The latest batch of European macroeconomic data, culminating in the September figures from France and Spain, confirms that the continent is firmly on a disinflationary path, though with significant divergence between its major economies. The overall trend is being driven by a moderation in core components and falling energy prices, allowing the European Central Bank (ECB) to maintain a more balanced policy stance. However, the persistence of services inflation and new geopolitical headwinds require continued vigilance.

France: Disinflation Gains Momentum

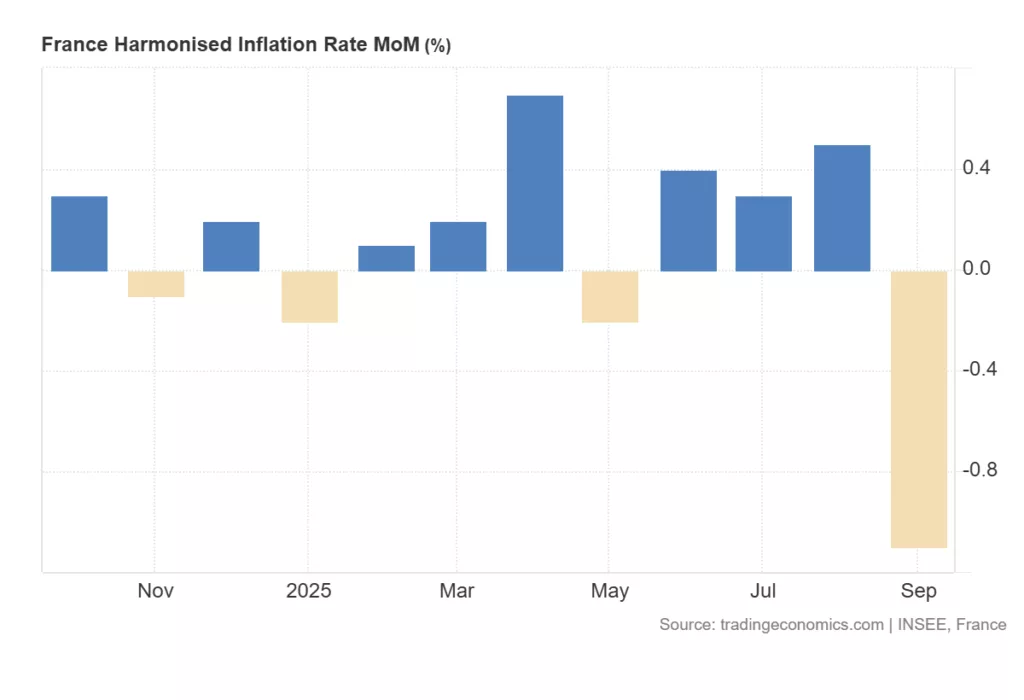

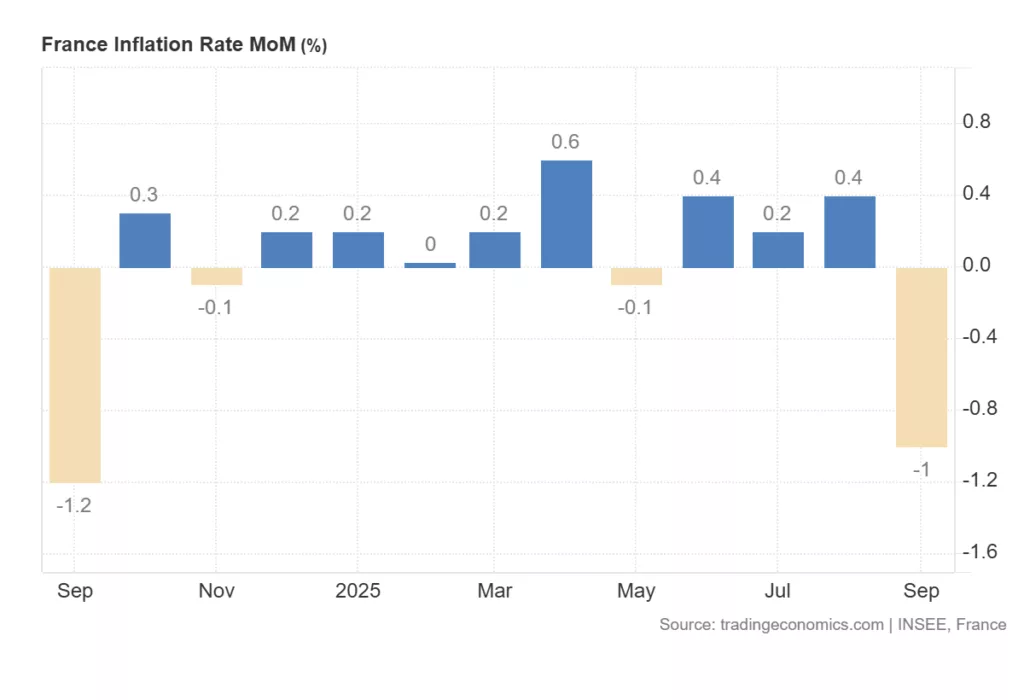

The final September data for France confirms a significant acceleration in its disinflation process. The year-on-year inflation rate rose to 1.2%, up from 0.9% in August, reaching its highest level in eight months . However, this headline figure masks a more complex underlying dynamic; data suggests that while some domestic, service-oriented price pressures persist, the overall inflationary environment in France is cooling rapidly.

- Services-Driven Uptick: The increase was largely driven by a rise in services inflation, which accelerated to 2.4% from 2.1% in August, with notable increases in health service costs .

- Easing Energy Deflation: The decline in energy prices was less pronounced in September (-4.4% vs -6.2% in August), contributing to the higher headline figure .

- Sharp Monthly Decline: A telling sign of weakening price pressures is the significant monthly drop. The Consumer Price Index (CPI) fell by -1.0% month-on-month, the sharpest decline in a year, primarily due to seasonal drops in service prices such as accommodation and transportation .

Spain Inflation In Line With Consistent Economic Growth

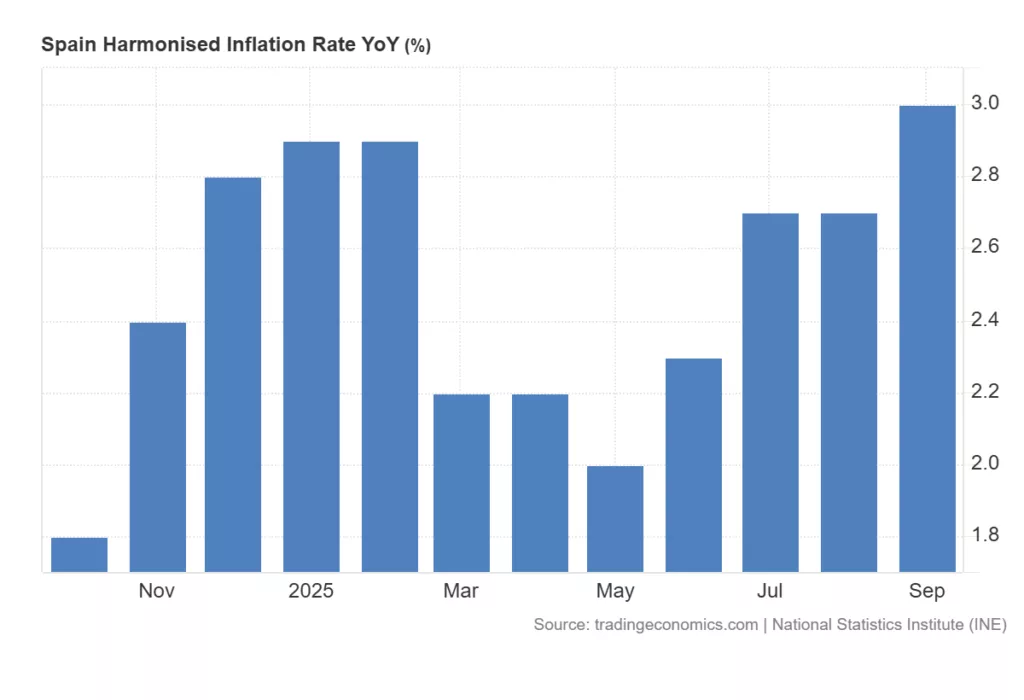

In contrast to France, Spain’s inflation picture remains more resilient. The annual inflation rate for September was confirmed at 3.0%, an increase from August’s 2.7% and significantly above the euro area average . This highlights the uneven nature of the inflation fight across the Eurozone. Spain’s figures demonstrate that inflationary pressures, particularly in the core components, are proving stickier than in some of its northern neighbors, a factor the ECB must weigh in its policy deliberations.

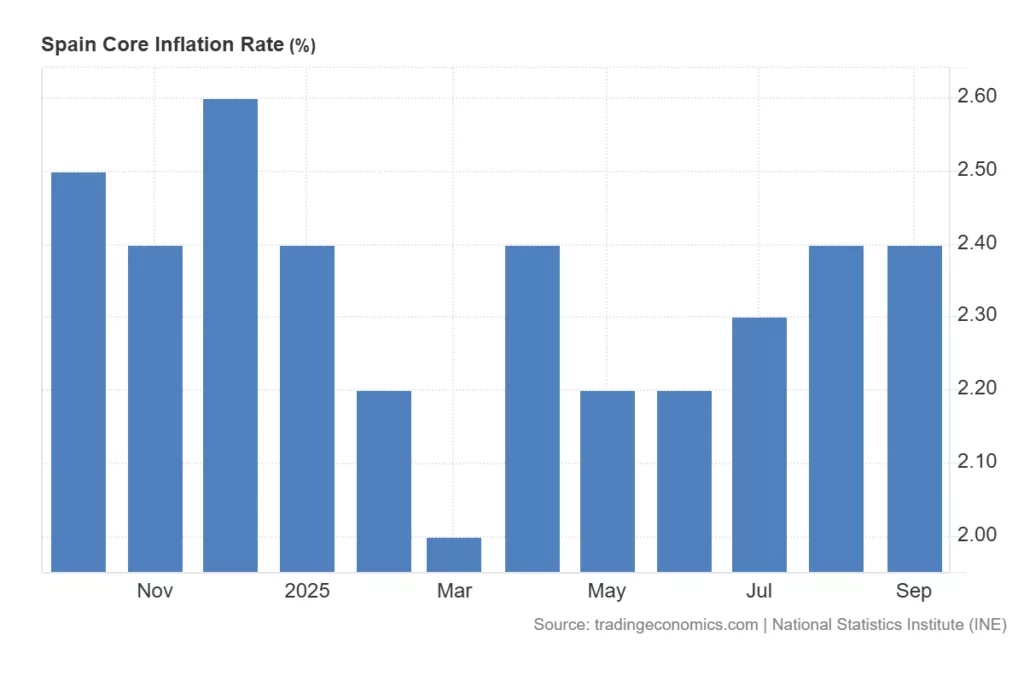

- Core Inflation Persistence: A key metric watched by the ECB, the core inflation rate (which excludes volatile food and energy prices), was finalized at 2.4% year-on-year . While high, it’s important to note this was slightly lower than the forecast of 2.3%, indicating a potential, albeit slow, moderation.

- Contained Monthly Movement: On a monthly basis, both the harmonised and standard inflation rates showed minimal change, at 0.1% and -0.4% respectively, suggesting a stabilization of price pressures at this higher level .

The ECB’s Balancing Act in a New Macro Context

The latest national data aligns with the broader projections from the ECB. The September 2025 ECB staff projections see headline inflation stabilizing around 2% for the rest of 2025, before dropping to 1.7% in 2026 and recovering to 1.9% in 2027 . The current disinflation is attributed to several factors:

- Moderating Wage Growth: As workers have largely recouped past real wage losses, wage growth is expected to slow, leading to significantly slower unit labour cost growth .

- Subdued Foreign Demand: Global trade growth is projected to decline significantly, with euro area foreign demand expected to slow to 1.4% in 2026, reducing imported inflation .

- Policy Impacts: The appreciation of the euro is also helping to curb goods inflation by making imports cheaper .

However, the outlook is not without risks. The ECB has noted that “services inflation remains elevated” and that new trade tariffs and geopolitical tensions pose upside risks to both inflation and economic growth . The IMF has also cautioned that Europe faces “high energy costs, and technological change” alongside “high public debt and weak medium-term growth prospects,” creating a challenging policy environment . The European economy is navigating a delicate transition, while the disinflation process is well underway, as clearly seen in the French data, allowing for a less restrictive monetary policy. However, the lingering inflation in services, as evidenced by Spain, and significant external uncertainties mean that policymakers cannot yet declare victory. The path to sustainably stabilizing inflation around the 2% target will require a careful and data-dependent approach in the months ahead.

Economic Bulletin Issue 5, 2025