CIR interest rate forecast model

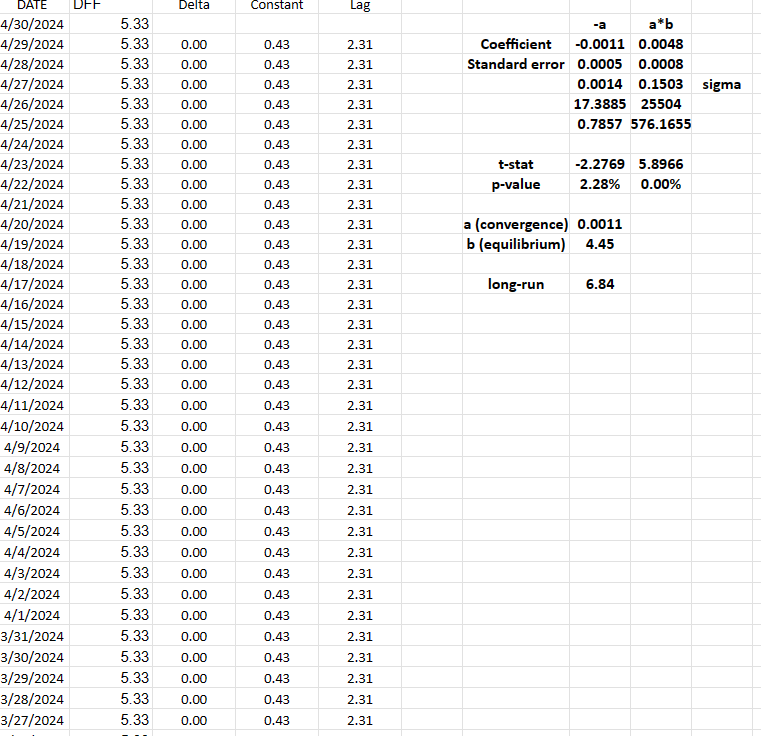

Cox Ingersoll Ross model to forecast interest rate variables in simple terms defines an Effective Federal Fund rate equilibrium of 4.45%, but with a forecast of a higher long-run Federal Fund Rate of 6.84% that could imply a slight possibility of further Federal Reserve hikes of Federal Fund rate. The interesting data becomes the equilibrium interest rate of 4.45% higher than the presumed R* of 2.0% | 2.5% range. Indeed, the statistical inference with a p-value close to 0% indicates statistical significance, considering a basic interest rate forecast elaboration.

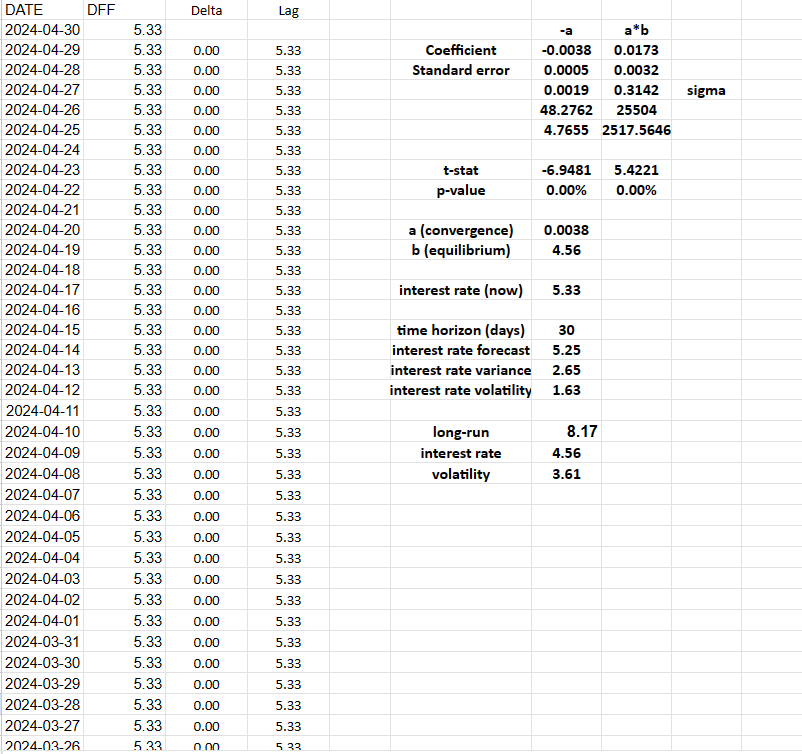

Another Interest rate forecast model of long-run equilibrium and interest rate volatility has been elaborated by applying the Vasicek model, which also results in statistical significance with p-values at 0%. The equilibrium interest rate result is almost similar at EFFR 4.56%, with a 30-day time horizon forecast of 5.2%, basically unchanged from current levels, however, the long-run Federal Fund Rate forecast results in a much higher EFFR of 8.15%. Both interest rate volatility models hint at the possibility of a higher Federal Fund Rate that could occur on the basis of Inflationary shocks, based on large energy supply and prices shock, with the de-anchoring of inflation expectations.