The wider global car industry slow-down and manufacturing recession will inevitably impact also Tesla’s revenues in the main business of car sales and leasing, considering its very high stock price valuation and stock financial ratios, these need to be a warning signal for all investors that hold Tesla shares. Based on Tesla’s financial statement at the end of Q3 2024, Automotive Sales year-to-date 2024 amounted to $53,28 billion already decreased -7.0% from $ 57,87 billion in 2023, while also confirming the decreasing trend in car sales. Tesla’s automotive leasing revenue in Q3 2024 was $446 million less than $490mln in Q3 2023 and overall YTD leasing revenue have been $1.38 billion decreasing -15% from $1.62 billion in 2023. Overall Tesla revenues from Sales and Services have been YTD $70,19 Billion slightly up from $69,57 billion in 2023, while the 2024 yearly figures have been fiddled by Tesla with the deferring of (FSD) Full Self Driving revenue figure of $3.54 billion as of Q3 2024, indicating an arbitrary increase in future revenue recognition from customers who have purchased FSD and related services, but whose revenue will be recognized over time. The car leasing line of business of Tesla has encountered a few bumps in the road, in fact, Tesla car leases have decreased -24% to $529mln in 2024 less than $692mln in 2023 for the same period.

Financial Ratios highlight extreme valuation

According to the last stock market price of Tesla $330.24 per share and the most usual ratio observed to measure if a stock price is overvalued, a P/E Ratio of 70.63 stands at multiples above an already high wider industry P/E Ratio of 24.15, in fact, Tesla shares are grossly overvalued in light of the fact that car sales growth has been slowing already and the prospect of the car industry seems on a slow but steady recessionary and stagnation, hence future Tesla revenues growth figures from car sales and leases have been overestimated and the multiples that investors pay for Tesla shares are grossly overvalued and mispriced, indeed, the P/E Ratio 70.63 also defines the economical fact that with $4.67 EPS it will take 70.63 YEARS for any investor to be repaid of the $330 of equity invested on a single Tesla share, let’s that sink.

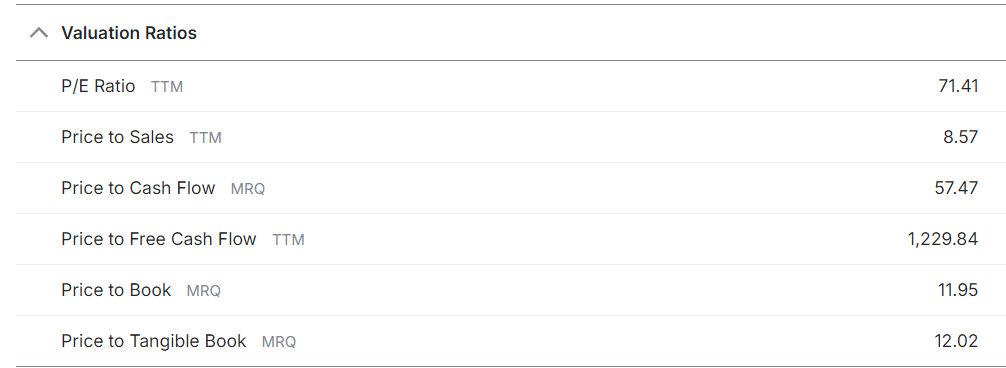

Indeed other financial ratios are quite alarming and should sound the alarm bell to investors, in fact, the Forward P/E Ratio of 60.02 has been estimated at a very high level compared to the industry average, and eventually mispriced expecting substantial growth in Tesla revenue while the global car industry is slowly declining into stagnation and reduction of personnel and lay off globally, due to overproduction compared to stagnating and declining car sales in all segments across all geographies and markets. Tesla’s PEG ratio of 4.10 compares unfavourably to the industry average of 3.52, implying that even when accounting for growth, Tesla’s valuation may be stretched. The PEG ratio is a metric often used to assess whether a stock is overvalued based on its growth rate, and a higher PEG ratio can suggest that the growth priced into the stock may not be fully justified by actual growth rates. At 10.90, Tesla’s P/S ratio also far exceeds that of Ford (0.27) and GM (0.40), and the automotive industry average is 2.76. This high P/S ratio could indicate an overvaluation if Tesla’s sales growth does not continue at a fast pace. Price to Book Value (P/BV) Ratio: Tesla’s P/BV ratio of 16.84 is considerably higher than Ford’s 1.03, GM’s 0.98, and the industry benchmark of 6.85. This metric implies a high premium on Tesla’s book value, indicating potential overvaluation relative to its asset base. Price to Cash Flow (MRQ): 57.47. This high ratio indicates investors are paying a substantial premium for Tesla’s operating cash flow, which could indicate a speculative investment unless growth justifies this figure. The most alarming financial ratio of Tesla shares is the Price to Free Cash Flow of 1,229.84. An extremely high ratio like this highlights potential overvaluation, with the price far outpacing Tesla’s free cash flow.

Tesla overvalued share price and the risk of decreasing Free Cash Flow and Operating Margins

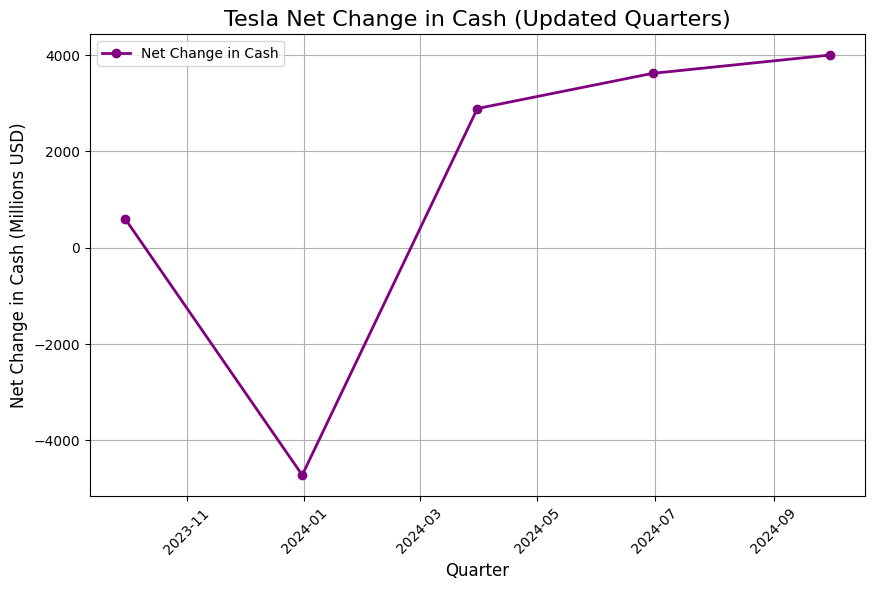

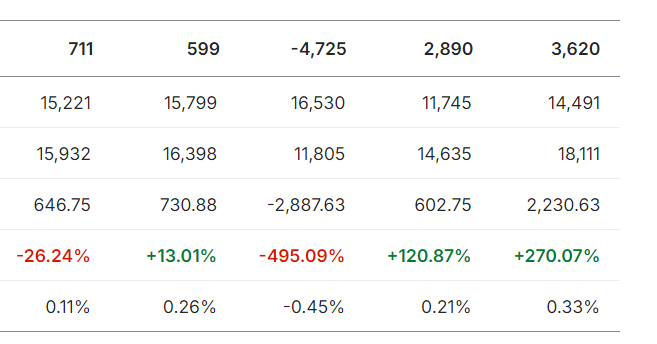

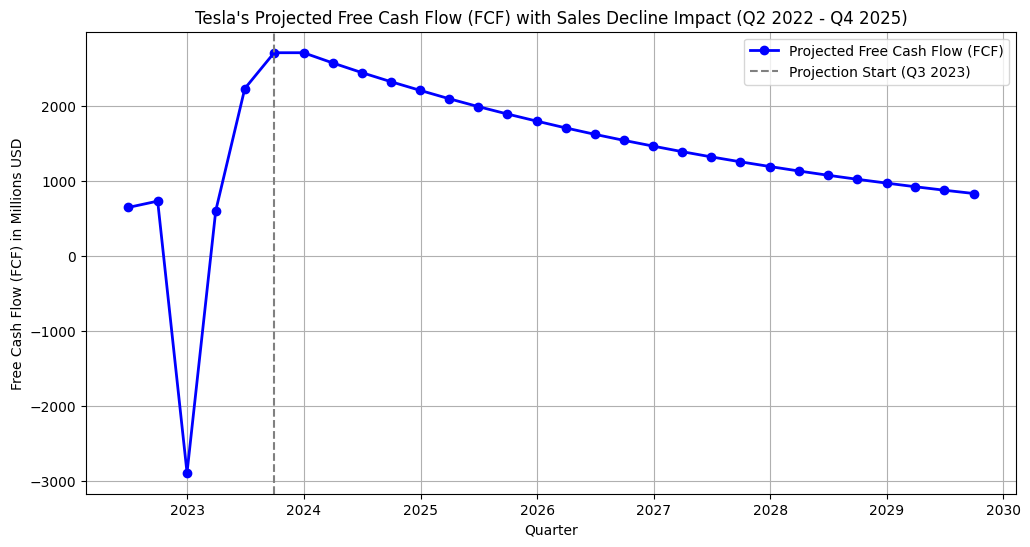

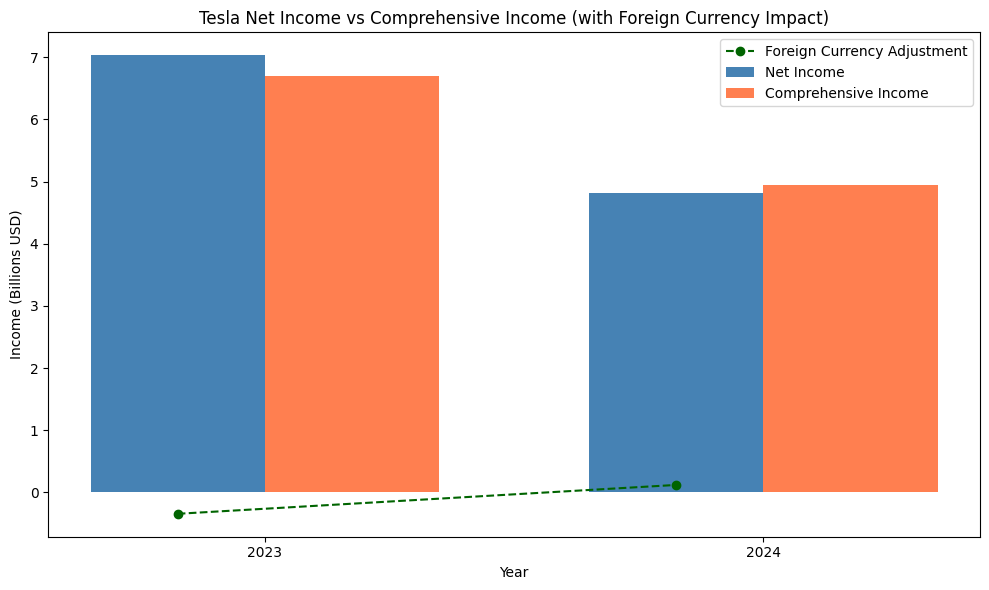

Recent quarters of Tesla’s free cash flow statement reflect substantial variability in revenues and operating margins and significant fluctuations from cash operations. Over the last five quarters, Net Change in Cash shows fluctuations, including a significant negative cash change of -$4,725 million in Q3 2023, followed by positive changes in subsequent quarters. While the company ended 2023 with strong cash balances (~$16 billion), the Levered Free Cash Flow figures are concerning. For Q1 2024, a large negative cash flow of -$2.89 billion was reported, followed by a strong recovery of $2.23 billion in Q2 2024. Free Cash Flow Yield remains low (~0.11% to 0.33%), which indicates that Tesla’s stock is not currently generating substantial cash relative to its market value, signalling potential overvaluation. Additionally, the leveraged free Cash Flow Growth fluctuated wildly, with a severe dip of -495% in Q1 2024, which is a major red flag indicating significant strain on cash generation capacity. For investors, the negative cash flow growth and volatility in cash generation may signal liquidity risks or a decline in operational efficiency, particularly in light of global economic challenges and slowing car sales. Tesla’s ability to maintain profitability and free cash flow growth is critical. If these trends continue, there may be heightened risks of overvaluation for the stock, especially if future earnings fail to justify the current market price. Investors should be cautious of potential price corrections if Tesla struggles to consistently generate positive cash flows, especially amid declining global automotive demand.

Impact of Declining Free Cash Flow (FCF)

Wall Street consensus and the stock market have been pricing exuberant growth of Tesla profits, meanwhile, the whole global car industry has been stagnating and global car sales flatlining and declining with the EVs segment seeing a very difficult future of growth in car sales. In this framework, considering Tesla’s Free Cash Flow of the past quarters results have been of a probability of FCF declines in the coming quarters, due to global car sales and leases slowing down and Tesla will likely experience reduced revenue growth due to weakening demand in the automotive market, particularly as global car sales are expected to contract. Lower sales volume, combined with possible pricing pressure due to increasing competition or inflationary costs, would lead to a decline in revenue growth, as also operating margins would see a squeezing. The decline in FCF driven by reduced global car sales will likely lead to a revenue slowdown and operating margin contraction for Tesla. This, in turn, could expose the overvaluation of Tesla’s stock, as investors will adjust their expectations and reprice the stock based on weaker fundamentals. Investors relying on continued strong earnings growth may face a reality check, which could result in a significant downward revaluation of Tesla’s stock price.

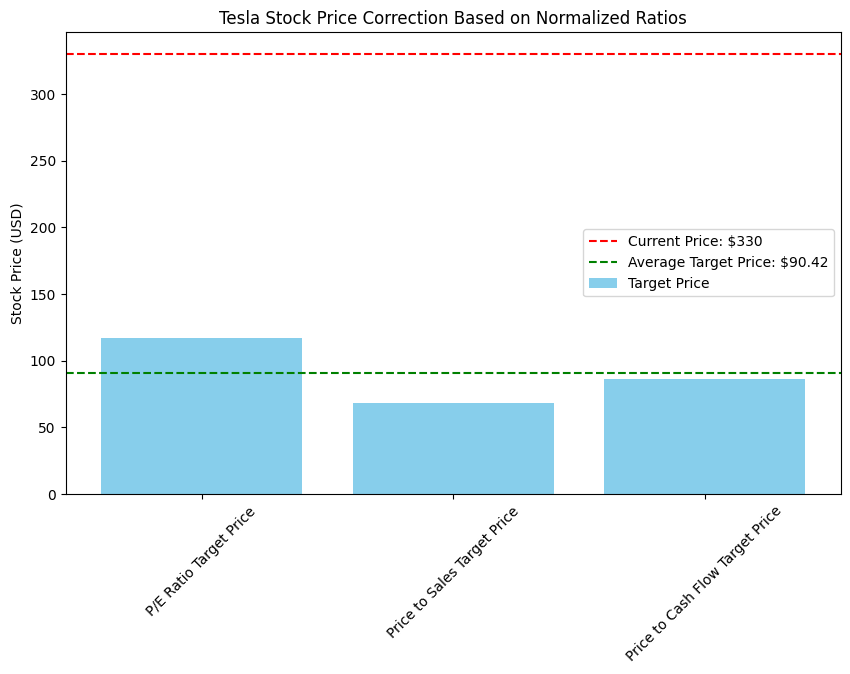

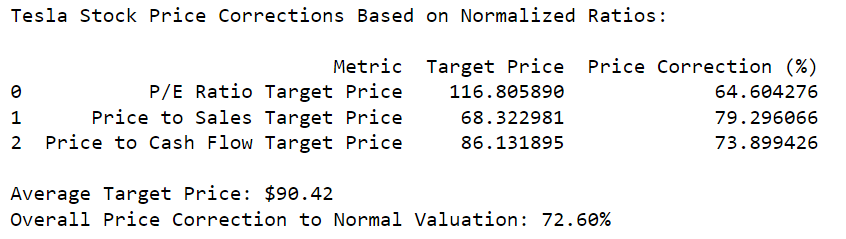

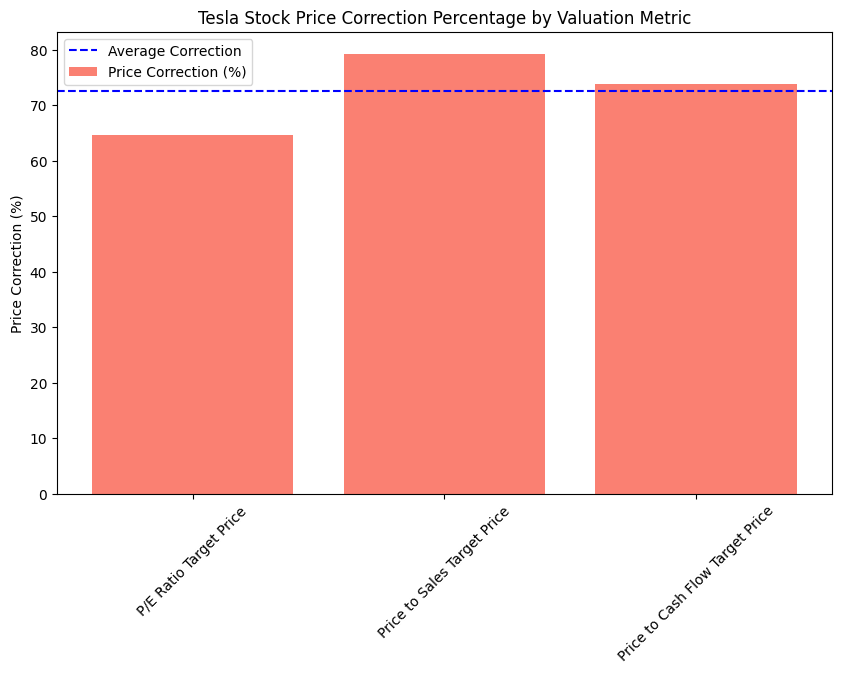

Tesla stock price target $90.42 overall stock price correction -72.6% to normal valuation

On the basis of available stock market data and Tesla’s financial ratios, a normalising average P/E Ratio range of 20 | 25 is typical for the auto industry, while also using Tesla’s trailing twelve months (TTM) earnings, we’ll calculate what stock price would correspond to a P/E ratio of 25. Results are of an average target stock price of $90.42 and the current Tesla $330 stock price will need a -72.6% correction to normalise to an average industry 20|25 P/E Ratio.

Relevant ratios such as Price to Sales, Price to Book and Tangible Book value also explain how the current Tesla stock price valuation has been extremely high in markets and investors run the risk of being impacted by volatile share price declines. In fact, A typical Price-to-Sales ratio for auto or tech companies often falls between 1-5. Tesla’s current ratio of 24.15 suggests the price could be overvalued relative to sales and may need further adjustment. Price to Book and Tangible Book: Normalizing these ratios (currently 11.95 and 12.02 respectively) to around 3-4 would also imply a significant reduction in price.

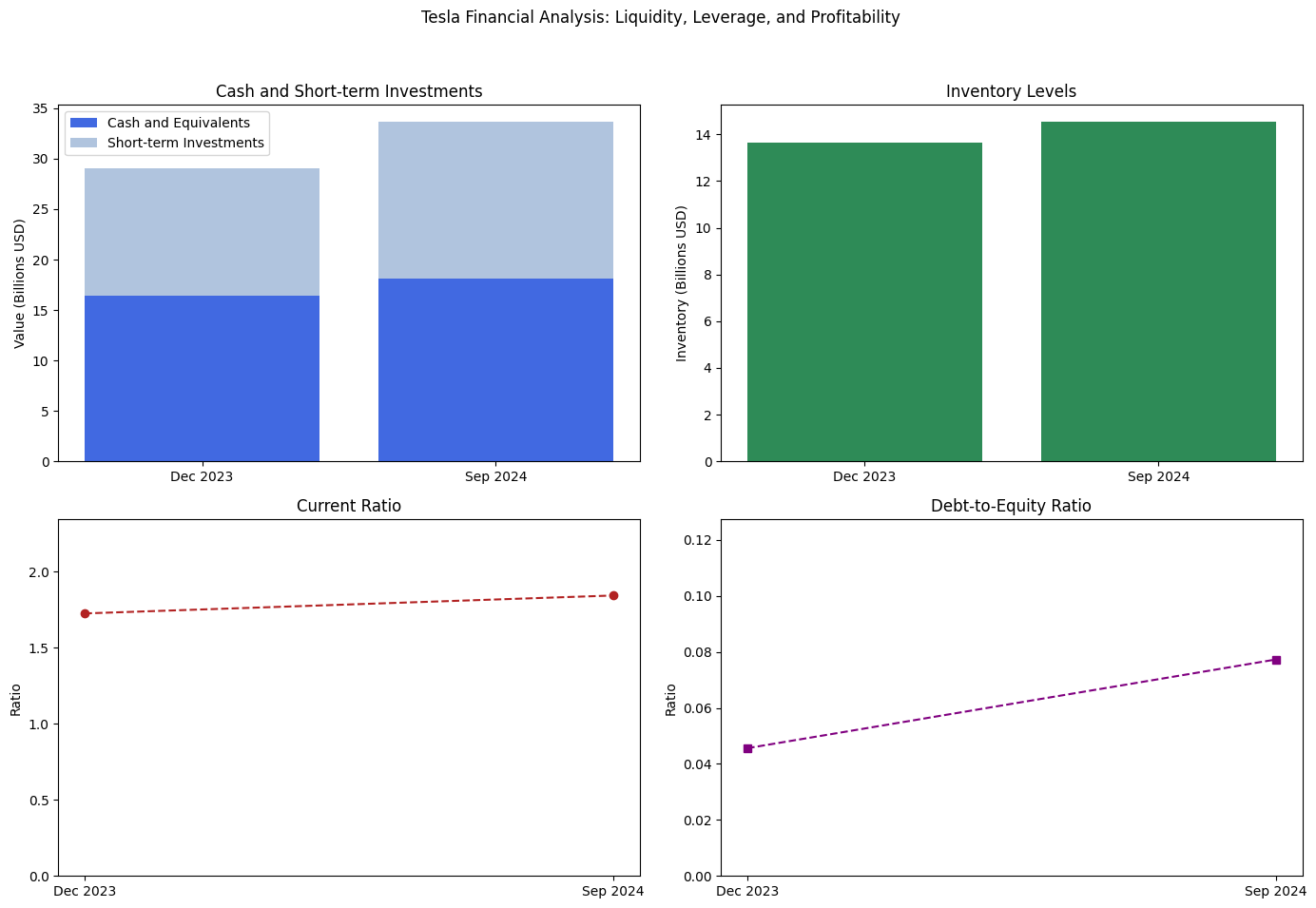

Tesla’s balance sheet has been resilient, but the operating margin will be under pressure

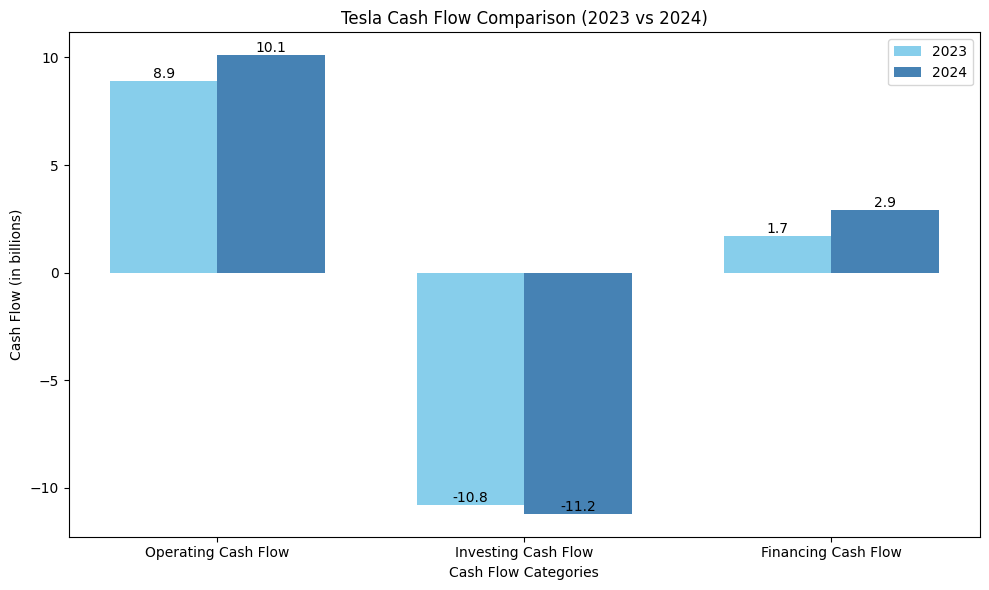

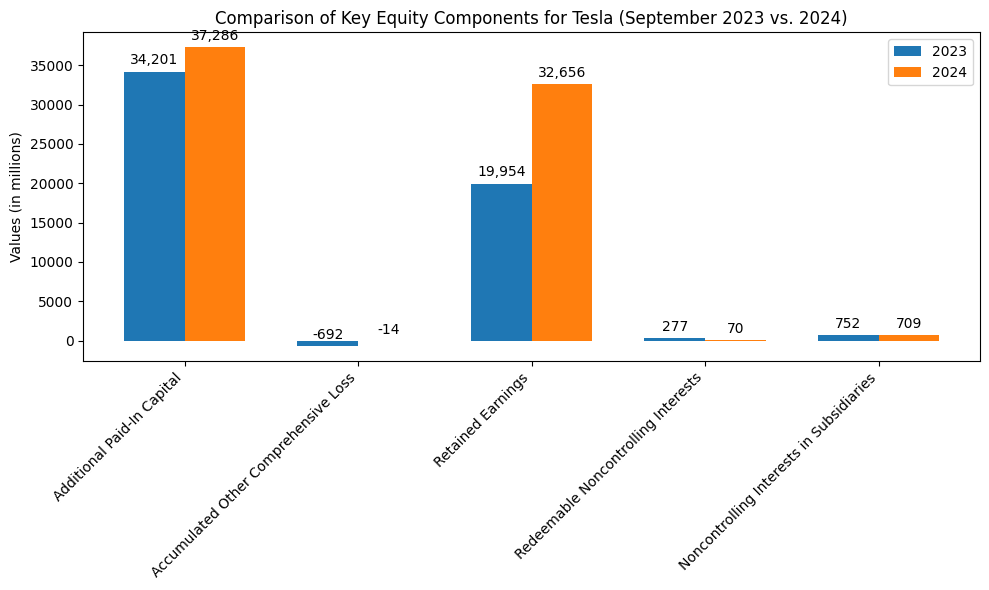

Tesla’s balance sheet has remained resilient, supported by strong liquidity, growing cash reserves, and manageable levels of debt, which provides the company with a solid foundation to weather short-term market fluctuations. The company’s cash flow from operations has been consistent, and its free cash flow generation remains positive, allowing Tesla to fund its capital expenditures and innovation without resorting to significant external financing. However, despite this strong balance sheet, Tesla is likely to face increasing pressure on its operating margins in the coming quarters. The global automotive market is experiencing a slowdown, and Tesla’s car sales are expected to be impacted by declining demand, higher competition, and potential pricing pressures. Additionally, as production costs rise due to supply chain challenges and inflationary pressures, Tesla’s operating margins may come under strain. While the balance sheet can absorb short-term shocks, the combination of slower sales growth and narrowing margins could challenge Tesla’s ability to sustain its current profitability levels, potentially undermining investor expectations for future earnings growth.

Impact on Market Capitalization:

Tesla’s market capitalization would shrink significantly. With the current share count of approximately 3.21 billion shares, a stock price of $90 would imply a market cap of roughly $288.9 billion (3.21 billion shares × $90). This is a sharp decline from its current market cap near $1.06 trillion. Such a drop could signal a loss of investor confidence, which could influence Tesla’s ability to raise capital at favourable terms in the future. Equity and Leverage Impact: A drop in market capitalization could erode shareholder equity, leading to a higher debt-to-equity ratio. While Tesla’s debt levels have been relatively manageable, a substantial decrease in equity value could make its debt burden appear more significant relative to its market value. This could raise concerns among creditors and investors regarding Tesla’s solvency. If the stock price correction reduces Tesla’s equity base, its leverage (both financial and operational) could increase, potentially leading to higher risk . Operational Risk and Margin Pressures: If the correction implies that future profits will be lower than previously forecasted, this could also affect the company’s ability to generate enough operational cash flow to finance ongoing research and development and scaling efforts. This could in turn affect Tesla’s ability to maintain its competitive edge in the market, particularly as other car manufacturers ramp up their electric vehicle (EV) offerings. Tesla’s operating margins could be under pressure if demand for its vehicles slows due to global market conditions. With a reduced stock price, the company might have less flexibility in its operations. A lower stock price could result in fewer resources for investment in new technologies, production expansion, and innovation.