Your Old China plates’ economy presents a mixed picture for the third quarter, characterised by robust industrial performance and steady GDP growth, but held back by persistent weaknesses in investment and the property market.

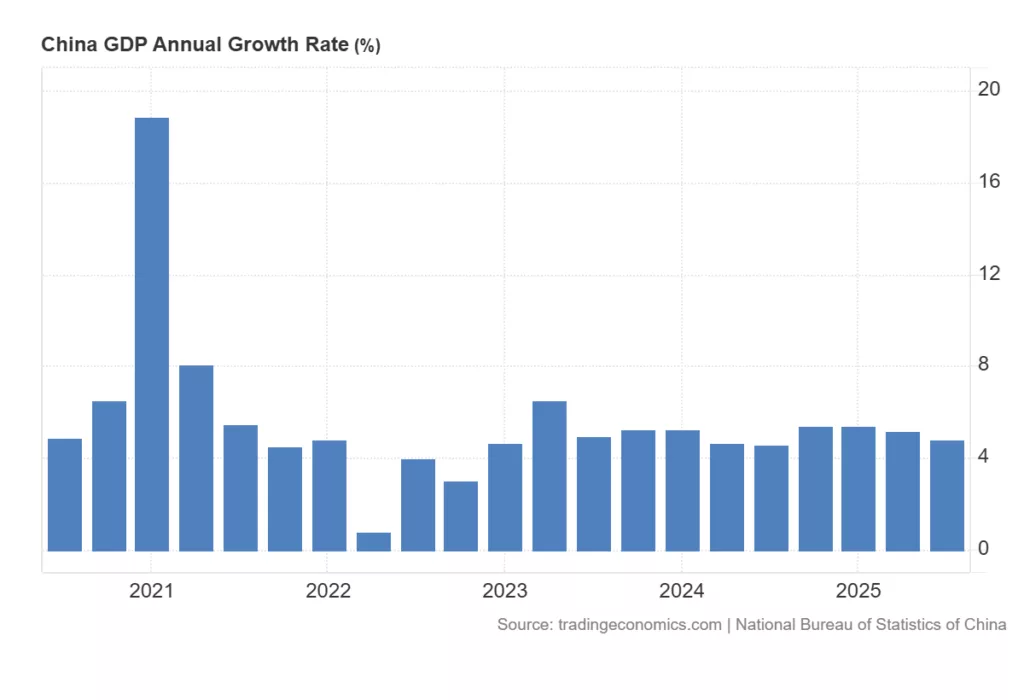

The economy grew at a year-on-year rate of 4.8% in Q3, slightly exceeding the consensus of 4.8%, though this represents a deceleration from the previous 5.2%.

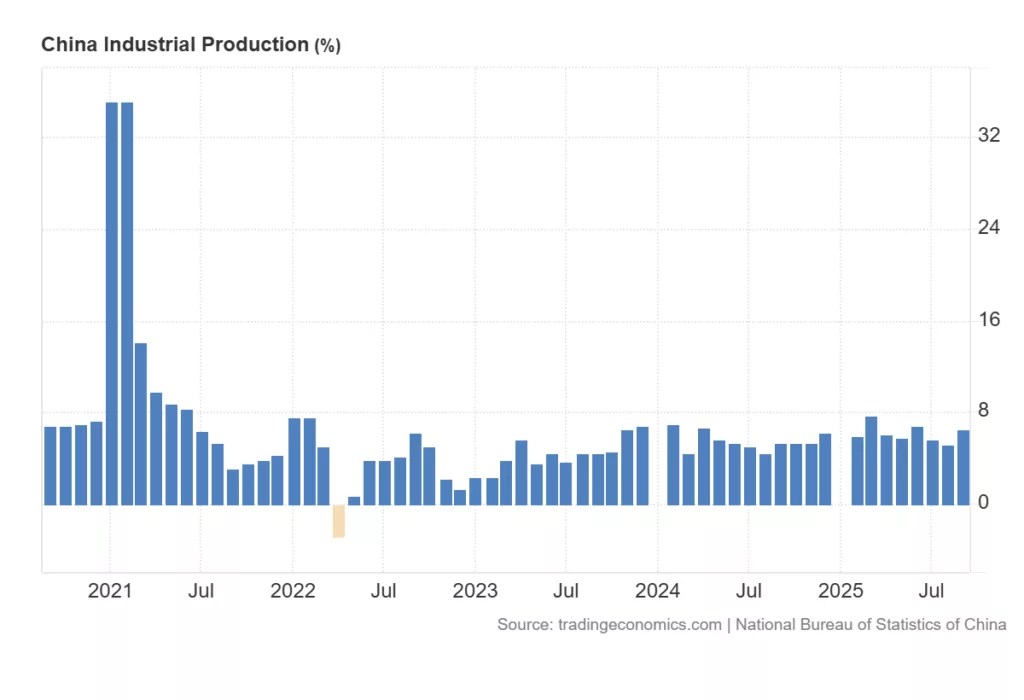

A key bright spot was Industrial Production, which surged to 6.5% year-on-year in September, significantly beating forecasts and indicating strong factory output. However, this industrial strength contrasts sharply with other sectors.

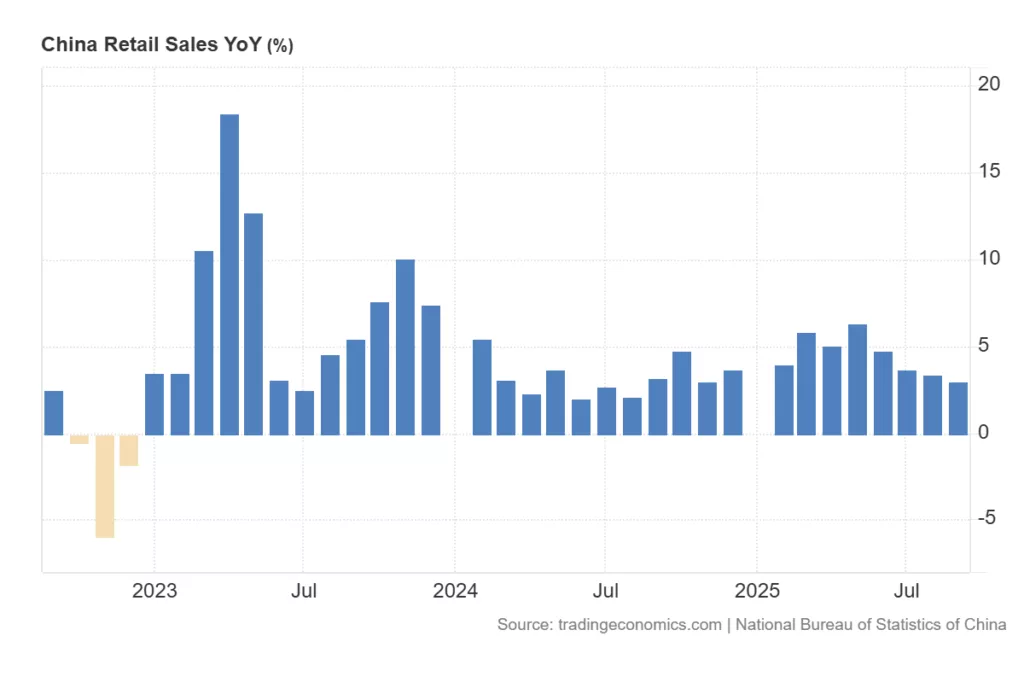

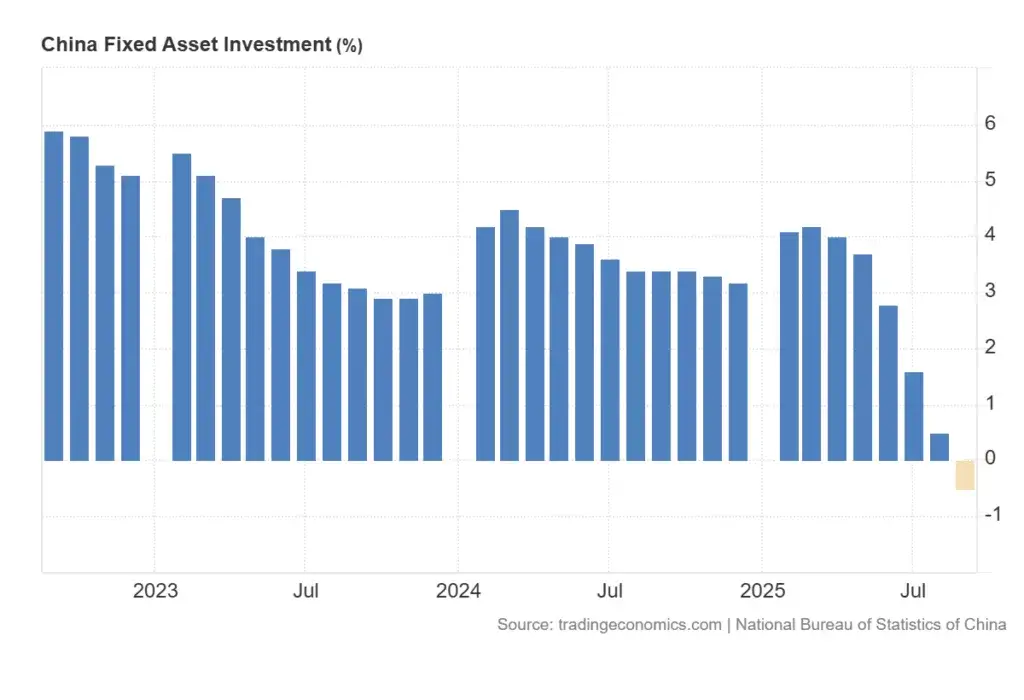

Fixed Asset Investment turned negative for the first time in the available data, recording -0.5% growth year-to-date, which points to a significant pullback in capital expenditure. Consumer spending also showed signs of softening, with Retail Sales growth slowing to 3.0% year-on-year in September.

The data also reveals ongoing challenges in the real estate sector, with the House Price Index falling -2.2% in September from a year earlier. In response to these mixed conditions, the People’s Bank of China (PBoC) has maintained an accommodative monetary policy, keeping the 1-year and 5-year Loan Prime Rates (LPR) steady at 3.0% and 3.5% respectively, continuing its support for borrowing and economic activity.

Most Important Macro-Data Points This Week

| Data Point | Region | Date | Key Focus & Potential Market Impact | |

|---|---|---|---|---|

| GDP, Industrial Production & Retail Sales | China | Monday, Oct 20 | Focus: Health of the world’s second-largest economy. Impact: Strong data could boost global commodity currencies (AUD, NZD) and equities; weak data may trigger risk-off sentiment. | China Retail Sales |

| Consumer Price Index (CPI) | Canada | Tuesday, Oct 21 | Focus: Bank of Canada (BoC) inflation path. Impact: Higher-than-expected inflation could strengthen the CAD and put pressure on the BoC to maintain a hawkish stance. | Canada Inflation Rate |

| Consumer Price Index (CPI) | United Kingdom | Wednesday, Oct 22 | Focus: Bank of England (BoE) policy path. Impact: A high print may force the BoE to keep rates higher for longer, supporting the British Pound (GBP). | United Kingdom Inflation Rate |

| Consumer Price Index (CPI) | United States | Friday, Oct 24 | Focus: The week’s highlight; signal for Fed policy. Impact: A soft reading could bolster bonds and risk assets while weakening the USD; a strong figure may revive hawkish fears, unsettling markets. | United States Inflation Rate |

- CONSTITUTIONAL ASYMMETRY, ECONOMIC DEPENDENCY,AND THE CASE FOR NATIONAL SELF-DETERMINATION

Wales, Scotland, and Northern Ireland in Historical,Sociological and Economic Perspective This paper examines the structural, historical, and economic contradictions inherent in the United Kingdom’s constitutional settlement as it pertains to Wales, Scotland, and Northern Ireland. Drawing on political theory, economic data, historical sociology, and comparative constitutional studies, it argues that the current devolution framework, while… Read more: CONSTITUTIONAL ASYMMETRY, ECONOMIC DEPENDENCY,AND THE CASE FOR NATIONAL SELF-DETERMINATION

Wales, Scotland, and Northern Ireland in Historical,Sociological and Economic Perspective This paper examines the structural, historical, and economic contradictions inherent in the United Kingdom’s constitutional settlement as it pertains to Wales, Scotland, and Northern Ireland. Drawing on political theory, economic data, historical sociology, and comparative constitutional studies, it argues that the current devolution framework, while… Read more: CONSTITUTIONAL ASYMMETRY, ECONOMIC DEPENDENCY,AND THE CASE FOR NATIONAL SELF-DETERMINATION - The Necessity of a United Nations HQ Relocation to the Hague with a Permanent Nuremberg Tribunal.The Impunity Crisis of Rogue Governments

The world witnesses today an unprecedented crisis of accountability in international law. As the genocide in Gaza unfolds before global eyes, as war crimes multiply across Ukraine, Myanmar, and countless other conflicts, the United Nations stands paralysed, not by lack of legal framework, but by institutional capture that protects the very criminals it should prosecute.… Read more: The Necessity of a United Nations HQ Relocation to the Hague with a Permanent Nuremberg Tribunal.The Impunity Crisis of Rogue Governments

The world witnesses today an unprecedented crisis of accountability in international law. As the genocide in Gaza unfolds before global eyes, as war crimes multiply across Ukraine, Myanmar, and countless other conflicts, the United Nations stands paralysed, not by lack of legal framework, but by institutional capture that protects the very criminals it should prosecute.… Read more: The Necessity of a United Nations HQ Relocation to the Hague with a Permanent Nuremberg Tribunal.The Impunity Crisis of Rogue Governments - The Digital Job Posting Bubble: Quantifying Phantom Demand in Online Labor Markets

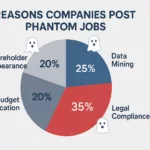

Are businesses and corporates truly hiring ? Has the digital economy become a massive convenience mystification of actual economic activities? How large, systemic and unstable is the assets bubble built by Wall Street financial engineering and gambling addiction? What are the empirical evidence of structural distortions in digital labor markets that represent a significant and… Read more: The Digital Job Posting Bubble: Quantifying Phantom Demand in Online Labor Markets

Are businesses and corporates truly hiring ? Has the digital economy become a massive convenience mystification of actual economic activities? How large, systemic and unstable is the assets bubble built by Wall Street financial engineering and gambling addiction? What are the empirical evidence of structural distortions in digital labor markets that represent a significant and… Read more: The Digital Job Posting Bubble: Quantifying Phantom Demand in Online Labor Markets - United States Criminality and Impunity: Historical-Sociological Perspective of United States Unaccountability and Impunity at the behest of International Law

The United States emerged from World War II as a principal architect of the modern international legal order, including the Nuremberg principles, the Geneva Conventions, and the Universal Declaration of Human Rights. Supreme Court Justice Robert Jackson, who served as chief prosecutor at Nuremberg, articulated a principle that would become foundational to international criminal law… Read more: United States Criminality and Impunity: Historical-Sociological Perspective of United States Unaccountability and Impunity at the behest of International Law

The United States emerged from World War II as a principal architect of the modern international legal order, including the Nuremberg principles, the Geneva Conventions, and the Universal Declaration of Human Rights. Supreme Court Justice Robert Jackson, who served as chief prosecutor at Nuremberg, articulated a principle that would become foundational to international criminal law… Read more: United States Criminality and Impunity: Historical-Sociological Perspective of United States Unaccountability and Impunity at the behest of International Law - What Everyone Gets Wrong About Inflation: 5 Surprising Economic DataThe public is rightly concerned about the rising cost of living, and the dominant economic narrative offers what seem like simple truths: falling prices are a bad omen, and we must accept higher unemployment as the bitter medicine needed to cure inflation. But this conventional wisdom isn’t just wrong—it’s dangerously flawed, leading to policies that… Read more: What Everyone Gets Wrong About Inflation: 5 Surprising Economic Data