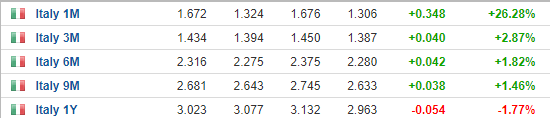

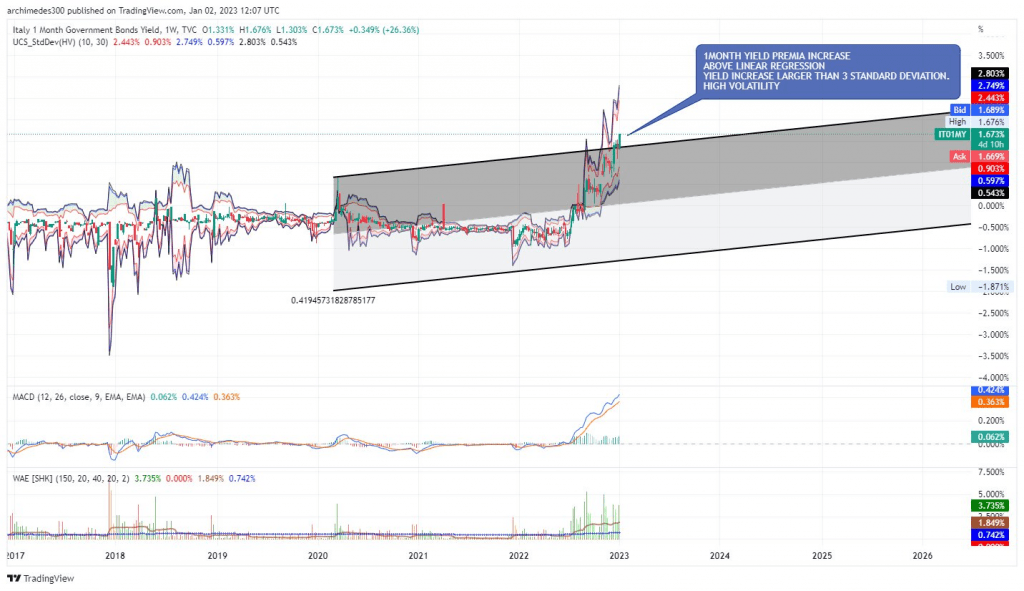

Observing high volatility in the 1-Month CTZ Italian debt yield. There’s a 348 basis point increase intraday. the yield jumped +26.28%. The chart below explains how the 1Month CTZ Yield has increased outside 3 standard deviations from the linear regression average yield. Yield historical patterns of volatility could eventually see the 1-MonthCTZ Yield increase even further to 2.4% / 2.79%.

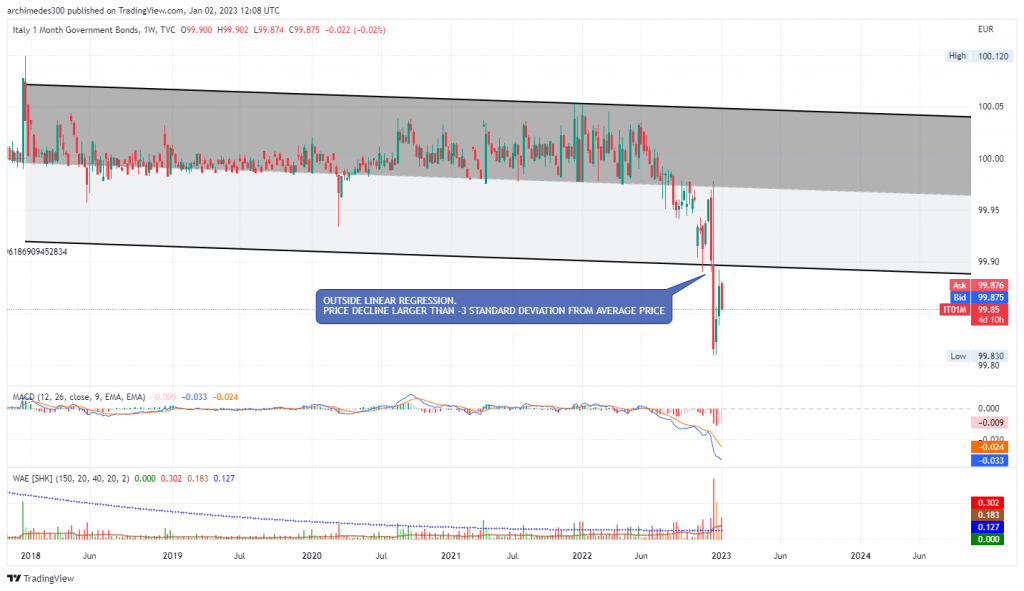

Also, the price of the 1-Month CTZ short terms debt has declined far outside the 3 standard deviations linear regression. Intraday above-average volumes.

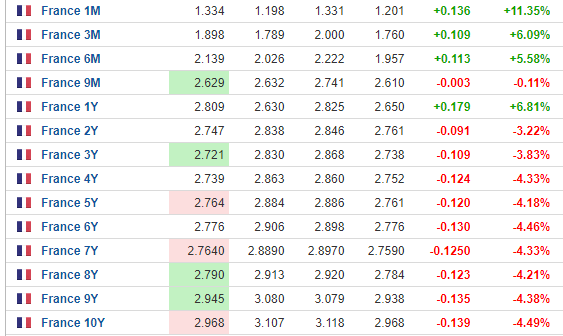

Similar volatility can be observed also for the French Sovereign debt yield curve. The 1-month debt yield has increased by 136 basis points. The 3-month debt yield 109 basis points, 6-month 113 basis points, while the 1Y OAT yield has jumped 179 basis points 2.80% curve inversion.