Several banks, including Zion Bancorp, Western Alliance Bancorp, Citizens Financial Group, KeyCorp, TR Financial, Andidon Bank Shares, Regions Financial, and Cam View, have seen their market values decrease. A primary issue contributing to this situation is the recent increase in the repo rate, in the aftermath shockwaves of the recent bankruptcies of auto industry firms First Brands and Tricolour, as factors of concern.

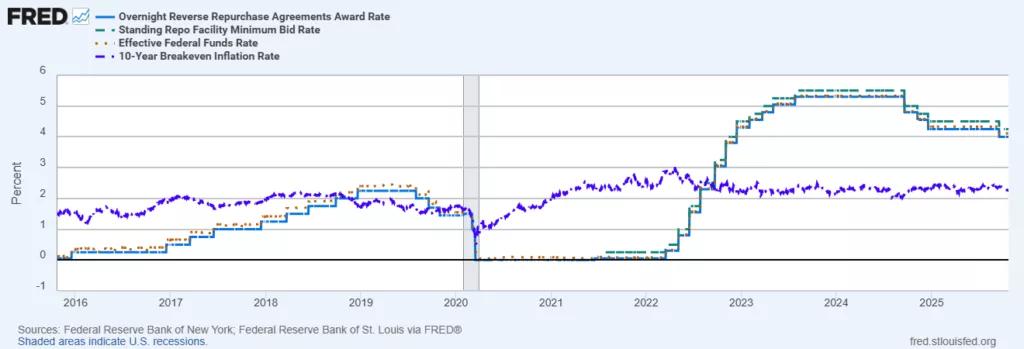

The repo rate currently hovers around 4.25%−4.3%, with potential spikes to 4.4% or 4.5%, maintaining a slight markup spread over the Fed fund rate of 4.1%. The 10-year Treasury yield is on a downward trajectory, falling below the Fed fund rate, which signifies an inverted yield curve. This inverted yield curve serves as a recessionary signal in the market, suggesting that the federal funds rate is expected to decrease in upcoming quarters due to anticipated slower long-term economic growth (around 3.8% plus inflation). An inverted yield curve indicates a general economic slowdown, short-term liquidity distress, and a deceleration of economic growth.

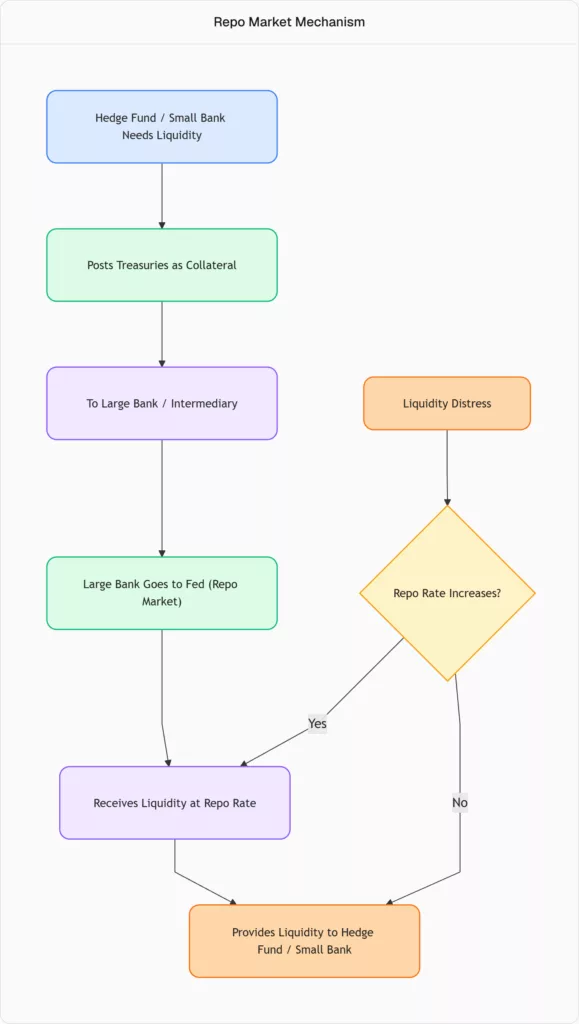

Market Dynamics: Collateral Demand and Liquidity Distress

The repo rate rises as the Federal Reserve demands a higher premium from banks for overnight or short-term liquidity. Investors are increasing their purchases of longer-duration debt, such as 10-year Treasuries, which can be a strategic move in the repo/reverse repo market or a reflection of concerns about economic growth. Banks may acquire Treasuries to inject liquidity into the repo market, utilising them as collateral to secure liquidity for smaller investment funds or hedge funds. The repo rate has exhibited volatility, recently climbing to 4.36% from an earlier level of approximately 4.25%. When the repo rate (4.36%) is significantly higher than the 10-year Treasury yield (3.95%), it implies that short-term liquidity is perceived as riskier than long-term Treasury debt, signalling market distress and liquidity distress. In conditions of market distress, the yield on collateral can surge if there is an urgent need for liquidity, compelling entities like small regional banks to sell their liquid assets (Treasuries), thereby driving yields upward. Large banks can capitalise on the 40 basis point spread between the repo rate and the 10-year Treasury yield by purchasing Treasuries and actively participating in the repo market. The liquidation of gold in the open market indicates liquidity distress, while the repo market addresses overnight liquidity shortfalls.

Zion Bancorp: Credit Exposure and Balance Sheet Concerns

Zion Bancorp’s stock experienced a 10% drop. Its current capital ratio of 10% is considered adequate but falls below the recommended 11%−12% for banks deemed “well-capitalised” (the minimum for regional banks is 6.5%. The bank’s total credit risk exposure stands at $110.861billion. This exposure is comprised of: Loans and leases: $59.6 billion. Unfunded lending commitments: $29.5 billion, suggesting the bank is rapidly depleting its cash reserves. Commercial real estate (CRE) lending: $13.5 billion. Total commercial lending: $31 billion. Consumer credit: $15.3 billion. Home equity credit lines (HELOCs): $3.6 billion. Mortgages: $10.3 billion. Credit cards: $472 million.

Off-balance sheet exposures include $7.9 billion in unusual commitments that are not consolidated into the total credit exposure, representing a potentially high-risk aspect of their financial reporting. The bank’s credit exposure spans geographically across Arizona, California, Colorado, Nevada, Texas, Utah, Washington, Oregon, and other states. Liquidity distress emerges when clients default on commercial real estate loans, credit card payments, or home equity lines, compelling the bank to utilise the repo market to balance its books daily. The stress tests and stated capital ratio figures for Zion Bancorp are believed to be inaccurate, as they do not adequately reflect the potential magnitude of losses from credit exposure.

Jefferies Financial Group: Repo Market Reliance and Liquidity Risk

Jefferies Financial Group’s stock also declined by 10%. As an investment bank, Jefferies extensively uses the repo market, with exposure of $12 billion or more in securities sold under repurchase agreements. They require consistent access to the repo market for liquidity, potentially needing up to $12 billion or $18 billion for their operations. Jefferies offers brokerage services and provides liquidity to hedge funds, engaging in speculative market activities and trading various derivatives (e.g., commodity swaps, credit default swaps). The high cost of refinancing through the repo market (at 4.36%) places a strain on their day-to-day operational margins. A significant funding issue could arise if counterparties refuse to roll over the $18 billion repo agreements, potentially leading to a severe liquidity shortfall and possible insolvency for Jefferies. Their heavy dependence on the repo market creates a liquidity risk, especially given a net negative position of approximately $5.9 billion between their repo and reverse repo activities. This reliance on risky repo/reverse repo transactions establishes a “circle of money” where liquidity problems in one segment can trigger ripple effects across the overnight funding market, consequently affecting stock prices.

Western Alliance Bancorp: Mortgage Business, Asset Valuation, and Cash Burn

Western Alliance Bancorp is deeply involved in the mortgage business and is characterised by its rapid depletion of cash, with its stock value potentially falling to zero. The bank operates through a complex network of small entities and divisions specialising in providing credit within the real estate market (e.g., mortgages, insurance, and properties in Las Vegas). They engage in purchasing, originating, repackaging, and reselling loans, including mortgages, and also hold these assets for investment. Western Alliance maintains minimal provisions for credit losses, despite holding billions in credit exposure and valuing assets (such as mortgage-backed securities) as AAA, even when their actual market value is considerably lower. Their cash flow analysis reveals substantial net losses from investment activities (e.g., $5.5 billion) and operating activities (e.g., $22 billion loss, with $11 billion losses in previous years). The bank is escalating its risk profile by increasing its holdings of available-for-sale residential mortgage-backed securities ($17.5 billion, up from $14 billion the prior year), including those rated AAA by federal agencies. Significant credit exposure in commercial real estate includes $6.5 billion in non-owner-occupied properties, which are deemed very risky due to reliance on intermediaries and a lack of productive economic activity. Total past-due loans currently stand at $720 million, a figure likely to increase, further underscoring the inadequacy of their $395 million allowance for credit losses against a $55.5 billion investment portfolio. The continuous practice of securitising mortgages and other credit products, despite consistent financial losses, suggests a failure to learn from previous financial crises. Customers with checking accounts at Western Alliance Bancorp are advised to withdraw their funds immediately, although FDIC guarantees cover up to $250,000.

- CONSTITUTIONAL ASYMMETRY, ECONOMIC DEPENDENCY,AND THE CASE FOR NATIONAL SELF-DETERMINATION

- The Necessity of a United Nations HQ Relocation to the Hague with a Permanent Nuremberg Tribunal.The Impunity Crisis of Rogue Governments

- The Digital Job Posting Bubble: Quantifying Phantom Demand in Online Labor Markets

- United States Criminality and Impunity: Historical-Sociological Perspective of United States Unaccountability and Impunity at the behest of International Law

- What Everyone Gets Wrong About Inflation: 5 Surprising Economic Data