Global markets had a dynamic against a backdrop of shifting yields, commodity surges, and headline economic releases. This Capital Market Journal morning briefing compiles overnight data, market movers, cross-asset updates, and implied impacts—all giving investors critical orientation for portfolio decisions as the trading day begins.

Australia Consumer Confidence

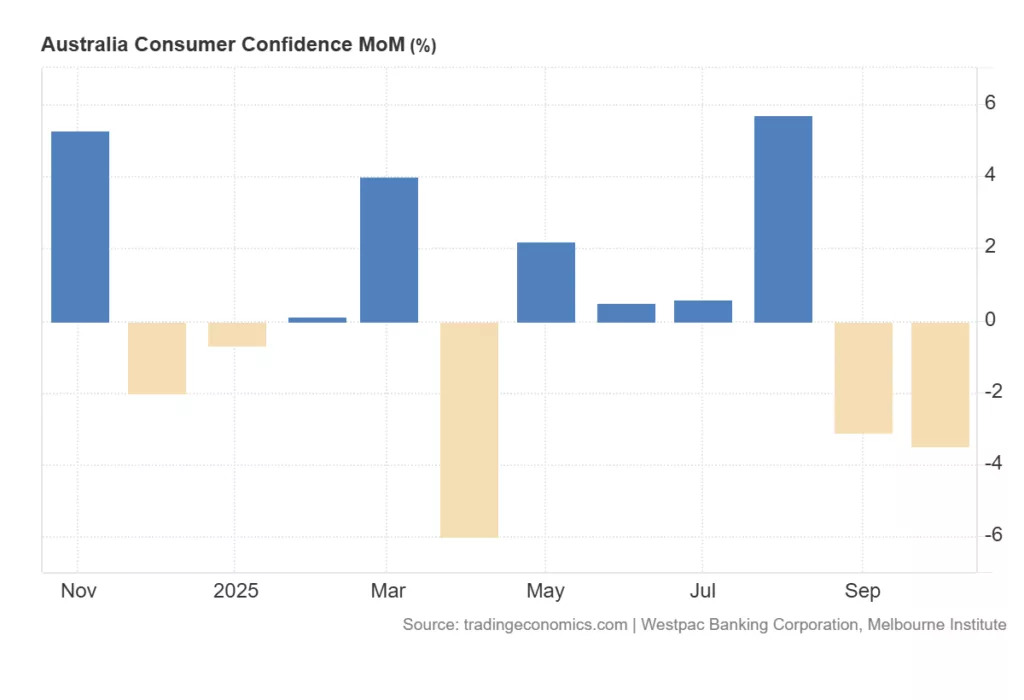

Australia’s Westpac-Melbourne Institute Consumer Sentiment Index fell by -3.5% month-over-month to 92.1 in October, marking its fastest drop since April and erasing gains made between May and August.

- Household views on family finances weakened with past year conditions dropping 4.8% to 82.1 and 12-month outlook plunging 9.9% to 97.1, the lowest in over a year.

- Broader economic sentiment showed a mixed picture with the 12-month outlook down 2.5% to 89.9, a one-year low, yet the 5-year outlook slightly improved by 1.4% to 94.0.

- The index for “time to buy a major household item” declined 1.1%, while unemployment expectations fell 2.9% to 127.6, slightly below the long-run average of 129.

- Mathew Hassan, Head of Australian Macro-Forecasting, noted households are unsettled by recent inflation trends, and while a cash rate cut in November is not guaranteed, it remains a possibility.

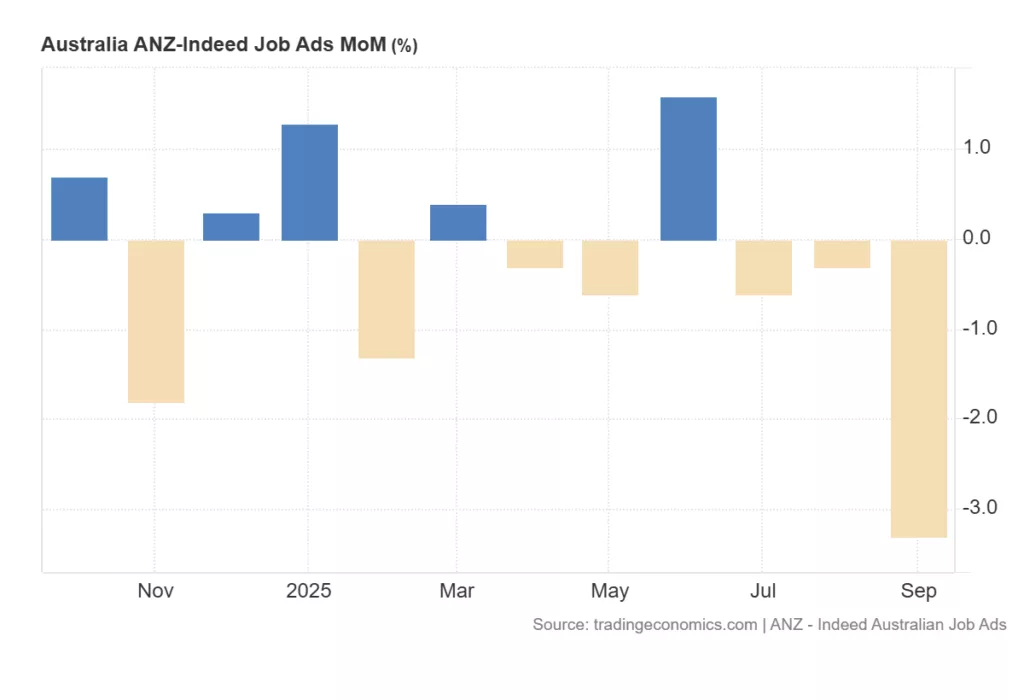

- ANZ-Indeed Australian Job Ads fell -3.3% month-on-month in September 2025, a much steeper drop than the downwardly revised 0.3% decline in the previous month. It was the third consecutive monthly decrease in job ads after holding broadly steady for over a year, marking the sharpest fall since February 2024 and adding to concerns about the labour market outlook.

Japan Household Spending

Household spending in Japan rose 2.3% year-over-year in August 2025, surpassing the market consensus of 1.2% and marking the fourth consecutive month of growth.

- On a monthly basis, spending rose by 0.6%, above expectations of 0.1%, though slower than July’s 1.7% gain.

- Key categories driving growth included transportation & communication (up 13.5%), education (up 16.9%), clothing & footwear (up 5.4%), and culture & recreation (up 12.2%).

- Spending on essentials such as food (-1.2%), housing (-0.7%), and furniture (-6.8%) declined, reflecting shifting consumer priorities amid inflation.

- Household income adjusted for inflation rose 2.8% year-over-year, supporting resilience in private consumption despite rising tariffs and inflation pressures.

Markets: Risk on, Risk off Implications

- The decline in Australian consumer confidence signals caution among households amid inflation uncertainties and interest rate worries, indicating potential domestic demand softness ahead. The possibility of a rate cut offers mixed cues to markets about monetary policy direction.

- Japan’s robust household spending growth reinforces the country’s economic resilience and supports the case for a gradual policy tightening timeline by the Bank of Japan. Increased spending on transport and leisure indicates improving consumer discretionary demand despite global tariff challenges.

Bonds and Central Bank Moves

Yields on US 10-year Treasuries have risen to 4.16%, reflecting sustained uncertainty linked to political disruptions and the federal government’s ongoing shutdown. Investors are lengthening maturities to lock in high rates, a trend also visible in global debt markets where dollar benchmarks offer 4.24–4.93%, and select emerging bonds such as Philippine peso notes yield up to 6.2% for longer tenors. Increased central bank activity and inflation expectations are driving these attitudes, with technical models flagging a flattening Phillips Curve and alternative drivers of persistent price pressures.

Currencies and Macro Themes

The US Dollar remains robust across trade-weighted indices. EUR/USD holds at 1.1704 amid cautious European inflation prints; USD/JPY stretches to 150.34 as the BoJ maintains ultra-loose policy, and GBP/USD trades at 1.3478 in the wake of soft UK macro data. This reflects divergences seen in European and Asian central bank stances, with volatility expected in FX pairs such as GBP/JPY and EUR/CHF given stated interest rate differentials and technical chart patterns.

Commodities and Hedging Flows

Gold has soared to $3,996.80 per troy ounce, with platinum surging even further amid supply constraints, underscoring their place in hedged portfolios. Oil trades with Brent at $65.65 and WTI at $61.85, as traders watch OPEC+ quotas and mid-East developments. Agricultural commodities are mixed: corn declined to $421.09/bushel, while energy sector spot prices fluctuate as inflation and supply chain issues ripple through valuation models.

ETFs and Thematic Trends

ETFs have set the day’s tone, with technology, AI, and commodity-linked products outpacing the S&P 500 by factors of four to nine this quarter. Leveraged and sector ETFs posted monthly returns from 90% to well over 130%, particularly in semiconductors (ASML), AI (BBAI), and innovative transport (TSLA), inflating returns for aggressive traders while escalating portfolio risk. Gold ETFs further cement their status as volatility hedges, a theme highlighted by several correlation analyses and Venn diagrams from order flow models featured in Capital Market Journal.

Market Movers and Portfolio Impact

Leading equity movers include Jio Financial, Bajaj Finance, AMD (+23%), and Tesla (+2%), with sector rotation into financials, technology, and energy boosting portfolio values. Declines in Tata Motors, Infosys, and Trent Ltd weigh on retail, IT, and auto allocations. Gold and platinum miners are top commodity performers. In fixed income, order flow analysis shows institutional participants shifting toward longer durations and credit-sensitive debt, reacting to inflation expectations and central bank signals.

Implied Impact on Equity Futures and Bond Yields

Climbing 10-year Treasury yields above 4% have pressured US equity futures, particularly in growth and tech-heavy indices, as profit margins confront higher discount rates and shifting investor preferences toward yield. The opportunity cost of equities has risen, with pronounced effects in utilities, real estate, and consumer discretionary sectors. Technical chart models place the S&P 500 below its 200-day exponential moving average, signalling possible further consolidation.