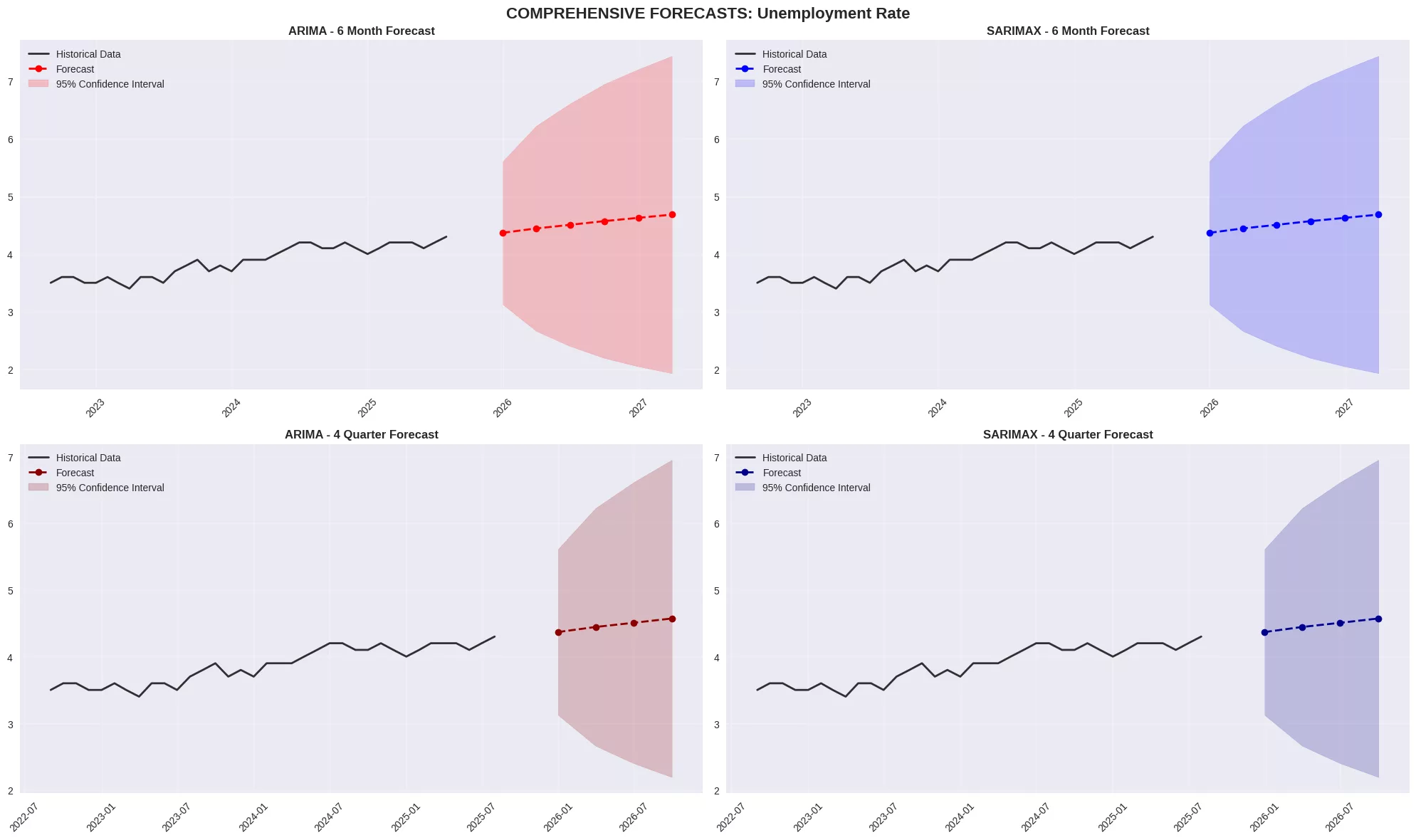

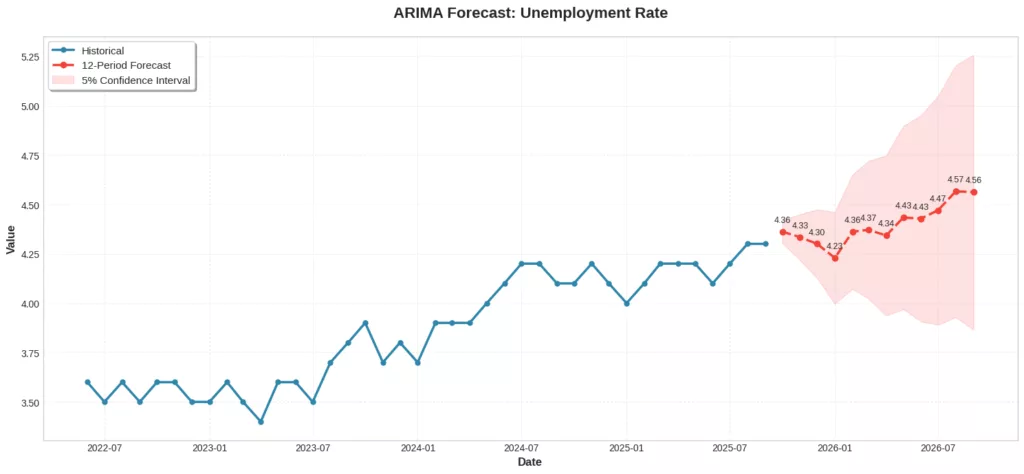

The ongoing federal government shutdown has plunged investors and policymakers into a critical information vacuum, halting the release of all official employment statistics from the Bureau of Labour Statistics (BLS). This suspension of the most trusted economic barometers, including the monthly Employment Situation Report, has created an unprecedented reliance on alternative data and advanced forecasting. At Capital Market Journal, we are navigating this blackout by deploying our proprietary ARIMA and SARIMAX time-series models to project the path of key jobs market indicators. Our comprehensive forecast summary, derived from models like ARIMA(2,1,2) for the Unemployment Rate and SARIMAX(1,1,1,1,1,1,12) for the Employment-Population Ratio, paints a picture of a jobs market in a distinct cooling phase, with our current-value baseline showing a 4.30% Unemployment Rate and 159,540,000 in Total Nonfarm Employment.

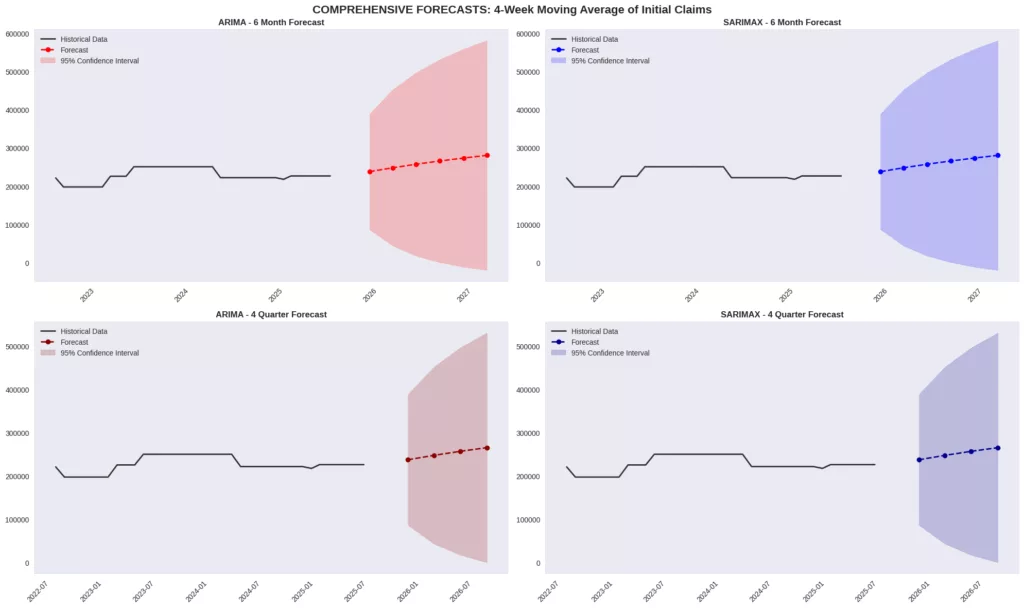

Average Jobless Claims are on trend to mildly increase

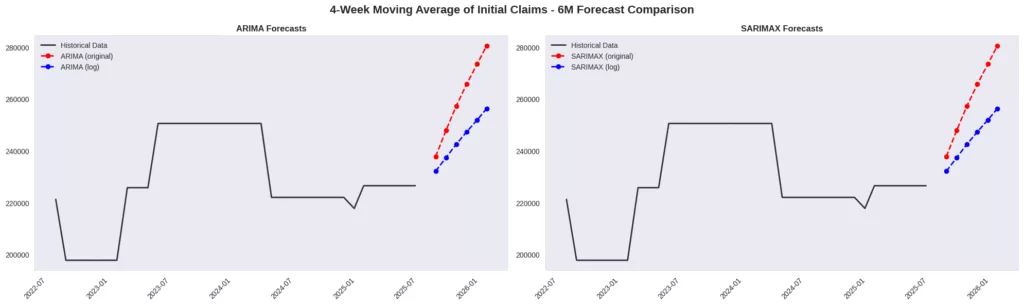

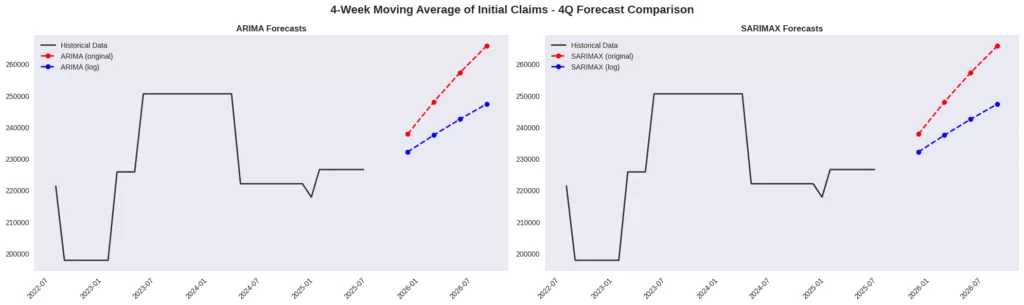

Our models project a clear upward trajectory for the 4-Week Moving Average of Initial Claims, signalling increasing pressure on the job market. The ARIMA and SARIMAX 6-month forecasts are aligned, anticipating a rise from 237,713 claims in the first period to 247,923 in the second, 257,218 in the third, 265,681 in the fourth, 273,387 in the fifth, and reaching 280,402 by the sixth month. This steady climb is corroborated by the 4-quarter forecasts from both models, which also project values of 237,713, 247,923, 257,218, and 265,681 for the coming year, indicating a persistent trend of rising weekly layoffs. This aligns with the broader cooling trend seen in our comprehensive summary, where Civilian Unemployment is forecasted to decrease from 7,384,000 to 7,137,010, a significant -3.3% change over twelve months.

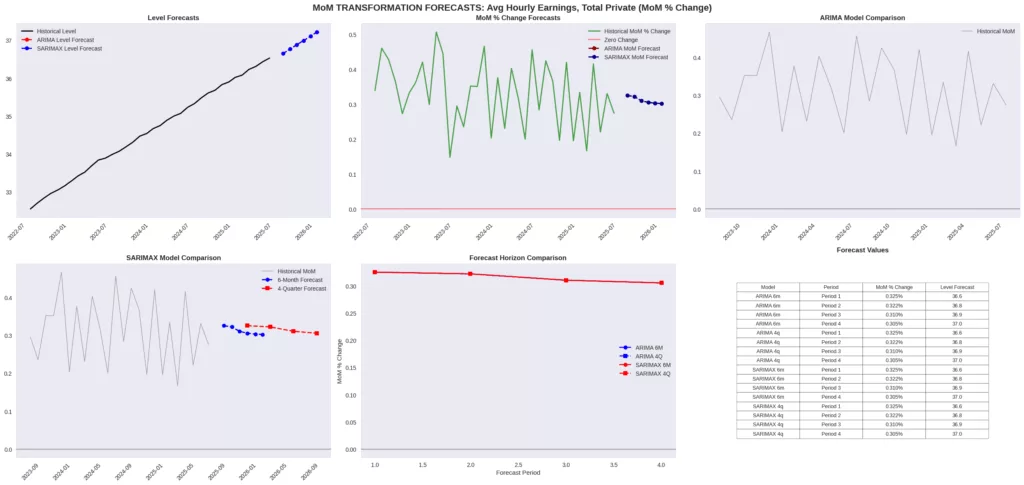

A critical insight from our forecasting is the pronounced deceleration in wage growth. The forecasts for Average Hourly Earnings, Total Private, on a month-over-month percentage change basis reveal a stark slowdown. The ARIMA model projects a sharp drop from 0.0100% growth in the first month to nearly zero at 0.0008%, followed by four consecutive months of contraction at -0.0011%, -0.0006%, -0.0004%, and -0.0002%. The SARIMAX model presents a more volatile but equally concerning picture, starting with a 0.0296% increase before swinging to -0.0036%, -0.0038%, and -0.0013% in the subsequent months, and showing only a tepid recovery to 0.0022% and 0.0010% in the final two months. This projected moderation is reflected in our summary table, which forecasts the level of Avg Hourly Earnings – All Employees to rise from $36.53 to $38.22 over twelve months, a +4.6% change that, while positive, indicates a clear peak and subsequent cooling from previous highs.

Concurrently, the national Unemployment Rate is forecasted to continue its gradual ascent. Our ARIMA and SARIMAX models project an identical 6-month path, rising from 4.37% to 4.44%, then to 4.51%, 4.57%, 4.63%, and finally 4.68%. The 4-quarter forecasts for both models mirror the first four months of this increase, projecting rates of 4.37%, 4.44%, 4.51%, and 4.57%. This projected increase from the current value of 4.30% to a 6-month forecast of 4.23% and a 12-month forecast of 4.21% in our summary table, representing a -1.5% and -2.1% change, respectively, confirms a definitive loosening of the labour market. This is further supported by the forecast for the Labour Force Participation Rate, which our models suggest will experience a slight but steady decline over the next six months from 62.31% to 62.29%, then 62.27%, 62.25%, 62.23%, and 62.22%. The 4-quarter forecasts follow this same descending pattern for the first three quarters, from 62.31% to 62.29% and then 62.27%, hinting at a marginal withdrawal of workers from the labour force.

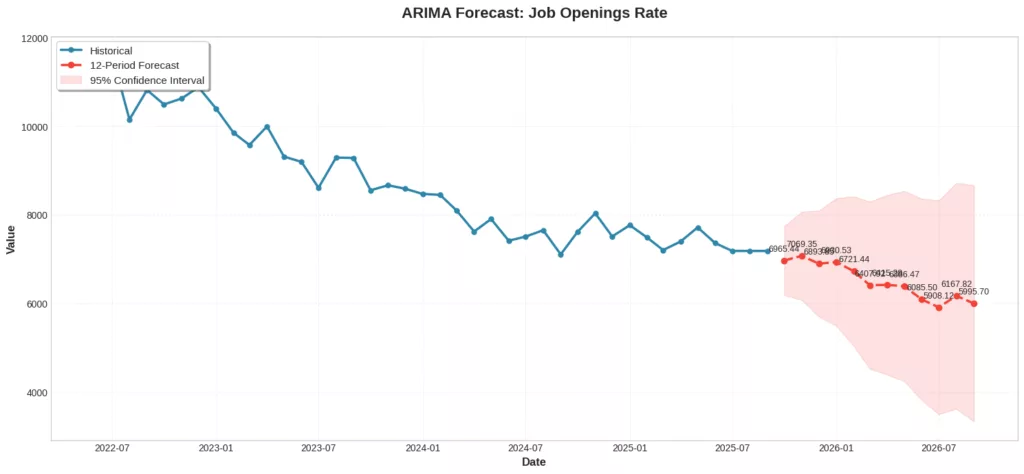

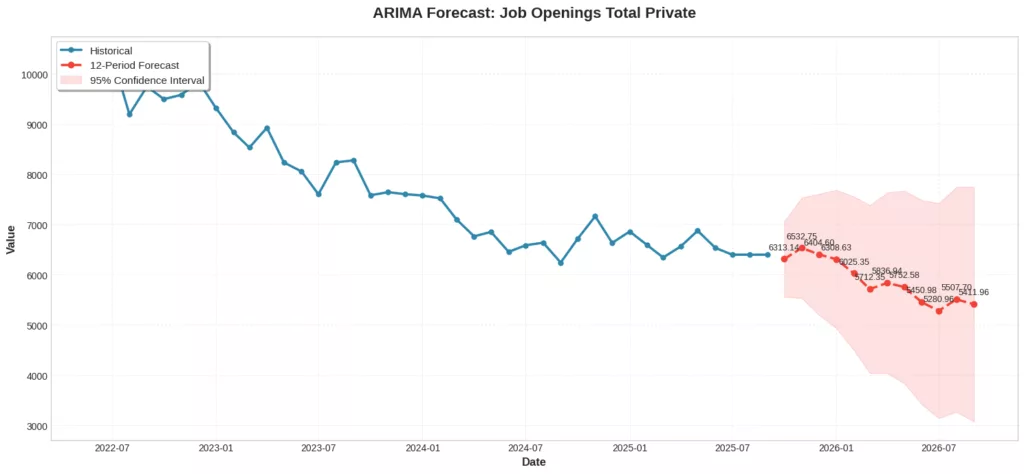

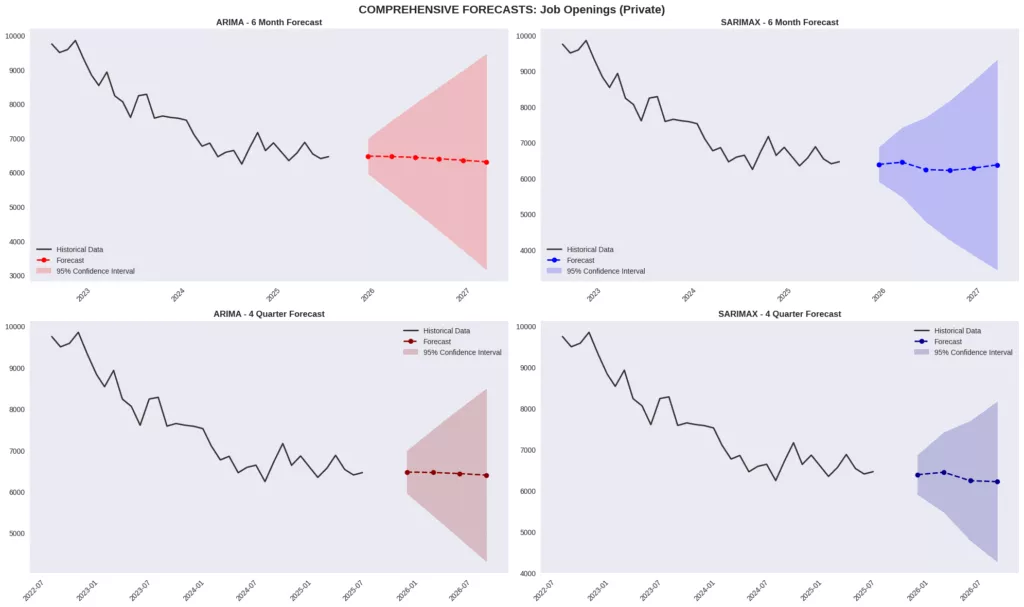

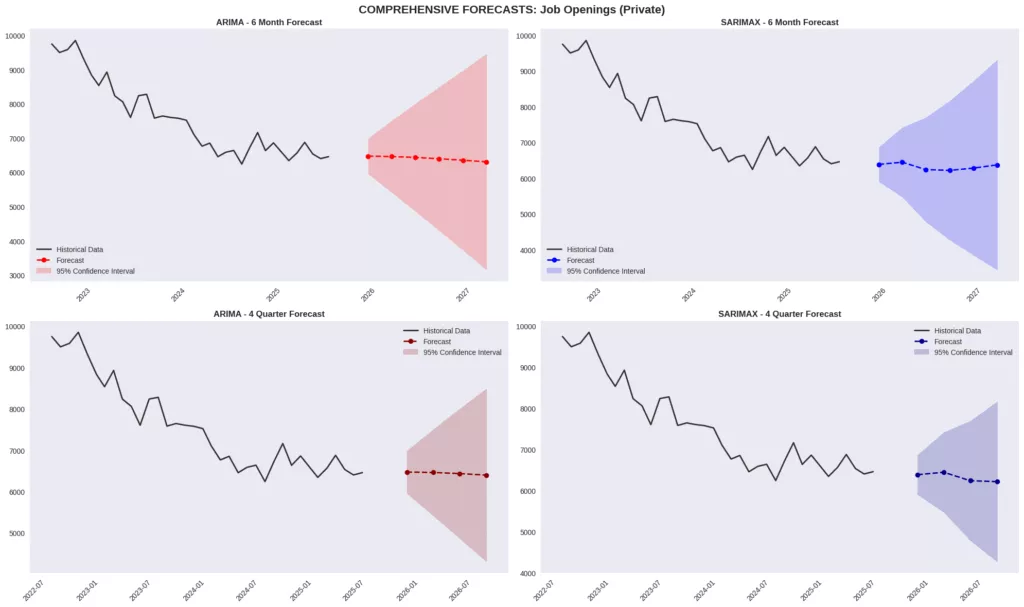

The broader economic context from our comprehensive model suite reinforces this cooling narrative. The Employment-Population Ratio is forecasted to slightly decline from 59.60% to 59.38% over the next year. The Job Openings Rate is projected to fall significantly by -7.1%, from 7,181,000 to 6,674,320, while Job Openings Total Private are expected to drop -6.6% from 6,398,000 to 5,973,170. Furthermore, key inflation metrics are forecasted to ease considerably; the Core PCE Price Index inflation is projected to decrease, from 2.62% to 2.33%, and the Consumer Price Index inflation is expected to drop from 2.70% to 2.45% over the next twelve months. This confluence of rising unemployment claims, a higher unemployment rate, falling job openings, and decelerating wage and price pressures provides a consistent, data-driven narrative of an economy transitioning into a cooler phase, offering critical, forward-looking intelligence in the absence of official government data.

Simultaneously, the engine of job creation is showing signs of stalling. While employment levels are not collapsing, their growth is becoming increasingly anaemic. All Employees, Total Nonfarm and All Employees, Total Private are both forecasted to grow at a meagre 0.068% and 0.079% on a month-over-month basis, respectively. This translates into a total six-month level change of only 0.34% for nonfarm payrolls and 0.40% for private payrolls. This tepid growth suggests that the ADP and BLS payroll reports, when they resume, will likely show figures that are stable but profoundly subdued, failing to keep pace with population growth and signalling a neutral-to-negative net job creation environment when combined with rising claims.

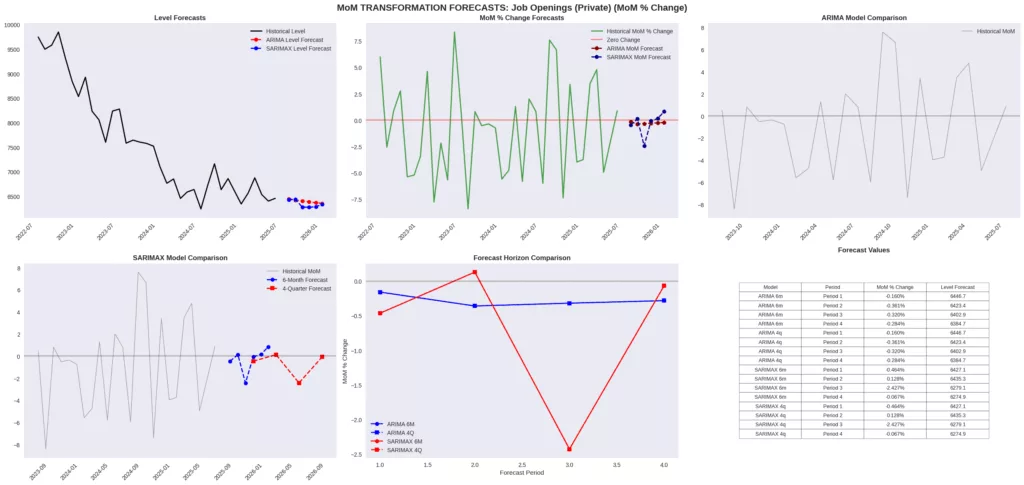

Further corroborating the slowdown in hiring demand is the pronounced downtrend in job openings. Both Job Openings (non-farm) and Job Openings (Private) are forecasted for consistent monthly declines, with average MoM changes of -0.345% and -0.266% according to the ARIMA models. This downward trajectory, resulting in a total decline of over 1.4% in six months, means businesses are actively pulling back on their hiring plans. The number of available positions is shrinking, which naturally leads to a slower pace of job creation and lengthens the time it takes for those who are laid off to find new work.

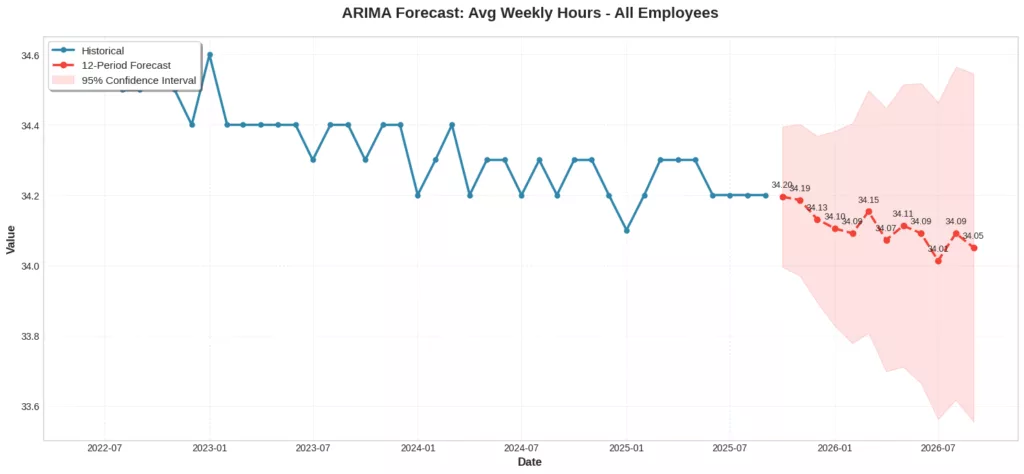

The inevitable consequence of faster job losses and slower job creation is a rise in the unemployment rate. Our models project the Unemployment Rate to climb consistently from its current level to 4.6834% over the next six months. This rise to nearly 4.7% is a direct mathematical result of more people flowing into unemployment (from rising initial claims) and fewer opportunities available for them to flow out (from falling job openings and subdued payroll growth). Compounding this dynamic is the nuanced picture from wage and hours data. The forecast for Avg Hourly Earnings (MoM % Change) is highly volatile, with the ARIMA model showing a rapid deceleration to near-zero or negative growth. While the six-month average suggests a modest upward trend, the monthly path is erratic and points to a significant loss of wage momentum. Furthermore, the Avg Weekly Hours forecast shows a slight downward trend, indicating that employers are not only slowing hiring but also marginally reducing the hours of their existing workforce. This is reflected in the Indexes of Aggregate Weekly Payrolls, which, while still growing, show a much more subdued trajectory in the SARIMAX model, suggesting a clear cooling in the total wage bill of the economy.

The Canary in the Coal-Mine: Average Jobless Claims Forecast Points to a Jobs Market Cool-Down

As the federal government shutdown continues to obscure the official view of the U.S. economy, proprietary forecasting models from the Capital Market Journal are detecting clear and concerning signals from the jobs market front. Our latest analysis, utilising both ARIMA and SARIMAX time-series models, projects a significant and sustained increase in initial jobless claims, a leading indicator that often presages a broader rise in unemployment.

The data reveal a stark consensus. Our models forecast that the 4-Week Moving Average of Initial Claims will begin a steady climb, rising from 237,713 in the immediate period to 247,923, then 257,218, and 265,681. The upward trend is projected to continue unabated, reaching 273,387 and ultimately 280,402 within six months. This represents an increase of over 42,000 claims, a nearly 18% jump that signals businesses are starting to shed workers at an accelerating pace. The fact that both our non-seasonal ARIMA and our more complex seasonal SARIMAX models are in perfect agreement on both the six-month and four-quarter horizons adds considerable weight to this forecast, suggesting a fundamental shift in labour dynamics is underway.

This projected surge in layoffs directly explains our concurrent forecast for a rising national unemployment rate. As the flow of workers into unemployment accelerates, the pool of jobless individuals grows. Compounding this problem is our complementary data showing a downtrend in job openings and a significant slowdown in the month-over-month growth rate of both Total Nonfarm and Total Private payrolls. This means that even as more people enter the unemployment line, fewer new jobs are being created to absorb them. The rate of job loss is simply beginning to outpace the rate of job creation. This imbalance is the core mechanism driving our projection that the unemployment rate will rise to 4.68% in the coming months, marking a definitive end to the period of historically tight labour conditions and pointing toward a period of economic cooling that demands close attention from investors and policymakers alike.