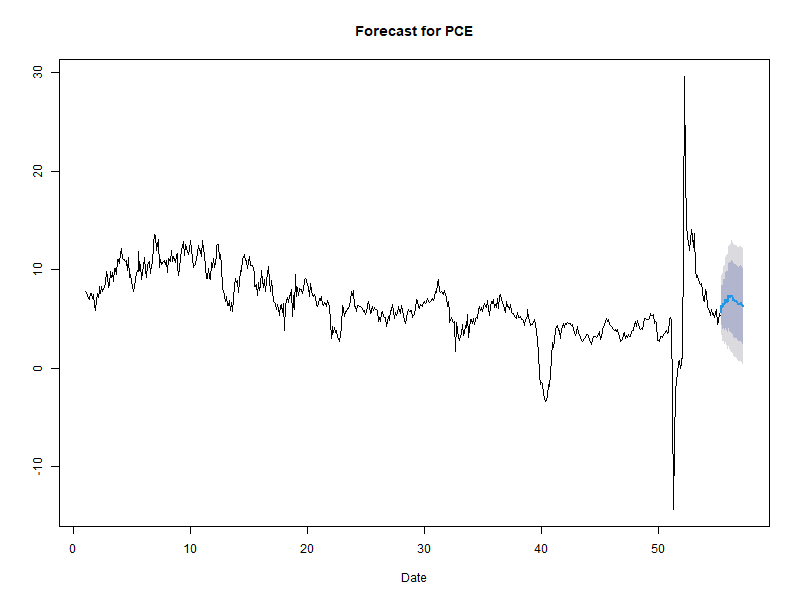

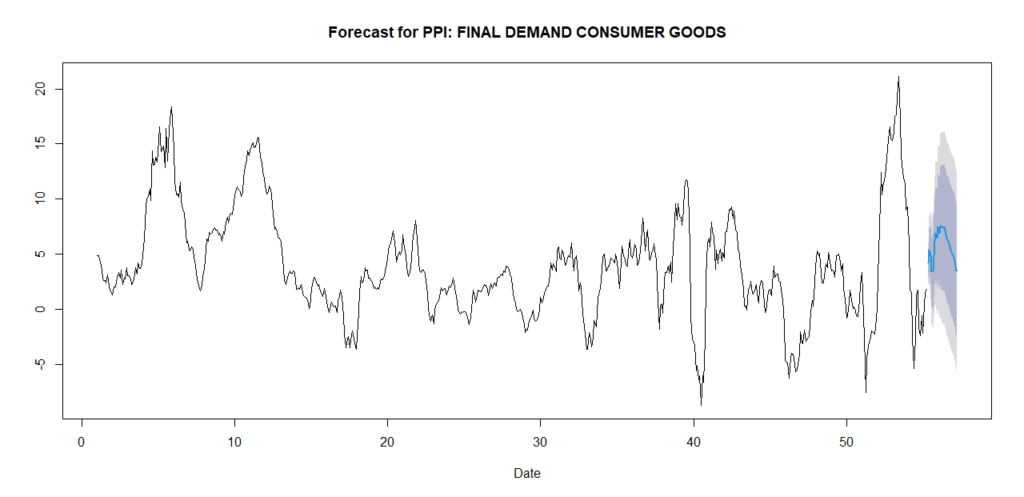

In order to elaborate a macroeconomic forecast of the United States economy two parallel studies have been performed, one research has been performed with a VAR, lags(1/4) and 8 quarters ahead forecast, taking into study main economic data time-series, of Q1 GDP data. Indeed, additional research has been performed on a basket of Inflation measures, with monthly data frequency, and a variety of volatility models have been applied, where ARIMA(1,0,1) and ARIMA(1,1,1) have been utilized to extract a 12 months and more accurate 24months forecast of Inflation trends.

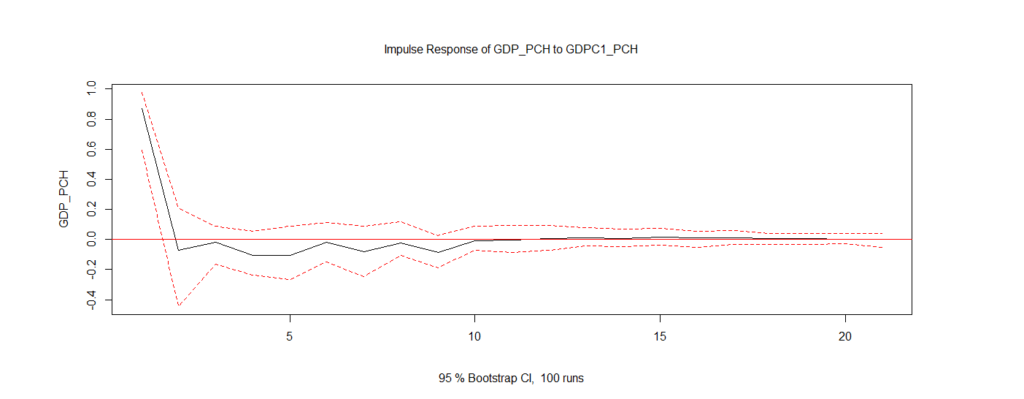

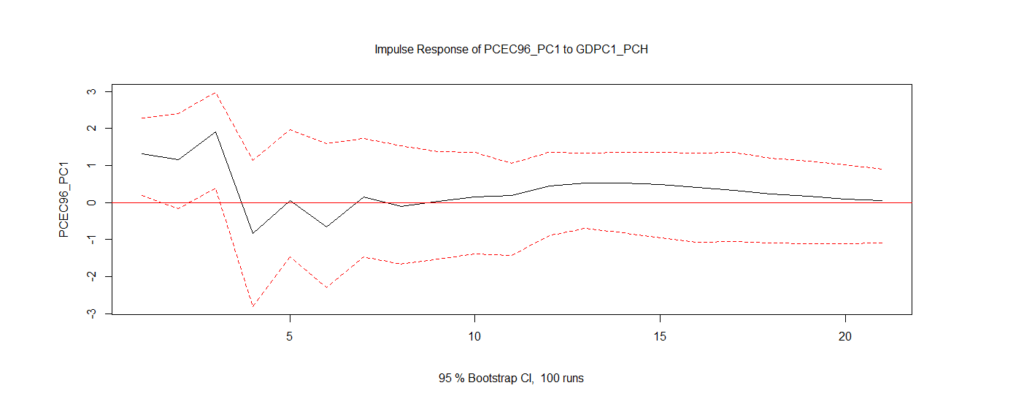

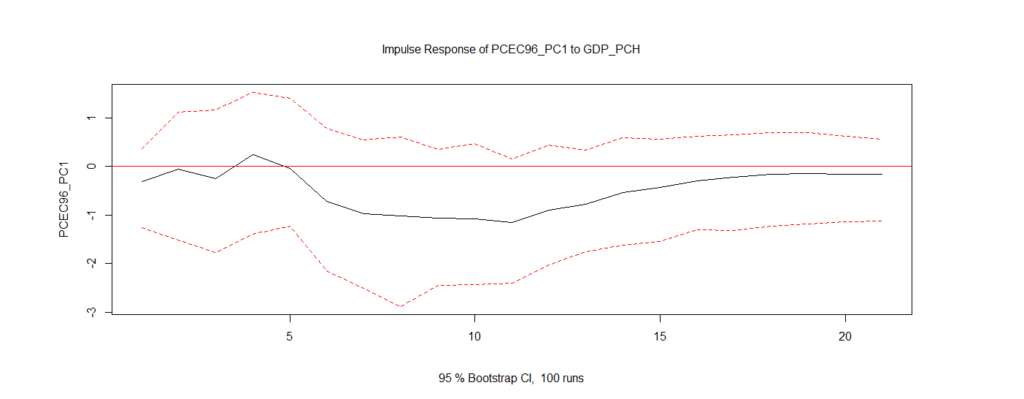

VAR Forecast of GDP| Real GDP, impulse response function explains how the Q1 economic growth deceleration could in fact become 1 standard deviation that could imply Real GDP growth to decrease, considering the Growth of Prices above the Real Growth of Aggregate Economic Output.

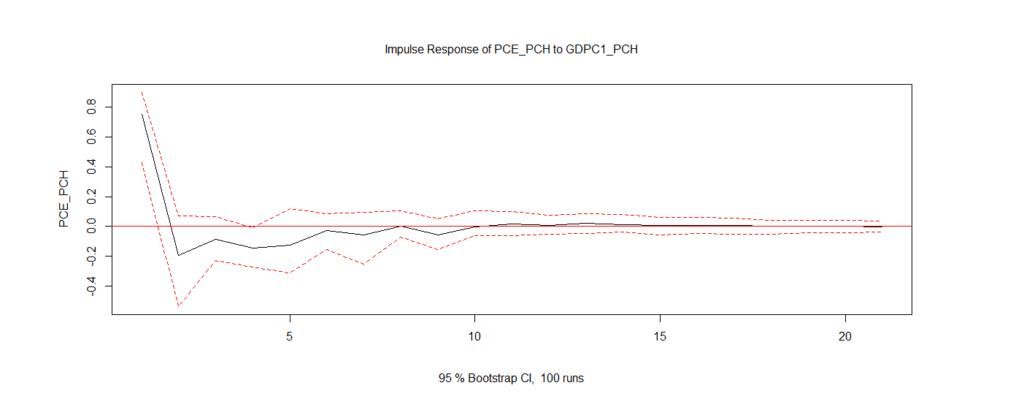

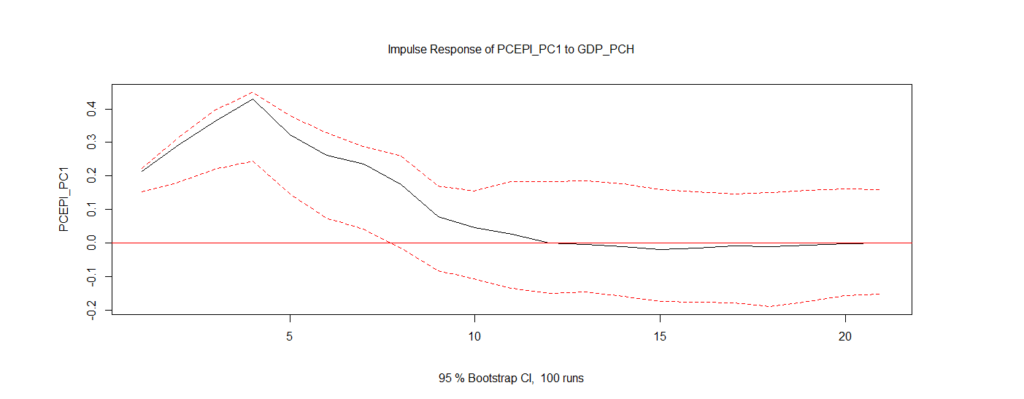

Core PCE Expenditure also forecasts a 1 standard deviation impulse that could then feed into Real GDP data with slowing economic growth in the coming quarters.

In fact, the VAR Forecast elaborates a decrease in Core Personal Consumption Expenditure that could produce a -1 standard deviation response in Real GDP Growth, in the United States economy, another data that hints at persistent higher Prices feeding into a marked decrease in Consumer Spending that would then see a slowdown in GDP growth.

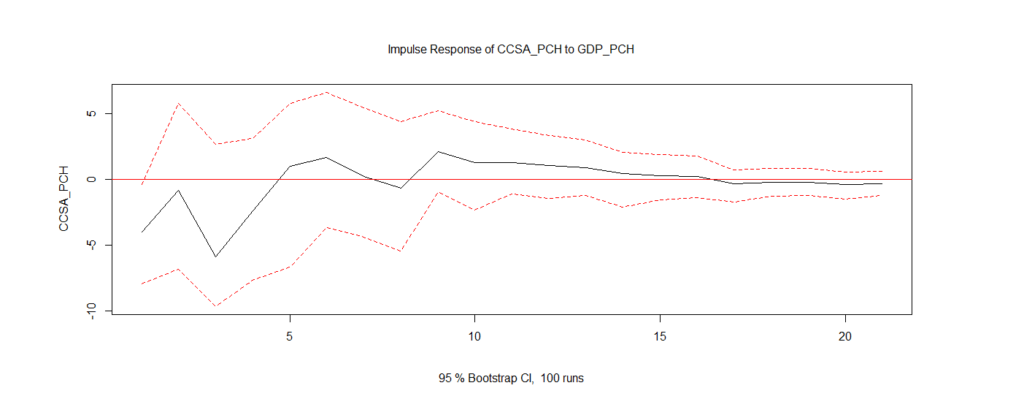

With Personal Consumption Expenditure decreasing with the expansion of GDP growth, another factor could be Jobless claims rising, in the graph below a 5 standard deviation increase in Jobless claims, feeding into economic growth slowdown.

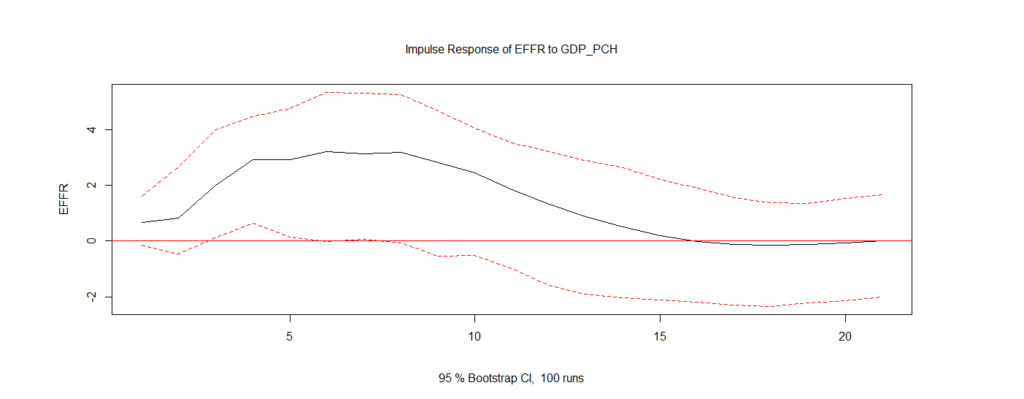

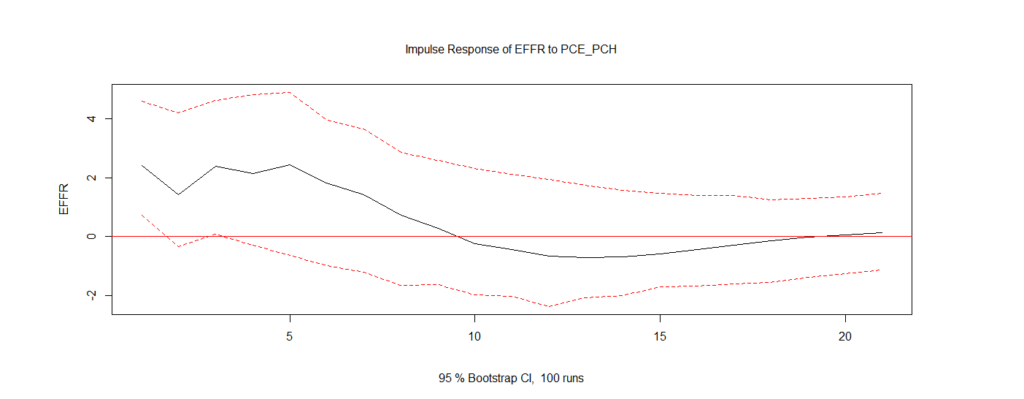

In fact, within the next 5 coming quarters, the Effective Federal Fund Rate could start to decrease and see the first Interest Rate cuts on U.S. Dollar money markets, as GDP Economic Growth and Personal Consumption Expenditure will decrease, with the Federal Reserve beginning to decrease Interest Rates in an economic slowdown, while Inflation could not be completely converged on 2.0% target.

ARIMA Forecast of Inflation, PCE and Consumer Demand elaborate an increase of Inflation measures, to then align with a sharp decrease in Consumer Spending and Consumption Demand that will then feed into a significant decrease in the Economic Growth of the United States, as of now, flat-lining or negative economic growth quarters can’t be excluded in the macroeconomic picture for the United States and the global economy, in order to see Monetary policy shift and interest rates decreasing.

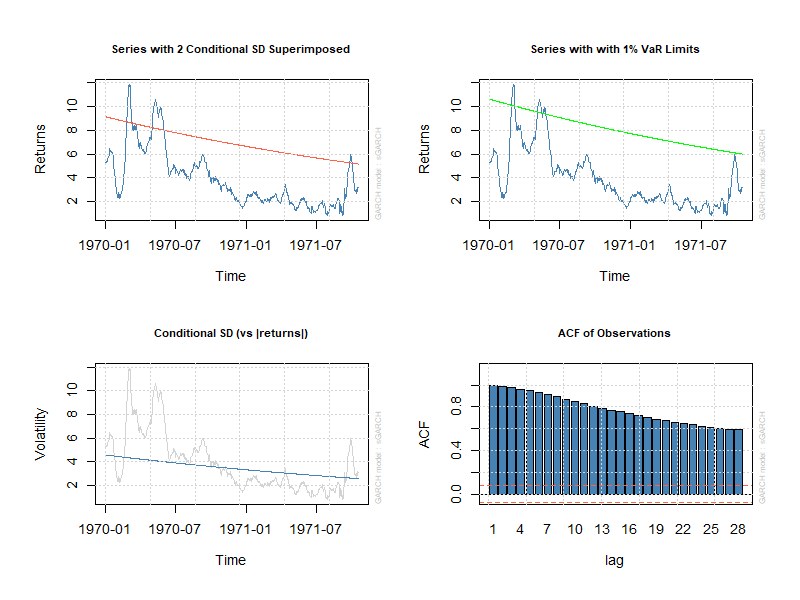

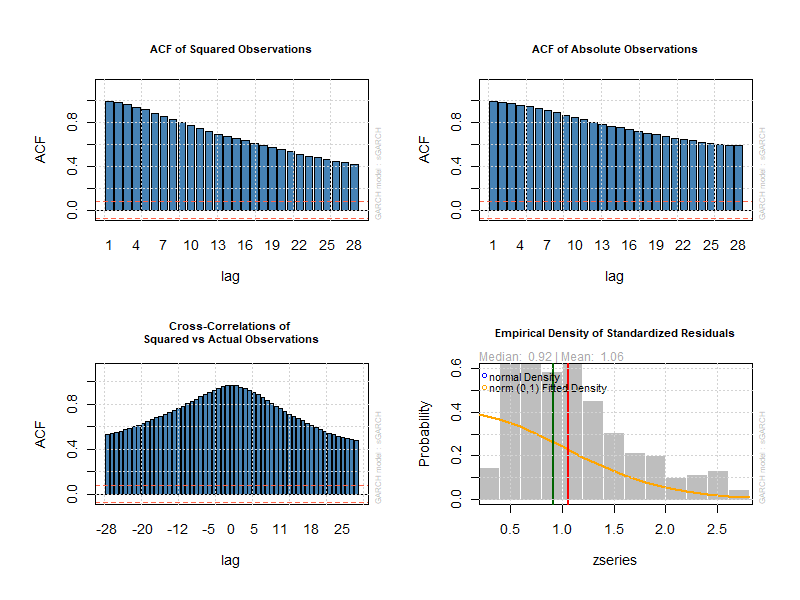

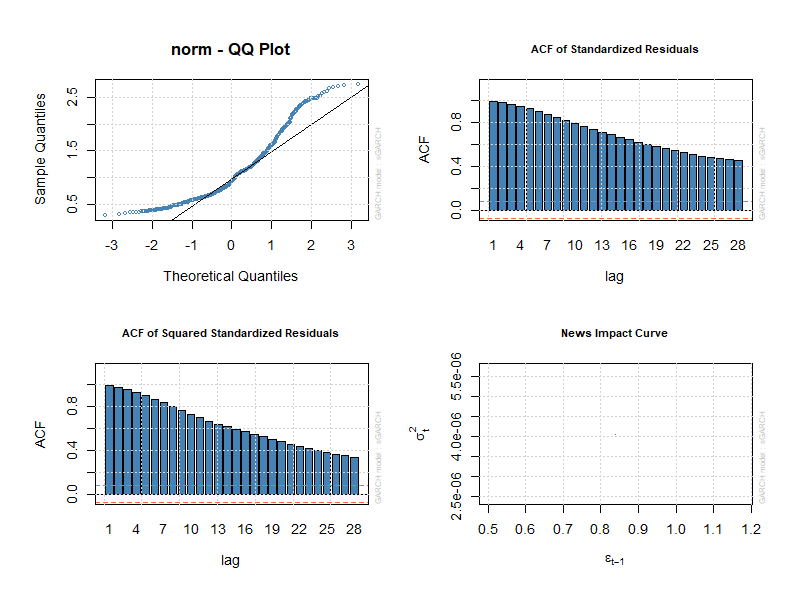

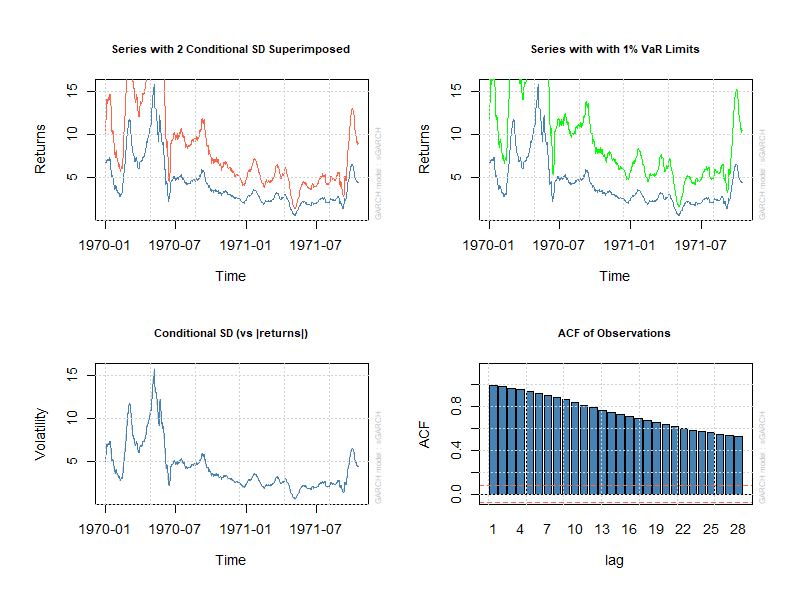

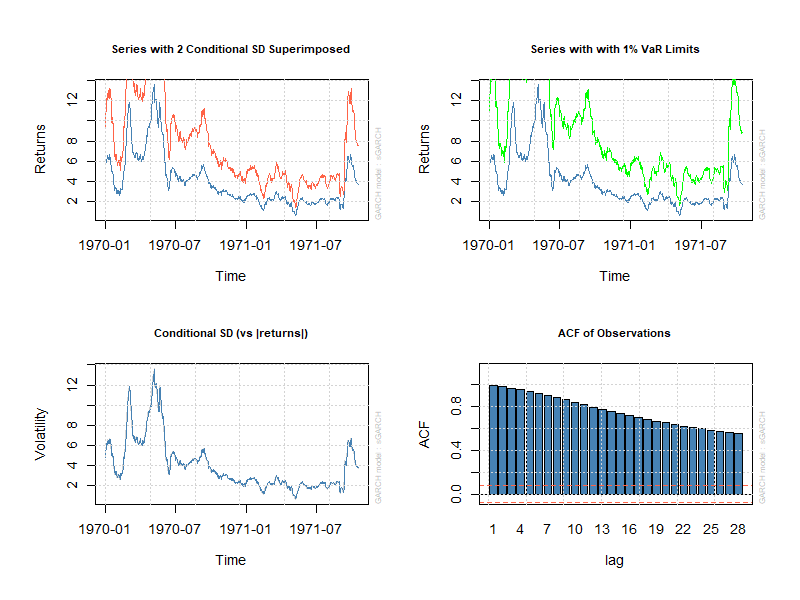

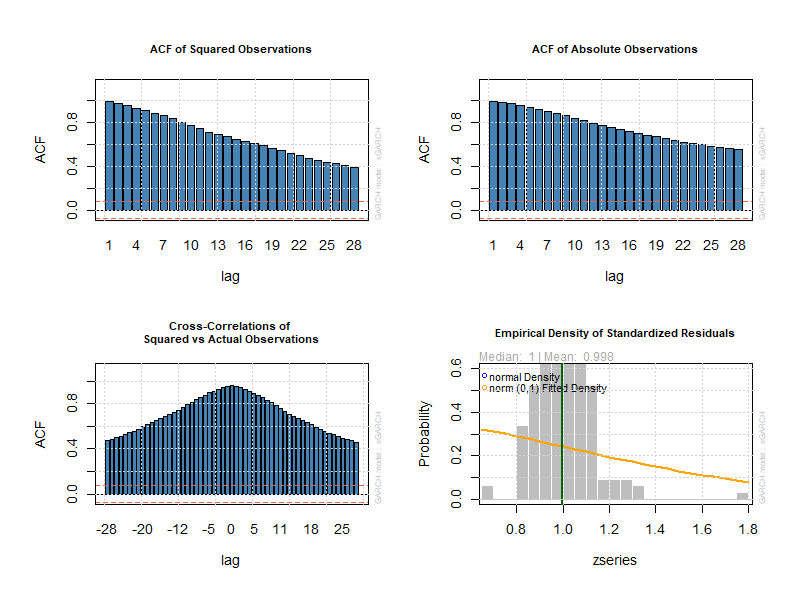

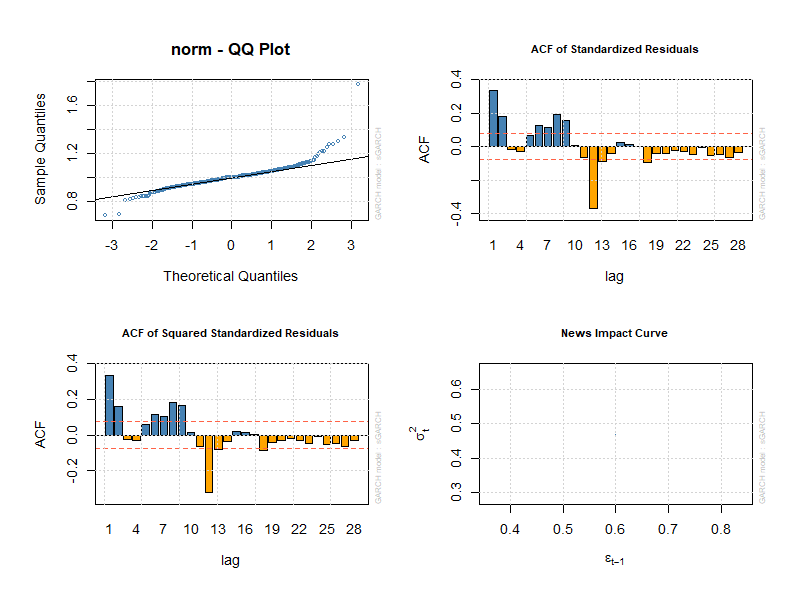

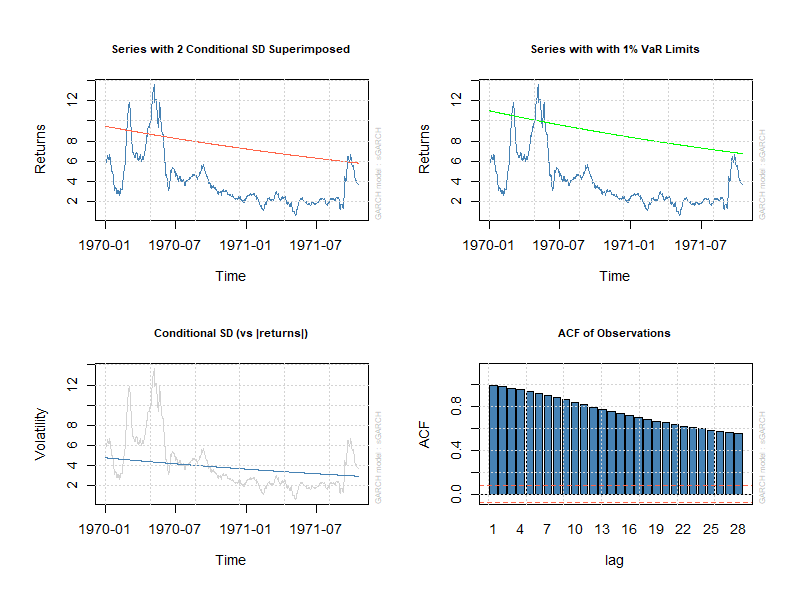

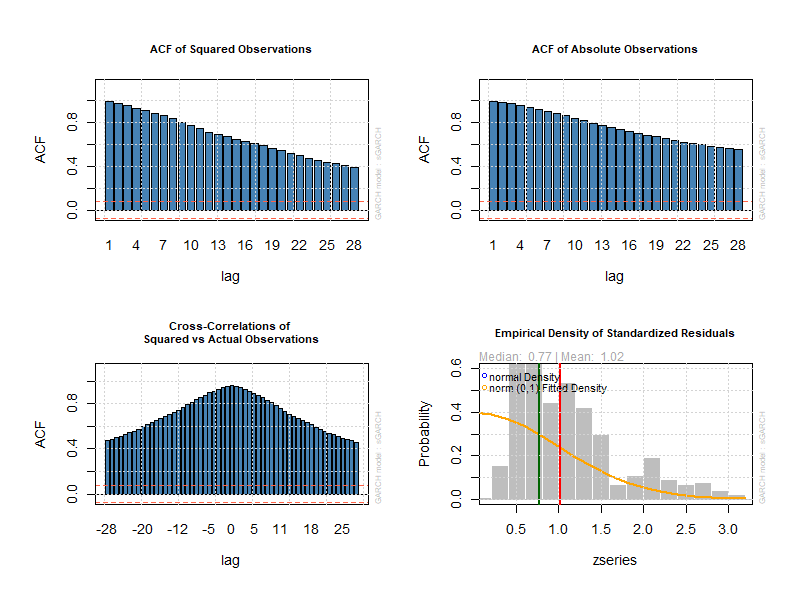

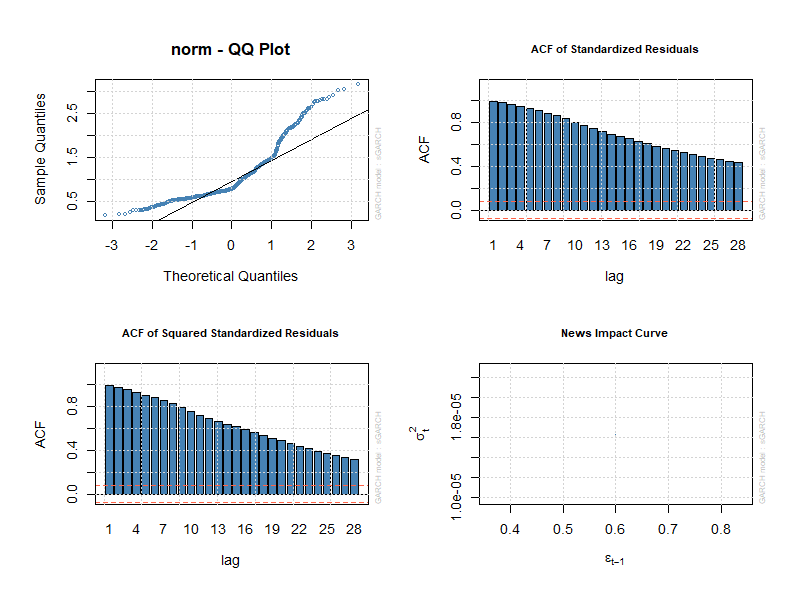

CORE STICKY Generalized Autoregressive Conditional Heteroskedasticity (1,1) MODEL

CORE CPI Generalized Autoregressive Conditional Heteroskedasticity (1,1) MODEL

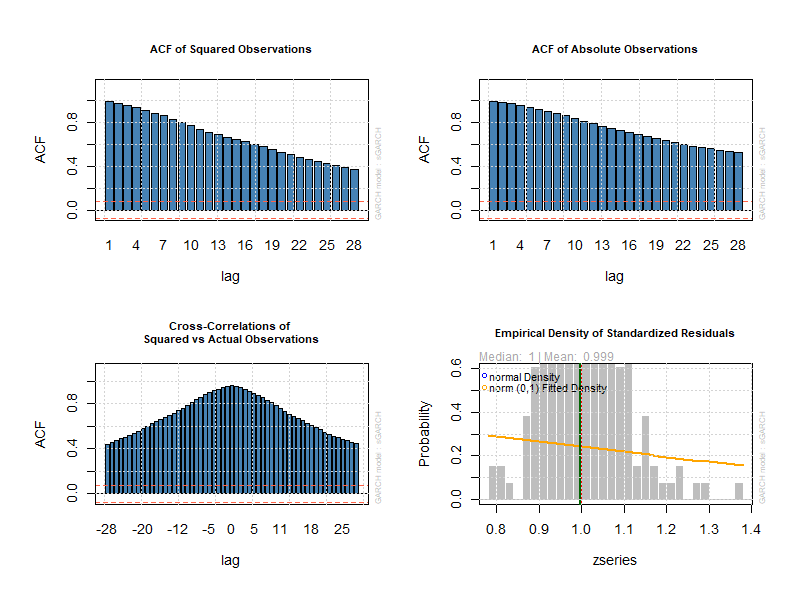

ARCH CORE CPI

ARCH, CORE STICY LESS FOOD AND ENERGY