Asian session has been characterized by a rebound in equity markets, driven by dovish signals from the U.S. Federal Reserve, which helped offset persistent concerns over U.S.-China trade tensions and deflationary pressures in China.

Market Performance Overview

| Stock Index | Performance (Oct 15, 2025) | Factors |

|---|---|---|

| Japan – Nikkei 225 | +1.53% | General market rebound, weakening dollar against the yen. |

| South Korea – Kospi | +2.15% | Strong performance from market heavyweights like Samsung Electronics . |

| Hong Kong – Hang Seng | +1.21% | Sustained momentum from IPO surge; attractive valuations. |

| Australia – ASX/S&P 200 | +0.85% | Broad-based regional rally. |

| China – Shanghai Composite | ~+0.1% | Cautious sentiment due to data and trade tensions; technical charts indicate “Sell” . |

| India – Nifty 50 | +0.43% (from previous close) | Technically neutral; investors watching corporate results (e.g., TechM, Infosys, Vedanta) |

Macroeconomic Data & Regional Context

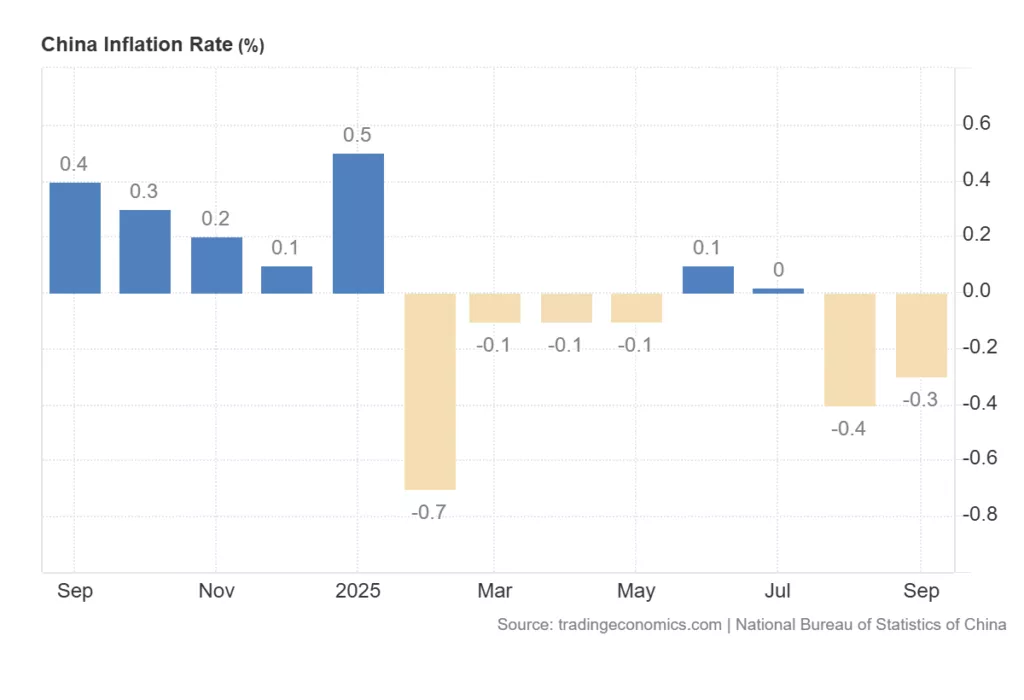

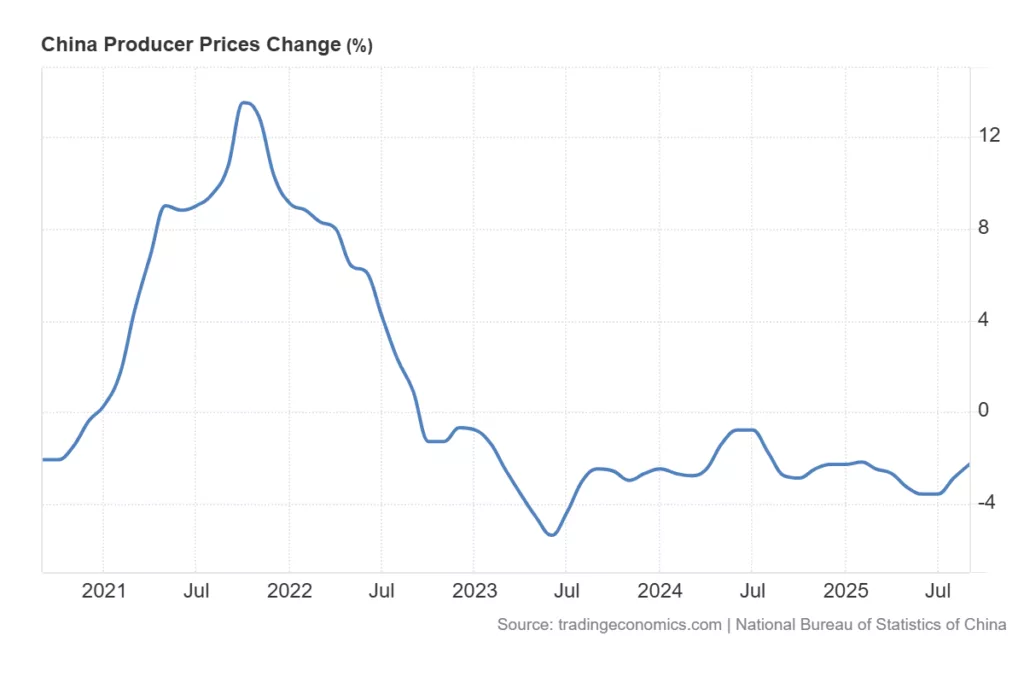

- China’s Deflationary Pressures: China’s September economic data confirmed ongoing deflationary trends. The Consumer Price Index (CPI) fell -0.3% year-on-year, a sharper decline than the 0.2% forecast. The Producer Price Index (PPI) fell -2.4% year-on-year, persisting in negative territory and indicating weak demand and falling margins for industrial companies.

- IPO Pivot to Hong Kong: There is a clear shift of Chinese listings from the U.S. to Hong Kong. Chinese IPOs in the U.S. have slumped, raising only $875.7 million year-to-date, down 93% from the same period in 2021. Conversely, Hong Kong has seen a 164% surge in IPO value, raising $18.4 billion, positioning it to become the world’s largest listing destination this year.

- Broader Regional Outlook: The ASEAN+3 region (including China, Japan, South Korea, and Southeast Asia) is positioned for resilience despite global trade shocks. Growth is increasingly driven by domestic demand and diversified export markets. However, the rgion faces significant headwinds from unprecedented global tariff escalation. In Southeast Asia, Q2 2025 saw stronger growth as businesses front-loaded activities during a temporary tariff pause, though a more challenging H2 is expected as these effects dissipate.

Nikkei225 Speculation vis a vis Japan Decreasing Industrial Production

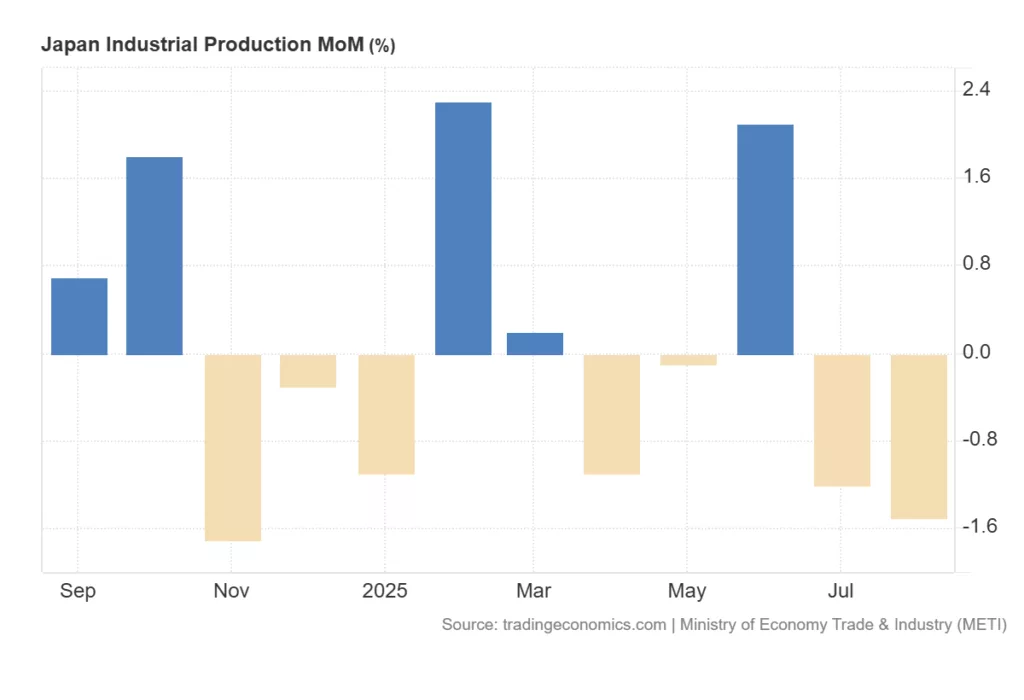

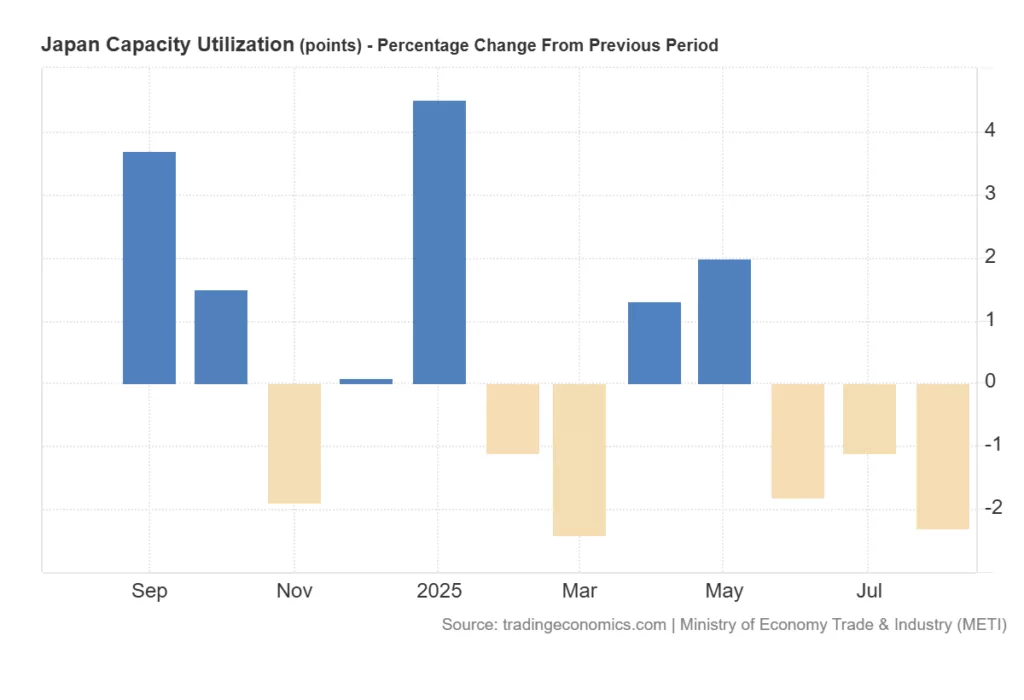

The speculative activity in Japanese stocks received its last boost, on the back of the newly Japanese Geisha showgirl wanna be Margaret Thatcher, with a clear simple and sexy receipe: more Japanese Yen Depreciation, More Fiscal Deficit and More Public Debt, just what Japan needs to blow the Dollar/Yen liabilities carry trade. The announcement of the newly Japanese wanna be Iron Lady with a softy softy mochi sweet-heart has done so good that every Japanese worker has been so distracted from work, in so far, Japan’s August data shows a notable decline in capacity utilization by -2.3% month-over-month, a sharper fall compared to the -1.1% expected and follows a previous positive 0.7% reading. This points to weakening industrial activity as firms are operating significantly below their potential output levels. Concurrently, industrial production also decreased by –1.5% month-over-month, worse than forecasts, and declined -1.6% year-over-year, signaling a broader contraction in manufacturing output. This trend of reduced capacity use and falling production reflects subdued demand conditions and cautious corporate sentiment amid an environment of economic uncertainty and political instability. The recent 20-year Japanese Government Bond (JGB) auction saw a yield around 2.67% amid solid investor demand, which also suggests expectations of persistent economic challenges and moderate inflation pressures. Taken together, these indicators reveal a macroeconomic backdrop for Japan characterized by slowing industrial momentum and cautious market sentiment, likely impeding robust economic growth in the near term

Market Drivers & Investment Implications

Comments from Federal Reserve Chair Jerome Powell were a primary catalyst for the market rebound. He signaled rising concerns about the U.S. labor market and hinted that the end of the Fed’s quantitative tightening program is near. This reinforced market expectations for potential rate cuts in October and December, supporting risk assets globally. Markets remain fragile due to ongoing trade friction. Recent developments include threats of additional 100% tariffs on Chinese goods and the imposition of new port fees. This volatility is particularly impactful on technology stocks, which are hypersensitive to trade issues due to their reliance on Chinese supply chains and consumer markets. Amidst the geopolitical and economic uncertainty, investors have been flocking to gold, which soared to new record highs above $4,200 per ounce. The U.S. dollar also eased slightly as Fed cut bets increased.

What Traders Should Look For During Europe and Americas Session

Traders shoud be looking for their bitch of the day, the tech sector will be once more in focus and sensitive to any headline on U.S.-China trade, also considering the deflationary data from China would be spinned around as China dumplings. In the FX market traders should continue monitoring any volatility in the Japanese Yen as the currency continues to depreciate while also creating inflationary pressures on the economy. To see live FX Market go on this page FX – Capital Market Journal.

The Asian market rebound demonstrates investors bias toward the Federal Reserve monetary policy and potential decrease in Fed Fund Rates,despite the same Central Bank and the wider forecaster industry travelling blind for the lack of data and the ongoing Government Shutdownm, probably nowhere near to be resolved. While China deflationary input costs generate hopes over trade friction fears. However, with deflation persisting in China and the threat of further tariffs looming, the current optimism stands on fragile assumptions.