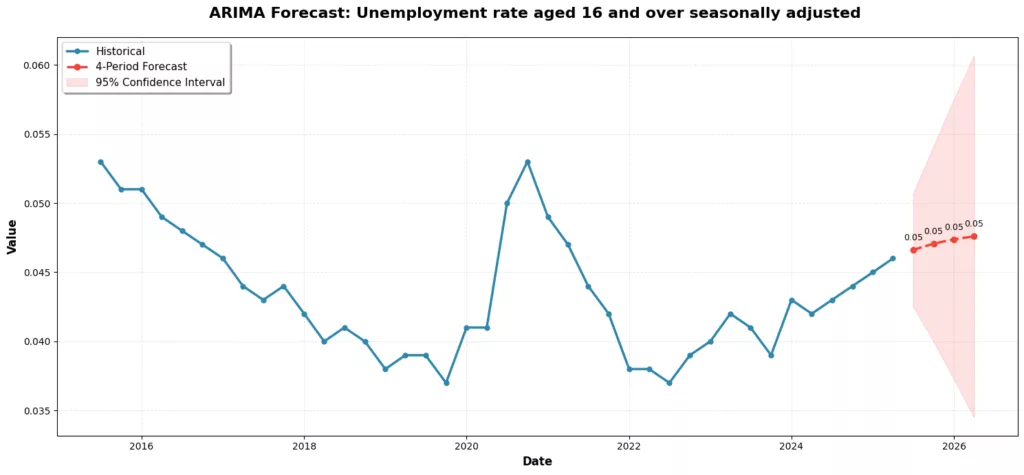

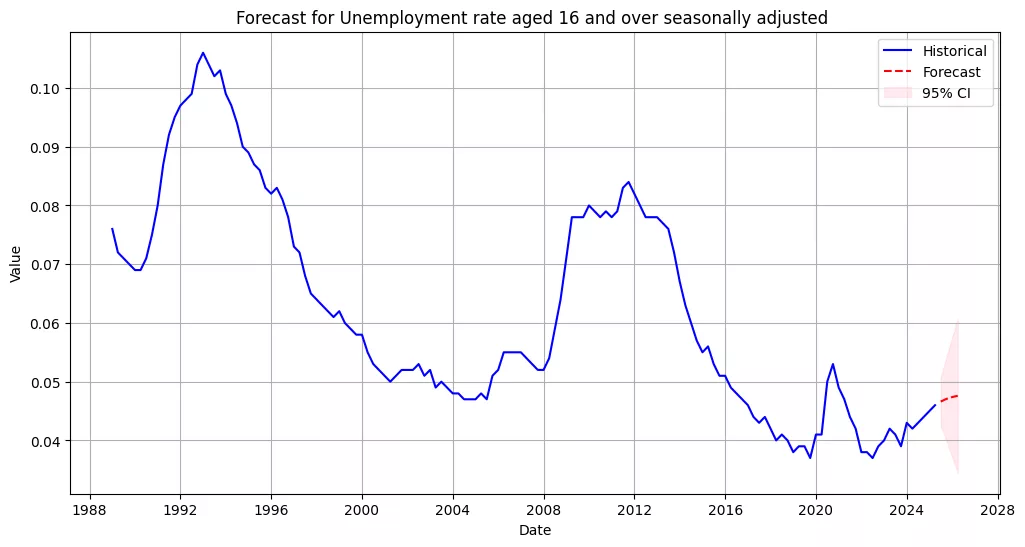

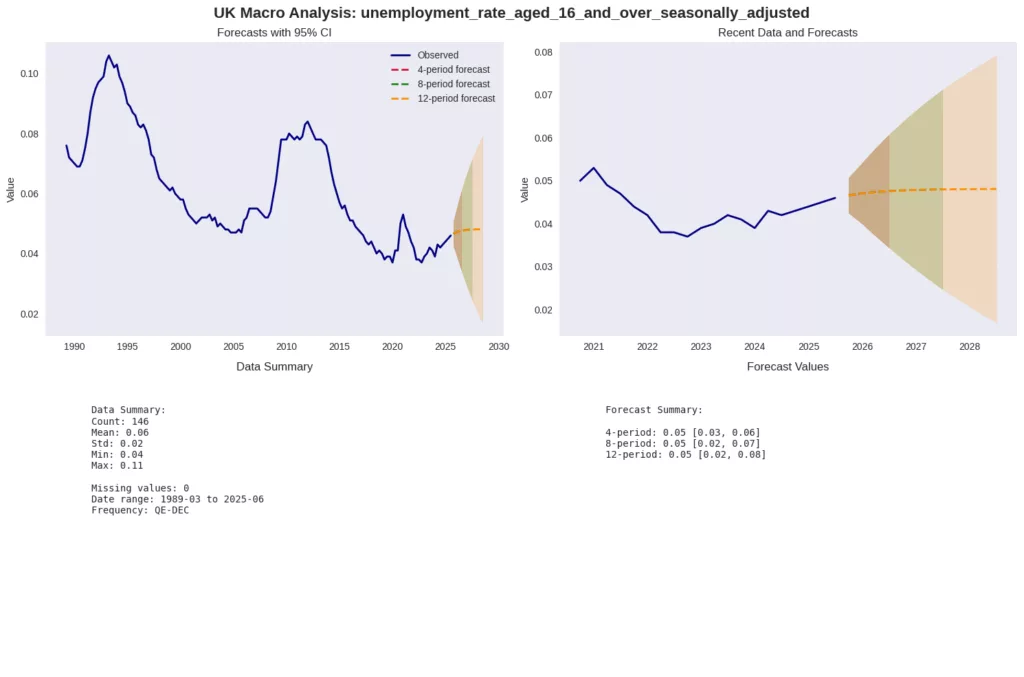

Among Many Economic Data starting the week after a long week-end with celebrating Columbus Day, Macro-Economic data this morning, confirm the rising trend in unemployment for the broader UK economy, exactly as my forecast shows below, the wider UK Unemployment rate has been forecast to increast toward 5% in the coming months and quaters, with a confidence interval range 4.76% up to 5.5%, according to my estimates. The hard data show how Payroll Employment declined to 10k in September, while Claimant count increased to 25,800. Rising unemployment will provide room for the Bank of England to continue evaluating the output gap, also in light of the upcoming Fiscal Budget, while on the other side of the scale, the Bank of England and the Exchequer have to grapple with higher and sticky inflationary input costs across the wider economy, which make the monetary policy and fiscal policy balance not a simple exercise.

Among Many other Economic Data starting the week after a long week-end we have :

Germany & Euro Area:

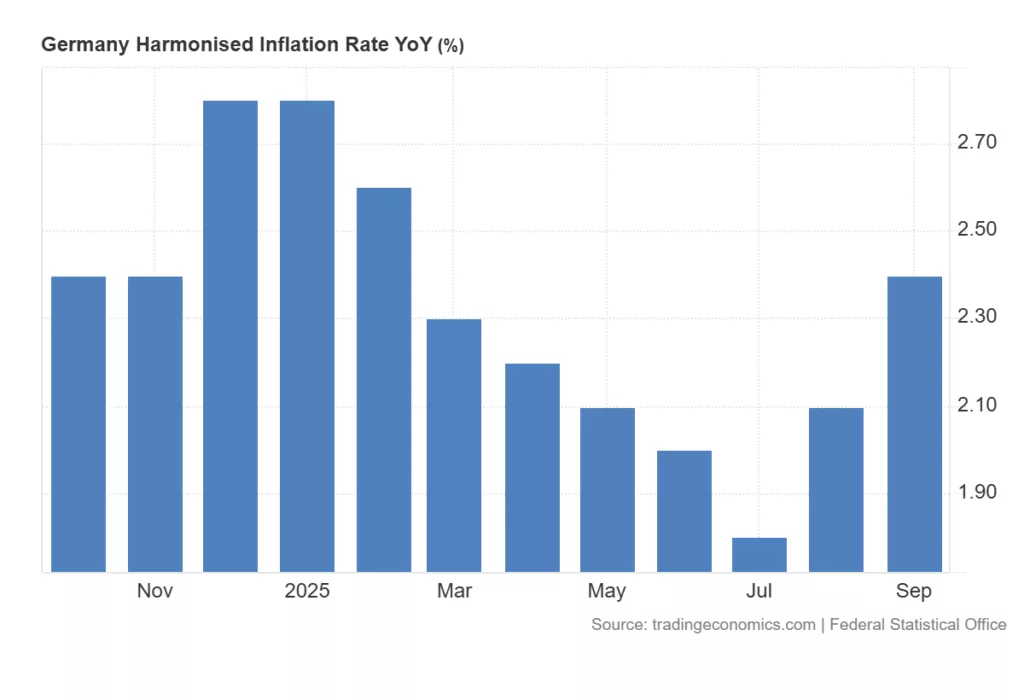

- Inflation rates for September confirmed at 2.4% y/y, just above the previous month (2.2%), keeping the ECB firmly focused on persistent price pressures.

- ZEW sentiment fell, signaling rising skepticism on growth outlook.

Singapore:

- Q3 GDP advanced 1.3% q/q (prev. 1.5%), with annual y/y growth at 2.9% (prev. 4.5%), flagging slower momentum as export demand softens.

Australia:

- NAB business confidence rose to 7 in September from 4 prior, with RBA minutes underscoring persistent inflation and rate-hold outlook.

India & South Africa:

- India’s WPI inflation decelerated to 0.13% y/y, food prices negative at -1.99% y/y, and fuel WPI fell -2.58% on global oil weakness.

- South African business confidence climbed to 121.1 in September, but mining output slipped.

| Indicator | Latest | Previous | Consensus | Trend/Comment |

|---|---|---|---|---|

| UK BRC Retail Sales Monitor YoY (Sep) | 2% | 2.9% | 2.5% | Growth slows; inflation |

| UK Unemployment Rate (Aug) | 4.8% | 4.7% | 4.7% | Up; labor market softens |

| Germany Inflation YoY (Sep, Final) | 2.4% | 2.2% | 2.4% | Persistent inflation |

| Euro Area ZEW Sentiment (Oct) | 22.7 | 26.1 | 30.2 | Lower; caution prevails |

| Italy 10Y BTP Auction (Oct) | 2.23% | 3.62% | — | Yields lower; demand up |

| Oil-Brent (spot) | $63.56/bbl | — | — | Supply fears |

| Gold (spot) | $4,150/oz | — | — | Safe haven demand |

| U.S. GOVT ETF Flows | +$1B | — | — | Risk-off behavior |

Global Financial Assets Overwiev

Markets remain cautious as investors weigh slowing global growth and mixed inflation signals against persistent central bank uncertainties, while asset rotation continues toward safe havens and defensive structures across bonds, gold, and government ETFs.

Bonds

European sovereign bond yields are generally lower this morning, reflecting persistent caution among investors. The Italian government’s latest BTP auctions recorded notably reduced yields, with the 10-year at 3.43% (previous 3.62%), the 15-year at 3.87% (previous 4.03%), and the 3-year at 2.36% (previous 2.44%), demonstrating stable demand for Italian debt, although the 7Y BTP auctioned at 3.05% a significant bp/s tail of 0.29% from the previous 7Y bond auction yield 2.76%, sign of longer duration global sovereign debt market convexity steepening of the yield curve. Germany’s 2-year Schatz auction yield dropped to 1.91% from 2.01% last month, mirroring continued “risk off” sentiment in Eurozone fixed income markets. Yields on government bonds remain subdued globally, with investors seeking safety due to growth concerns, fluctuating inflation, and policy uncertainty.

Currencies

Currency markets reflected moderate volatility. The U.S. dollar continues to hold firm after President Trump’s recent remarks on trade, which sparked calming of geopolitical tensions. The euro is stable near $1.1588. The Japanese yen strengthened to 151.72 per dollar in response to renewed caution. Emerging market currencies are subdued; the British pound weakened marginally as wage and employment data undershot forecasts, and the trend mirrors caution expressed in European bond auctions.

Commodities

Commodities are delivering a mixed picture. Gold set new highs above $4,150/oz in response to risk aversion, while silver similarly reached all-time highs on continued safe-haven flows. Oil prices have been decreasing after rebounding—Brent at $6.56/bbl and WTI at $59.23/bbl—driven by OPEC’s forecasts for tighter balances, as the IEA report today echoed supply concerns, intraday Globa Oil Market see WTI $58,09 declining -2.38%, while Brent $61.85 declining -2.31%. Copper is stable on tight supply, but other industrial metals, including platinum and iron ore, have seen pressure on softer demand and trade uncertainty, in fact also Copper Price $4.9 are declining -4.15%, as a sign of Global Demand Recession and slower economic activity in the coming quarters. South Africa’s gold and mining sector posted mixed results, with August gold production down -3.6% y/y and overall mining output falling -0.2% y/y, highlighting weakness in basic materials. Indian WPI inflation slowed sharply in September, reflecting cheaper fuel and moderating manufacturing costs.

ETFs

ETF flows suggest investors are favoring defensiveness. Nearly $1 billion flowed into the iShares U.S. Treasury Bond ETF (GOVT), with government and gold ETFs attracting continued demand as equity exposure receded. Stock index ETFs faced net outflows (notably SPY and QQQ), evidencing risk rotation, while sector-specific ETFs (technology, internet) remain volatile. New ETF listings on Nasdaq offer fresh leveraged options for active traders today.

Equity Markets

Stock indices globally are subdued as investors digest growth and inflation data. European equities are trading lower, pressured by weaker German and Euro Area ZEW economic sentiment (22.7 for euro area, 39.3 for Germany in October, below consensus), and deep negative readings for current conditions in Germany (-80.0 vs -76.4 prior). Asian equities are mixed as Chinese vehicle sales surged 14.9% y/y in September, but broader growth remains uncertain.