Current Economic Framework of the UK

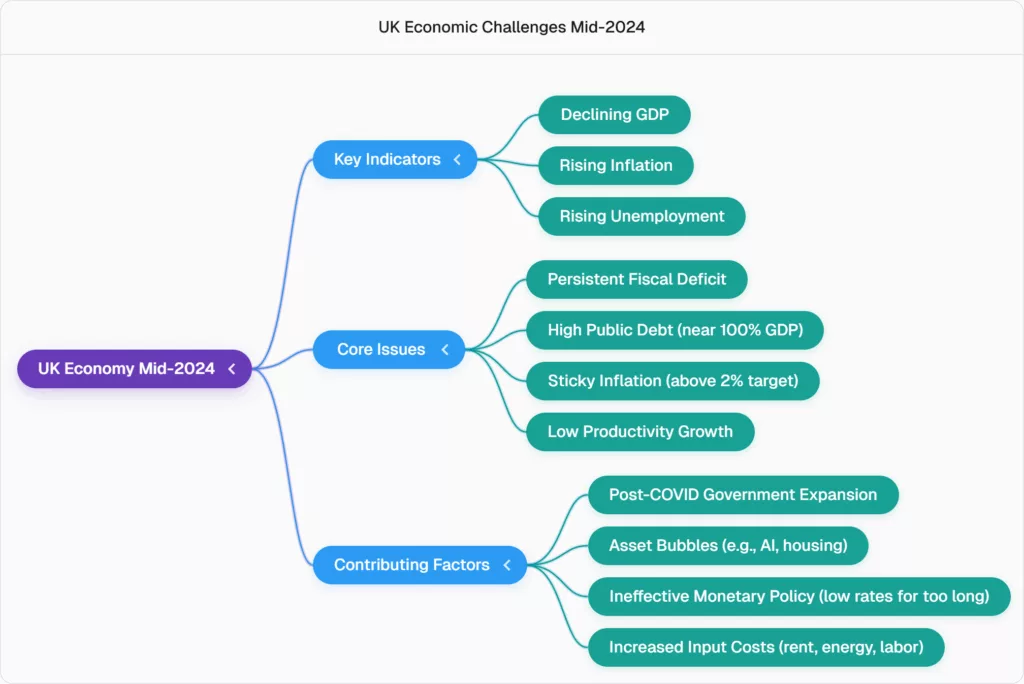

- The UK economy is currently experiencing a slowdown, characterised by declining GDP and rising inflation, which raises questions about the need for fiscal and economic policy adjustments.

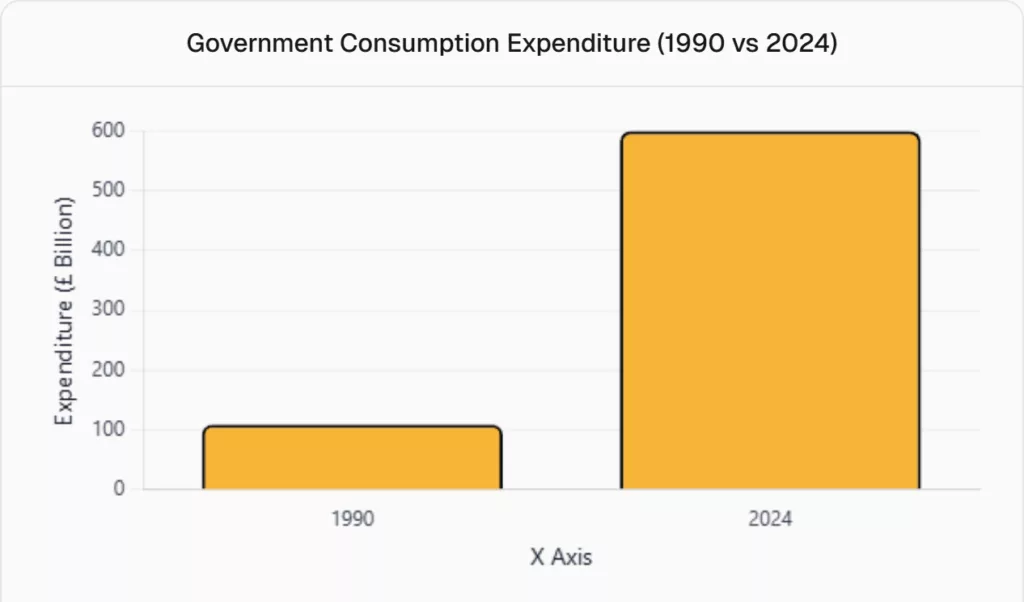

- Government final consumption expenditure has grown exponentially, reaching £599 billion in 2024, a significant increase from £109 billion in 1990, driven by an expanding government workforce and increased demand for public services.

Government Finances and Debt

- The aggregate of National Insurance Contribution (NIC) receivables remained stagnant at around £230.7 billion for both 2023 and 2024. A shortfall of £66 million from 2023 to 2024 likely necessitated an increase in the employer NIC rate from 13.8% to 15% to boost cash flow.

- The UK has experienced a persistent fiscal deficit since 1990, with surpluses only recorded in 1999, 2000, and 2001. These surpluses coincided with technological improvements that enhanced GDP growth and increased tax revenues.

- Since the 2010 Great Financial Crisis, the government has accumulated over £1.75 trillion in deficits, largely due to a prolonged period of zero lower bound interest rates and quantitative easing. This accumulation makes managing public finances challenging as the debt-to-GDP ratio approaches the psychological threshold of 100%.

- The cost of servicing the UK’s public debt has dramatically increased from approximately £30 billion to over £80 billion, primarily due to higher inflation and rising long-duration interest rates.

Inflationary Pressures and Forecasts

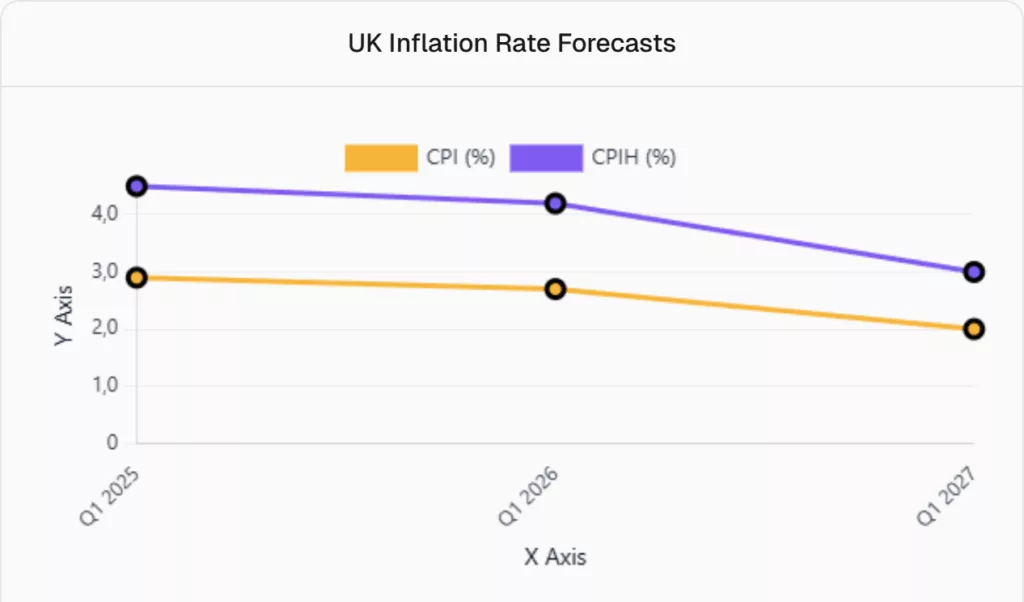

- Various forecasts consistently indicate that UK inflation will remain persistent and “sticky,” often above the target 2%.

- The Consumer Price Index (CPI) is projected to decline to around 2.9-2.6% in the near term, with a potential convergence to 2% by approximately 2027.

- The CPIH (which includes housing costs) is expected to remain higher, around 4-4.6% in 2025-2026.

- The Retail Price Index (RPI) is consistently forecast above 3%, with the 12-month RPI around 4.9-4.4%. Rent prices, a significant component, are projected to remain very high, potentially above 8%.

Here is a line chart showing inflation rate forecasts for CPI and CPIH:

- Inflation data shows characteristics of a fat-tail distribution (kurtosis > 3) and autocorrelation for several lags, implying high volatility and correlation with past data.

Labour Market Trends, Productivity and Output Gap

- Forecasts indicate a rising trend in unemployment, expected to reach around 4.6-4.7%, suggesting a weakening aggregate supply in the economy.

- Employment levels are stable around 75%, which is below the pre-2020 peak of 76.4%.

- The simultaneous occurrence of rising unemployment and high inflation creates a challenging economic situation akin to stagflation

- Labour productivity has been slightly negative, indicating sluggishness in the economy’s efficiency.

- The overall output gap is estimated to be flat or slightly negative, meaning the economy is operating below its full potential and faces a risk of stagnation.

- Persistent high inflation negatively impacts the output gap, leading to real GDP growing at a slower rate than its potential.

Monetary and Fiscal Policy Challenges

- The Bank of England faces a significant dilemma: high inflation pressures suggest maintaining or raising interest rates, while a negative output gap and rising unemployment call for rate cuts to stimulate economic activity.

- Globally, monetary policy has been excessively accommodative for too long, contributing to the current inflationary shock and the formation of an asset bubble.

- The Taylor Rule suggests that during periods of high inflation (e.g., 12% inflation), interest rates should have been hiked significantly more (potentially over 10%) to properly price the money supply and constrain excessive government borrowing.

- The UK economy is described as an “overheating engine” due to high input costs and sticky inflation, running at high “RPMs” (high costs) without a corresponding increase in “speed” (economic growth). Businesses respond by reducing “horsepower” and workforce to manage costs.

- To address these challenges, fiscal policy must support monetary policy through structural reforms, such as implementing a more progressive income tax structure with additional income brackets and adjusting tax rates in line with wage growth to free up capital and enhance the economy.

Policy Simulations and Recommendations

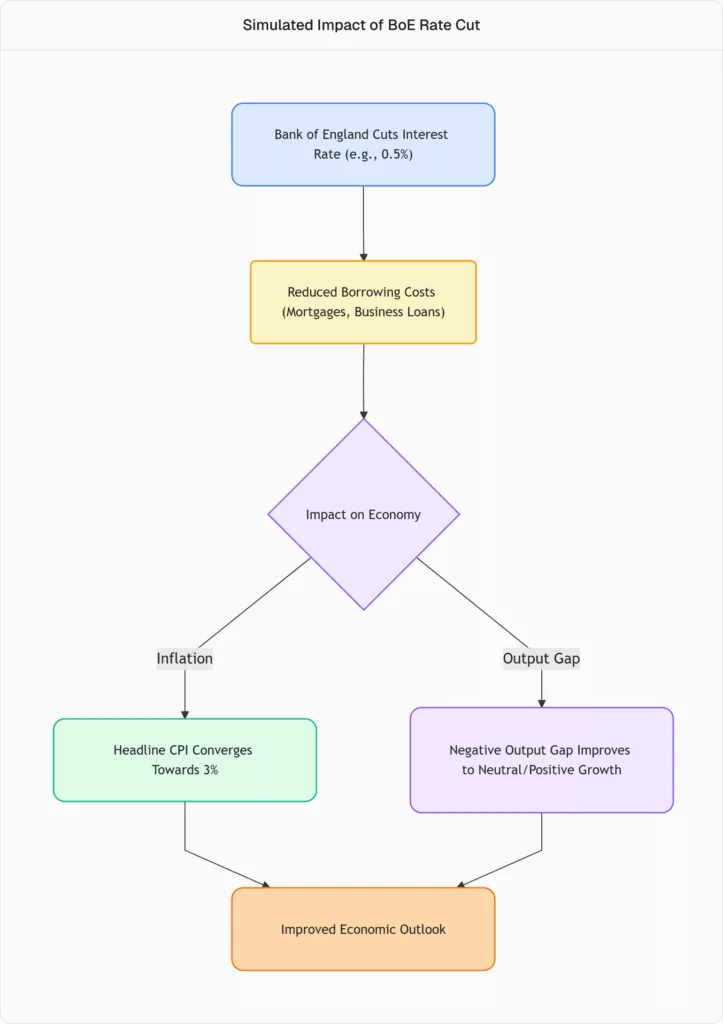

- Simulations suggest that if the Bank of England were to reduce interest rates by 0.5 percentage points (two 0.25% cuts), inflation could paradoxically decrease and converge towards 2-2.5% over 20 periods, while the negative output gap could become neutral or positive.

- Such rate cuts would reduce borrowing costs for mortgages and businesses, potentially contributing to lower inflation and stimulating economic growth.

- Despite inherent risks, there is an argument to encourage the Bank of England to implement modest rate reductions (e.g., 0.25% or 0.5%) given the slowing economy and rising unemployment.

- UNITED STATES GOVERNMENT VIOLATIONS OF HABEAS CORPUS ARE A VIOLATION OF ARTICLE 3 OF THE NATO TREATY AND A THREAT TO INTERNATIONAL LAW

THE UNITED STATES OF AMERICA WILL BE OFFICIALLY DEFINED: ROGUE STATE IN THE FORM OF ETHNO-NATIONALIST, NAZIST, WHITE SUPREMATIST, GENOCIDAL TOTALITARIAN DICTATORSHIP. The UNITED… Read more: UNITED STATES GOVERNMENT VIOLATIONS OF HABEAS CORPUS ARE A VIOLATION OF ARTICLE 3 OF THE NATO TREATY AND A THREAT TO INTERNATIONAL LAW

THE UNITED STATES OF AMERICA WILL BE OFFICIALLY DEFINED: ROGUE STATE IN THE FORM OF ETHNO-NATIONALIST, NAZIST, WHITE SUPREMATIST, GENOCIDAL TOTALITARIAN DICTATORSHIP. The UNITED… Read more: UNITED STATES GOVERNMENT VIOLATIONS OF HABEAS CORPUS ARE A VIOLATION OF ARTICLE 3 OF THE NATO TREATY AND A THREAT TO INTERNATIONAL LAW - The Necessity of a United Nations HQ Relocation to the Hague with a Permanent Nuremberg Tribunal.The Impunity Crisis of Rogue Governments

The world witnesses today an unprecedented crisis of accountability in international law. As the genocide in Gaza unfolds before global eyes, as war crimes… Read more: The Necessity of a United Nations HQ Relocation to the Hague with a Permanent Nuremberg Tribunal.The Impunity Crisis of Rogue Governments

The world witnesses today an unprecedented crisis of accountability in international law. As the genocide in Gaza unfolds before global eyes, as war crimes… Read more: The Necessity of a United Nations HQ Relocation to the Hague with a Permanent Nuremberg Tribunal.The Impunity Crisis of Rogue Governments - THE UNITED STATES VICE-PRESIDENT IS EXPRESSION OF THE DERANGED INNER CIRCLE OF AMERICAN-NAZIST RUNNING THE WHITE-NUTHOUSEBy the time the cameras cut away, the Vice-President had spoken for exactly 2,040 seconds.That was all it took to show the country what… Read more: THE UNITED STATES VICE-PRESIDENT IS EXPRESSION OF THE DERANGED INNER CIRCLE OF AMERICAN-NAZIST RUNNING THE WHITE-NUTHOUSE

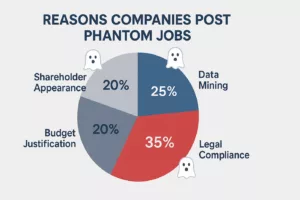

- The Digital Job Posting Bubble: Quantifying Phantom Demand in Online Labor Markets

Are businesses and corporates truly hiring ? Has the digital economy become a massive convenience mystification of actual economic activities? How large, systemic and… Read more: The Digital Job Posting Bubble: Quantifying Phantom Demand in Online Labor Markets

Are businesses and corporates truly hiring ? Has the digital economy become a massive convenience mystification of actual economic activities? How large, systemic and… Read more: The Digital Job Posting Bubble: Quantifying Phantom Demand in Online Labor Markets - The U.S. NSS 2025 is a Grandiose Magalomaniac view of the WorldThe 2025 U.S. National Security Strategy is the first state paper to be issued from inside a full-blown collective state apparatus psychosis. It does… Read more: The U.S. NSS 2025 is a Grandiose Magalomaniac view of the World