Q1 2025 Seasonal Volatility and Stock Market Correction: A Forecasting Analysis

The first quarter of 2025 may bring increased stock market volatility, potentially leading to a market correction. A detailed analysis of major U.S. indices, including the Dow Jones Industrial Average (DJIA), S&P 500, NASDAQ 100, and Russell 3000, suggests that…

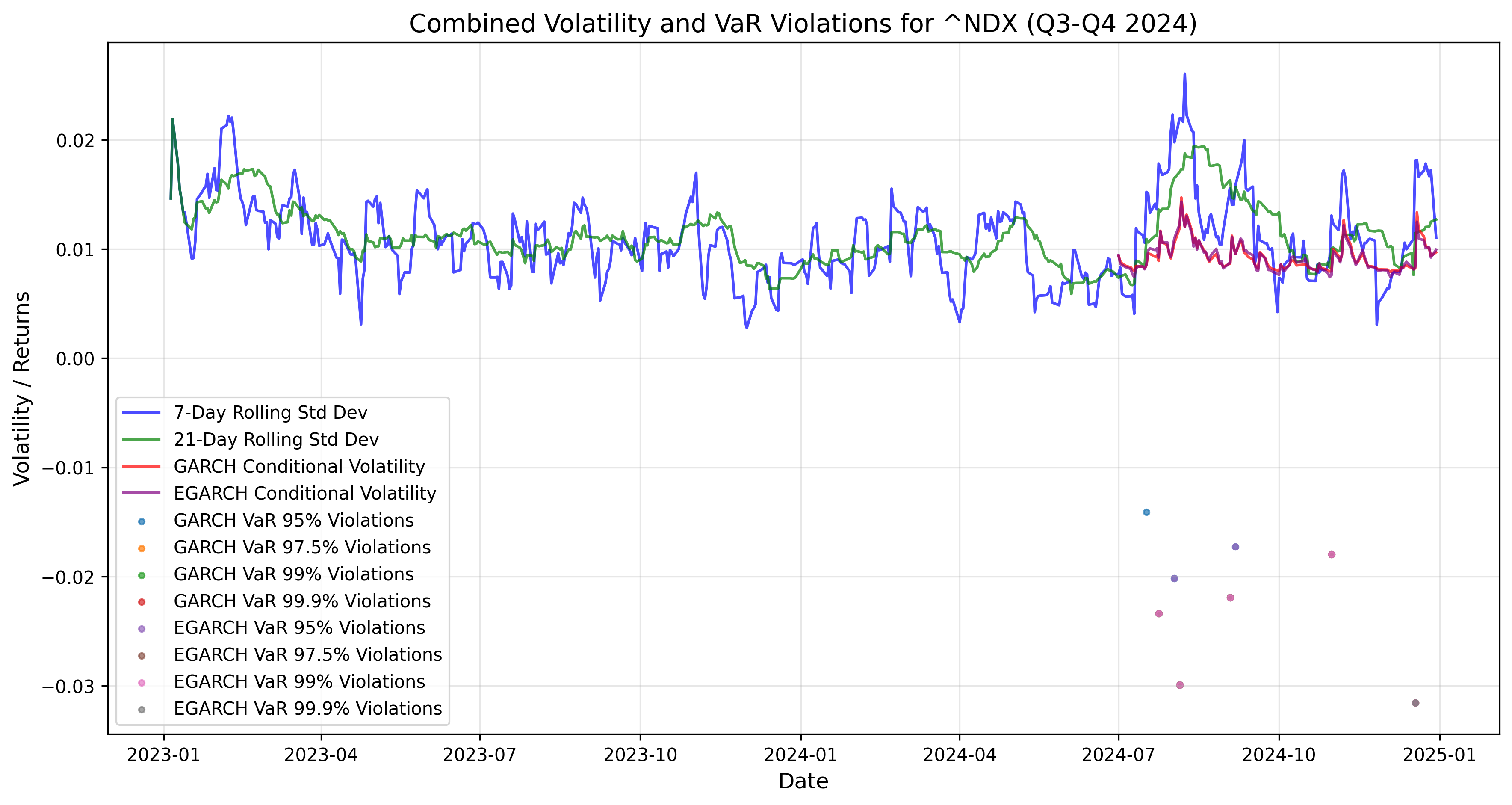

Leverage effect could bring seasonal Q1 stock market drawdown

The recent Q4 volatility patterns of the major U.S stock market Index, such as Dow Jones Industrial Average, S&P500, Nasdaq100 and Russell 3000 could have been a forthcoming market signal of a volatility build-up going into Q1 2025, as among…

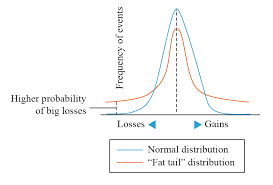

Forecasting Value-at-Risk under Fat-Tail Distribution Assumptions

Financial Econometrics studies have demonstrated that forecasting Value At Risk under standard normal distribution conditions could lead to underestimation of potential losses, hence of fat tail volatility risk events, other methods to improve Value At Risk forecasting have been studied…