Global capital markets began the week on a volatile yet adaptive note, with a blend of central bank influence, resilient risk appetite, and outstanding performance from select asset classes. The interplay among bonds, currencies, commodities, and ETFs outlines a market shaped by Federal Reserve policy, ongoing geopolitical adjustments, and shifting investor sentiment. Below, the allocations and flows of each major market segment are examined with the most up-to-date figures and analytics.

Bonds: A Resilient Rally Amid Fed Signals

U.S. Treasury yields exhibited mild stability at the start of the trading week. The benchmark 10-year note stands at 4.08%, while the 30-year bond yields 4.69%, flat to slightly lower than last week’s settlement. This stabilization follows a modest rally in longer maturities, fueled by expectations of Federal Reserve rate cuts before year-end. Investors are increasingly looking to lock in yields, anticipating a more dovish policy turn.

Futures pricing hints at a 25 basis point cut at the approaching Federal Reserve meeting, with some market participants projecting further cumulative cuts over the next few months. Investment-grade corporate bonds continue to outperform, sustaining robust demand and trading at yield spreads close to three-decade lows—a sign of investor confidence and healthy appetite for risk assets even in a potentially interest rate softening.

Currencies: Central Banks and Policy Crosswinds

The U.S. Dollar Index (DXY) remains steady at 97.70 after recent support zone retests, navigating between resistance at 98.10–98.50 and support at 97.50. Should the DXY slip below 97.70, additional declines could accelerate, undermining recent stability.

- The euro (EUR/USD) has reclaimed 1.1730 as support, aiming toward 1.1780, though any loss of support could push rates back toward 1.1645.

- The Indian rupee, buffeted by U.S. tariff threats, is kept stable near all-time lows via decisive Reserve Bank of India intervention.

- The New Zealand dollar faces further downside risks as expectations solidify around a central bank rate cut to 2.75%; swaps markets are already pricing in more aggressive moves if necessary.

Commodities: Precious Metals Outperform, Oil Retreats

Commodities present a bifurcated landscape. Gold is trading sharply higher, up more than 48% year-to-date, mirroring surging investor demand amid persistent macro uncertainty. Silver’s extraordinary 60% gain makes it the leading performing major asset, surpassing even gold’s stellar run. The oil market, conversely, has softened after OPEC+ announced a minor production increase. Crude futures are quoted at $61,70 per barrel—representing a daily rise of roughly 1%, but remaining off prior highs due to stabilization in supply expectations. Agriculture commodities are trading mixed: coffee has jumped 2.7% to 388.35 USd/Lbs, though milk, potatoes, and corn have dipped slightly, suggesting a cautious short-term demand outlook.

ETFs: Robust Flows and Continual Product Launches

The ETF market highlights the intensifying competition and innovation sweeping the investment landscape. U.S. Bitcoin ETF inflows rose to a record $7.5 billion last week, as BlackRock’s IBIT attracted $790 million—total ETF flows now account for an impressive 7% of Bitcoin’s total market capitalization. Ethereum ETF products also drew $233 million in flows, though below their recent peak. Product development continues apace, with Nasdaq launching the F/m Emerald Special Situations ETF today, and Swiss ETF trading turnover surging nearly 66% higher than last year to reach CHF 94.4 billion YTD. JPMorgan’s Flexible Income ETF trades ex-dividend today ahead of a $0.29983 per share payout later in the week. The ETF ecosystem remains vibrant, buoyed by demand for both traditional and crypto-linked products. Market participants are closely tracking central bank actions, fiscal headlines, and sector rotations that shape the intricate mosaic of global capital markets. As risk appetite remains resilient and flows continue to diversify across asset types, this morning’s data reflects an ecosystem anchored by liquidity, policy guidance, and evolving investor strategies. The interplay between defensive positioning in bonds, dynamic currency activity, runaway commodity outperformance, and rapid ETF innovation will be decisive for capital allocators in the days ahead.Here is a comprehensive capital market journal article reflecting all major asset class developments from this morning’s debrief as of October 6, 2025.

- Massively Unprofitable RCS MediaGroup Downgraded to Sell

RCS MediaGroup has presented fiscal year 2025 financials that do not withstand basic scrutiny. The company reported a collapse in gross margin from ~40% to 12.4% , an implausible 98% reduction in SG &A, and a positive net income of €54.8M that contradicts every other operational metric. Our analysis of the balance sheet, income statement, and cash flow statement reveals: We… Read more: Massively Unprofitable RCS MediaGroup Downgraded to Sell

RCS MediaGroup has presented fiscal year 2025 financials that do not withstand basic scrutiny. The company reported a collapse in gross margin from ~40% to 12.4% , an implausible 98% reduction in SG &A, and a positive net income of €54.8M that contradicts every other operational metric. Our analysis of the balance sheet, income statement, and cash flow statement reveals: We… Read more: Massively Unprofitable RCS MediaGroup Downgraded to Sell - Europe at the Crossroads: Why European passivity on Ukraine and Iran is strategically incoherent, and what a coherent Great Moderation approach looks like

Europe faces two converging geopolitical crises that its current leadership is managing as isolated, intractable problems. This analysis argues they are, in fact, structurally linked — and that a coherent dual-track strategy can resolve both simultaneously. On the eastern front, a negotiated settlement with Russia, structured around energy revenue, EU accession, and permanent NATO renunciation… Read more: Europe at the Crossroads: Why European passivity on Ukraine and Iran is strategically incoherent, and what a coherent Great Moderation approach looks like

Europe faces two converging geopolitical crises that its current leadership is managing as isolated, intractable problems. This analysis argues they are, in fact, structurally linked — and that a coherent dual-track strategy can resolve both simultaneously. On the eastern front, a negotiated settlement with Russia, structured around energy revenue, EU accession, and permanent NATO renunciation… Read more: Europe at the Crossroads: Why European passivity on Ukraine and Iran is strategically incoherent, and what a coherent Great Moderation approach looks like - CONSTITUTIONAL ASYMMETRY, ECONOMIC DEPENDENCY,AND THE CASE FOR NATIONAL SELF-DETERMINATION

Wales, Scotland, and Northern Ireland in Historical,Sociological and Economic Perspective This paper examines the structural, historical, and economic contradictions inherent in the United Kingdom’s constitutional settlement as it pertains to Wales, Scotland, and Northern Ireland. Drawing on political theory, economic data, historical sociology, and comparative constitutional studies, it argues that the current devolution framework, while… Read more: CONSTITUTIONAL ASYMMETRY, ECONOMIC DEPENDENCY,AND THE CASE FOR NATIONAL SELF-DETERMINATION

Wales, Scotland, and Northern Ireland in Historical,Sociological and Economic Perspective This paper examines the structural, historical, and economic contradictions inherent in the United Kingdom’s constitutional settlement as it pertains to Wales, Scotland, and Northern Ireland. Drawing on political theory, economic data, historical sociology, and comparative constitutional studies, it argues that the current devolution framework, while… Read more: CONSTITUTIONAL ASYMMETRY, ECONOMIC DEPENDENCY,AND THE CASE FOR NATIONAL SELF-DETERMINATION - The Necessity of a United Nations HQ Relocation to the Hague with a Permanent Nuremberg Tribunal.The Impunity Crisis of Rogue Governments

The world witnesses today an unprecedented crisis of accountability in international law. As the genocide in Gaza unfolds before global eyes, as war crimes multiply across Ukraine, Myanmar, and countless other conflicts, the United Nations stands paralysed, not by lack of legal framework, but by institutional capture that protects the very criminals it should prosecute.… Read more: The Necessity of a United Nations HQ Relocation to the Hague with a Permanent Nuremberg Tribunal.The Impunity Crisis of Rogue Governments

The world witnesses today an unprecedented crisis of accountability in international law. As the genocide in Gaza unfolds before global eyes, as war crimes multiply across Ukraine, Myanmar, and countless other conflicts, the United Nations stands paralysed, not by lack of legal framework, but by institutional capture that protects the very criminals it should prosecute.… Read more: The Necessity of a United Nations HQ Relocation to the Hague with a Permanent Nuremberg Tribunal.The Impunity Crisis of Rogue Governments - The Digital Job Posting Bubble: Quantifying Phantom Demand in Online Labor Markets

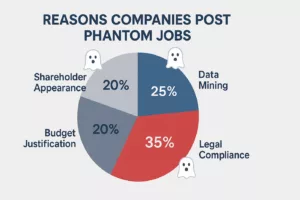

Are businesses and corporates truly hiring ? Has the digital economy become a massive convenience mystification of actual economic activities? How large, systemic and unstable is the assets bubble built by Wall Street financial engineering and gambling addiction? What are the empirical evidence of structural distortions in digital labor markets that represent a significant and… Read more: The Digital Job Posting Bubble: Quantifying Phantom Demand in Online Labor Markets

Are businesses and corporates truly hiring ? Has the digital economy become a massive convenience mystification of actual economic activities? How large, systemic and unstable is the assets bubble built by Wall Street financial engineering and gambling addiction? What are the empirical evidence of structural distortions in digital labor markets that represent a significant and… Read more: The Digital Job Posting Bubble: Quantifying Phantom Demand in Online Labor Markets