Bund’s Yield Curve Term premium to steepen in longer duration

Germany’s prevailing uncertainties and projected macroeconomic landscape will necessitate a higher term premium on long-duration Bunds. This is driven by embedded higher inflation expectations and increased ECB interest rates.

The steepening of the 10Y to 30Y Bund Yield will likely be driven by an increased term premium and heightened inflation expectations. Germany’s economy may need procyclical fiscal deficits to support investments in diversifying productive capacities, particularly in the automotive and renewable energy sectors. These investments necessitate consistent fiscal support and procyclical budget deficits, which Germany can afford due to its consistent primary account surplus.

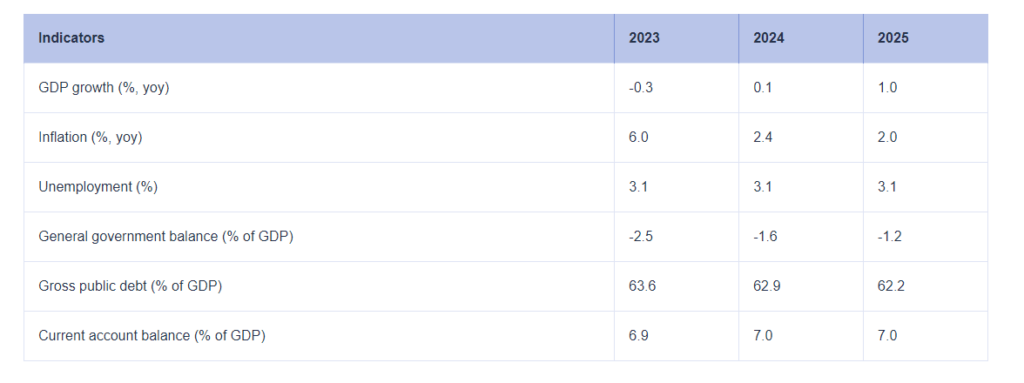

ECB macroeconomic indicators do forecast sluggish stagnating economic output while Inflation Expectations are likely to stabilise at around the 2.0% aim, while the General Government Balance percentage to GDP is forecasted to have mild deficits, that can be anticipated to become larger for the German economy to turn around from the quagmire of economic stagnation and unemployment.

In very simple terms, longer-duration issuance Bunds would probably be required to price a slightly higher term premium, to compensate for higher inflation expectations and Fiscal expenditures. In the graph below the 30Y BUXL Yield should price a range of 2.75% | 2.85% with 25 to 30 basis points drift

Similar 10Y Bund yield premium dynamics could be required to be priced in markets where the 10Y Bund should rise to 2.68% | 2.7% range with a 30 | 33 basis points drift.