The global equity markets opened mixed amid geopolitical tensions and economic uncertainty. The U.S. indices saw a modest pullback, led by technology and AI sector cooling, while European markets remained steady with selective sector strength in luxury and energy. Asian markets experienced mixed performance with cautious trading ahead of major policy announcements. Safe-haven assets surged as gold prices broke above $4,000 per ounce for the first time, reflecting investor anxiety. The Japanese yen weakened sharply, and the U.S. dollar strengthened on continued fiscal risks from the prolonged U.S. government shutdown. Commodity prices saw divergent moves, with platinum and silver also advancing, while crude oil prices showed resilience amid supply concerns. Market participants await upcoming U.S. earnings and Fed speakers for further direction. European equities are displaying a dynamic landscape marked by both high-momentum movers and compelling value plays, as well as clear evidence of volatility around 52-week extremes. Portfolio allocation remains a key theme in managing these opportunities and risks.

Biggest European Stock Movers

The EURO STOXX 50 showcases several notable performers this week. Top gainers include technology and financial leaders such as Adyen B.V., which advanced 2.14%, and ASML, a semiconductor heavyweight, up nearly 2% on the day with double-digit growth over the past year. SAP and Allianz also post strong, steady annualised gains, highlighting ongoing sector resilience. On the losing side, luxury giant LVMH faces a pullback, while cyclical industrials like Saint-Gobain and VINCI endure late-period volatility. The breadth across sectors—from health to energy and telecom—underscores diverse regional economic drivers.

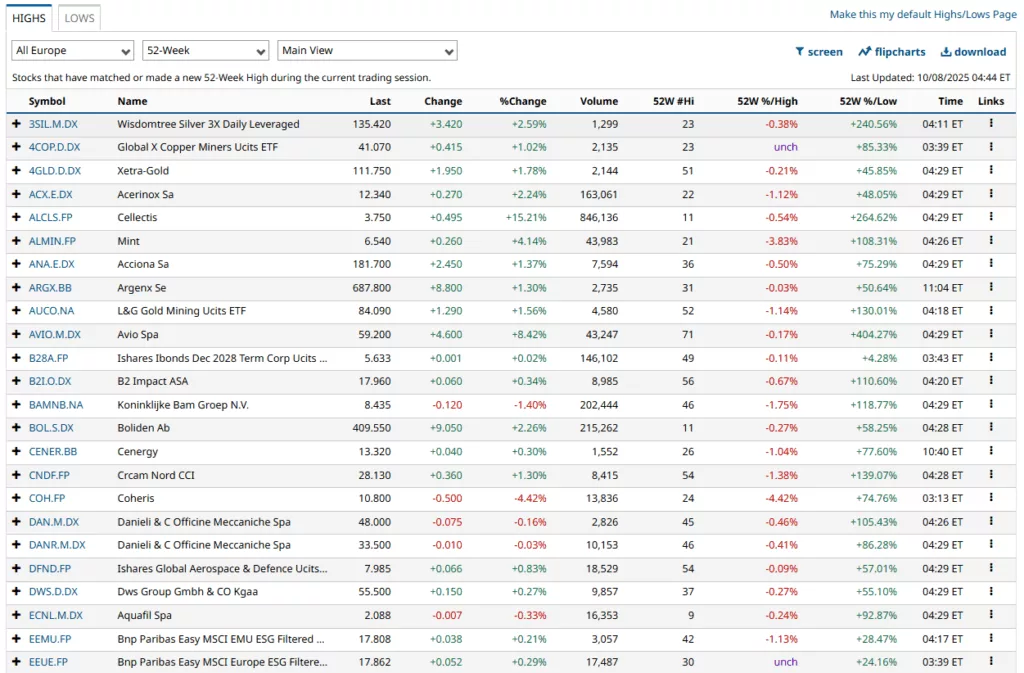

52-Week Highs and Lows

Europe continues to see a number of stocks testing, matching, or breaking their annual price records. For investors, stocks near their 52-week lows, such as select names in manufacturing, energy, or basic materials, may represent value entry points due to cyclical or idiosyncratic pressures. Conversely, technology, insurance, and some financial stocks are recording new highs based on robust earnings and sector rotation trends. Monitoring these levels offers insight into positioning for recovery candidates as well as momentum trades.

Trends and Portfolio Allocation Strategies

- Growth sectors (technology, financials, and industrials linked to sustainability) outperform, but volatility remains due to macroeconomic shifts.

- Defensive allocation to health care, consumer staples, and utilities is seen where recession fears persist.

- Cross-sector diversification remains vital, with some rotation toward value stocks at 52-week lows as part of a contrarian or value strategy.

- Regional allocation increasingly prioritises countries with strong fiscal stimulus and infrastructure investment, such as Germany and the Netherlands.

- Balanced portfolios favour a mix between high-momentum growth stocks and deep-value plays with strong fundamentals.

Allocating substantially to large-cap leaders, layering in resilient dividend growers, and selectively adding small/mid-cap recovery plays create defensive and opportunistic balance. Short-term traders may favour momentum names, while long-term investors blend stable blue chips with emerging market disruptors. Risk management is critical given global headwinds such as inflation, interest rate uncertainty, and political instability.

Key Risks Moving Forward

Investors should watch for: Rapid swings at 52-week highs and lows, indicating crowding and potential reversals, and Sudden shifts in central bank policy impacting rates. Geopolitical developments and supply chain strains are affecting cyclicals. Earnings surprises, particularly expected in sectors that benefited from artificial growth during previous stimulus cycles.