European financial markets have experienced a notable rally in 2025, but beneath the surface, nuanced trends, pockets of stress, and sector-specific drivers demand close analysis. This comprehensive article synthesises overnight developments, sector momentum, credit market signals, risks, and recent equity and CDS spread dynamics, providing a detailed briefing for global investors with a focus on the European market environment.

Market Overview: Rally, Resilience, and Sector Leaders

European equity benchmarks like the STOXX Europe 600 and the Euro STOXX 50 entered October demonstrating cautious stability. Indices hovered near record or multi-year highs, reflecting optimism fueled by robust corporate earnings, steady economic activity, and anticipation of central bank policy support.

The current rally is broadening but selective, with sector winners emerging:

- Automotive: Benefiting from continued demand for high-end and electric vehicles, exemplified by strong moves in BMW.

- Insurance: Münchener Rückversicherungs-Gesellschaft and Allianz outperformed as investors sought defensive characteristics.

- Pharmaceuticals: Sanofi and others drew capital flows amid ongoing healthcare innovation and global demographic trends.

- Luxury Goods: LVMH led gains, highlighting the ongoing strength of discretionary consumer spending in premium brands.

- Industrials: Siemens and Airbus delivered gains, fueled by rising investment in manufacturing, infrastructure, and defence.

What’s Driving the Rally: Structural and Policy Supports

- Government Spending and Defence: Heightened announcements on EU defence funding and fiscal stimulus, particularly in Germany, galvanised the industrials and defence stocks. Aerospace and military sector companies like Rheinmetall and Leonardo saw significant outperformance.

- Healthcare Innovation: Uncertainty resolution around international drug pricing, coupled with ageing societies and resilient R&D pipelines, spurred interest in pharmaceutical and healthcare equities.

- Commodity Upside: Mining stocks (especially in gold and uranium) benefited from strong commodity price rallies, with gold miners advancing as spot prices soared over 45% this year.

- Accommodative Monetary Policy: Investor optimism is shored up by expectations of rate cuts from the US Federal Reserve and a supportive stance from the European Central Bank. Easier policy regimes are lowering the cost of capital and encouraging risk-taking.

- European Sovereignty Investments: Policy initiatives are targeting long-term strategic priorities in defence, cybersecurity, energy transition, and green technologies, channelling capital to these sectors.

Credit Markets: Stress Signals and CDS Spreads

- Widening Credit Spreads: Investment-grade corporate bond spreads versus government benchmarks have shown signs of widening, reflecting increased risk aversion. This repricing is particularly visible for banks and corporates with weaker balance sheets or greater exposure to global market disruptions.

- Liquidity Fluctuations: Recent episodes—such as the rapid sell-off in US Treasuries—revealed underlying fragilities as leveraged market participants repositioned. These moves can tighten funding and increase credit risk premiums, hitting banks’ funding profiles.

- Private Debt Fragility: The private credit market, now a substantial lender to European corporates, shows rising stress: interest coverage ratios have halved since 2021, and almost half of borrowers report liquidity strain. This is resulting in more “Payment-in-Kind” lending and a higher risk of defaults.

The European banks that showed the largest CDS widening this month include

- Credit Agricole: CDS spreads widened by about 31.7%

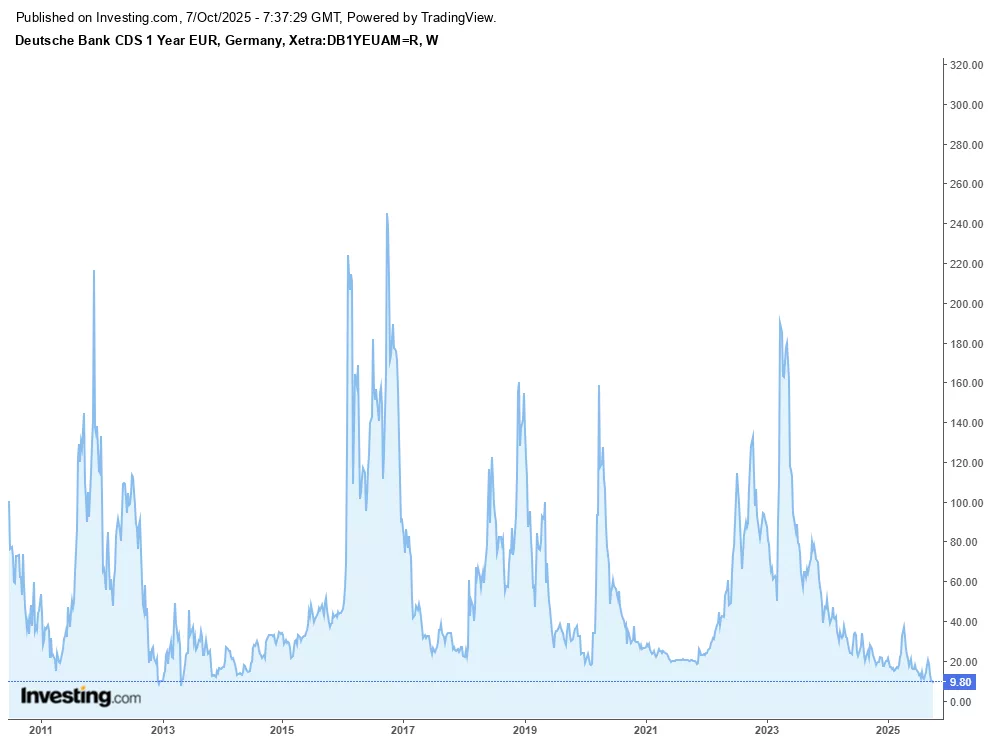

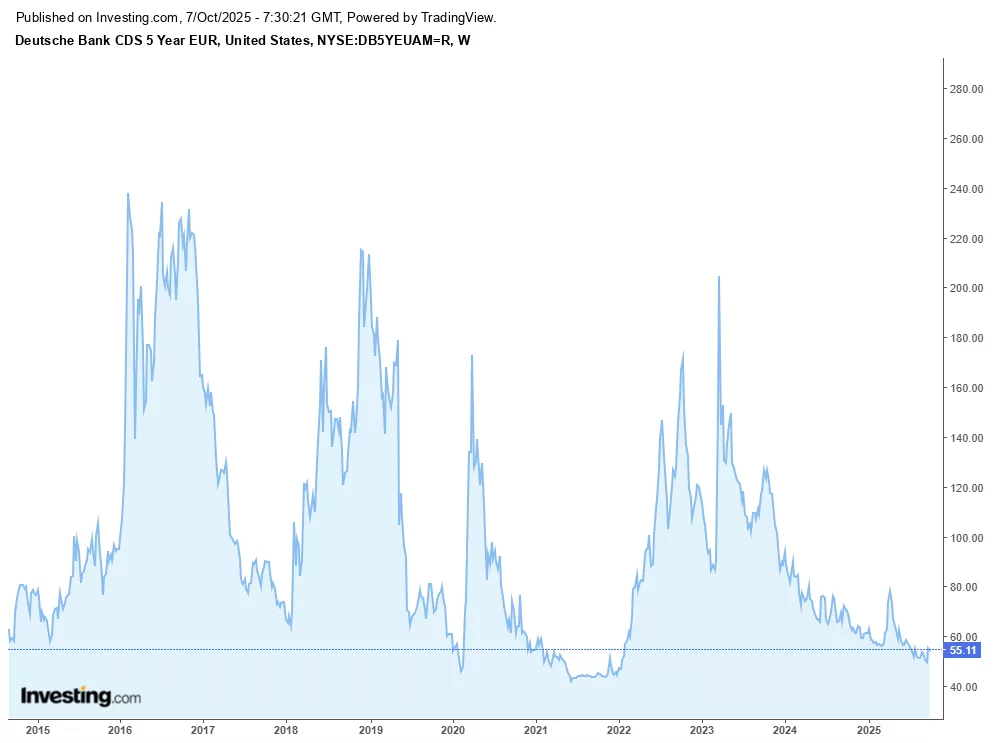

- Deutsche Bank: CDS spreads widened by about 31.3%

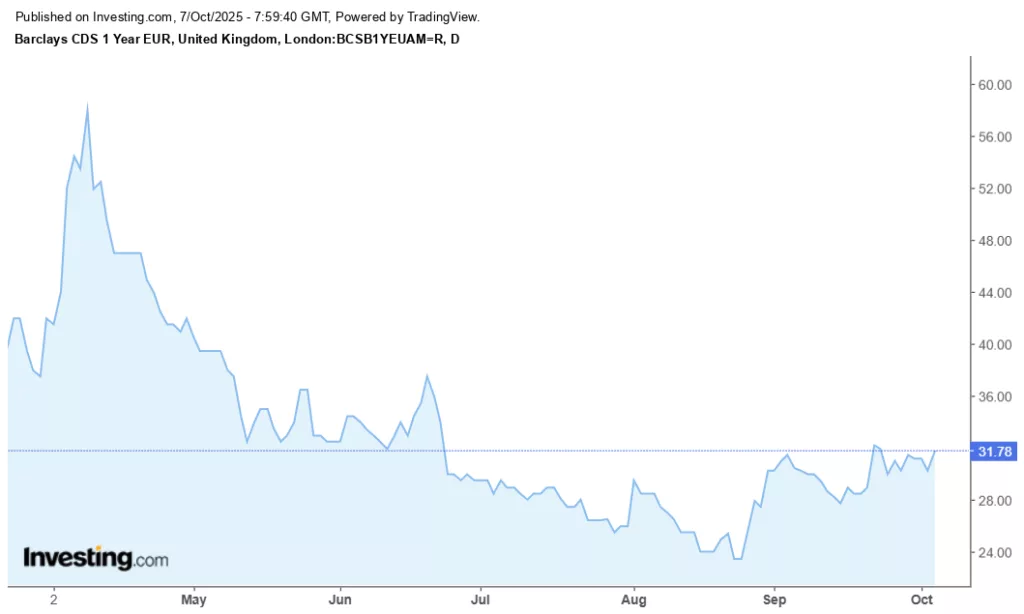

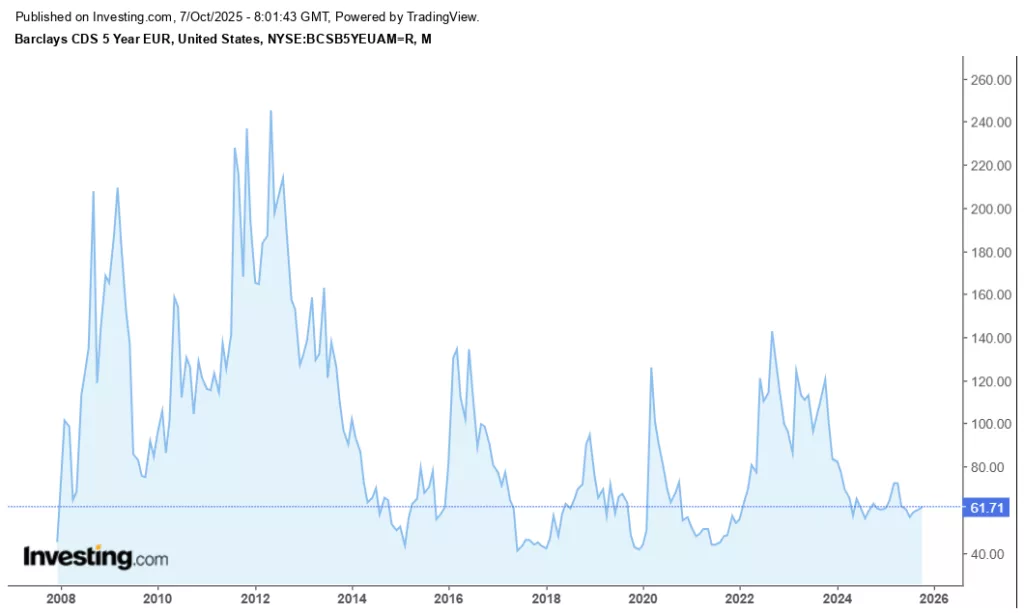

- Barclays: five-year CDS widened around 38 basis points from earlier lows this year

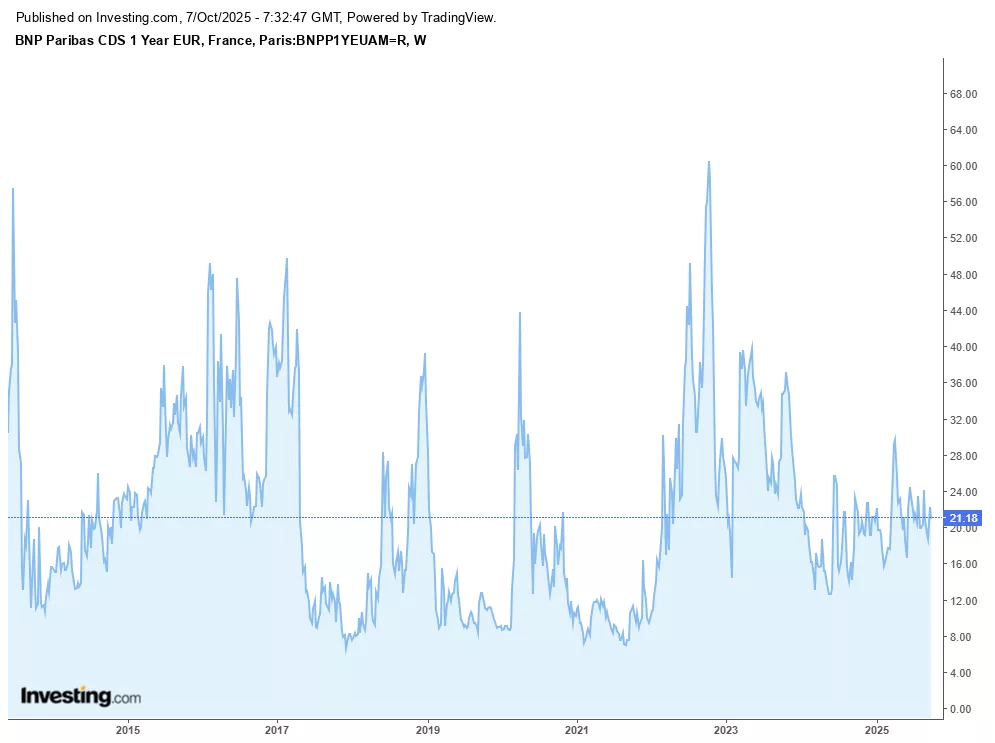

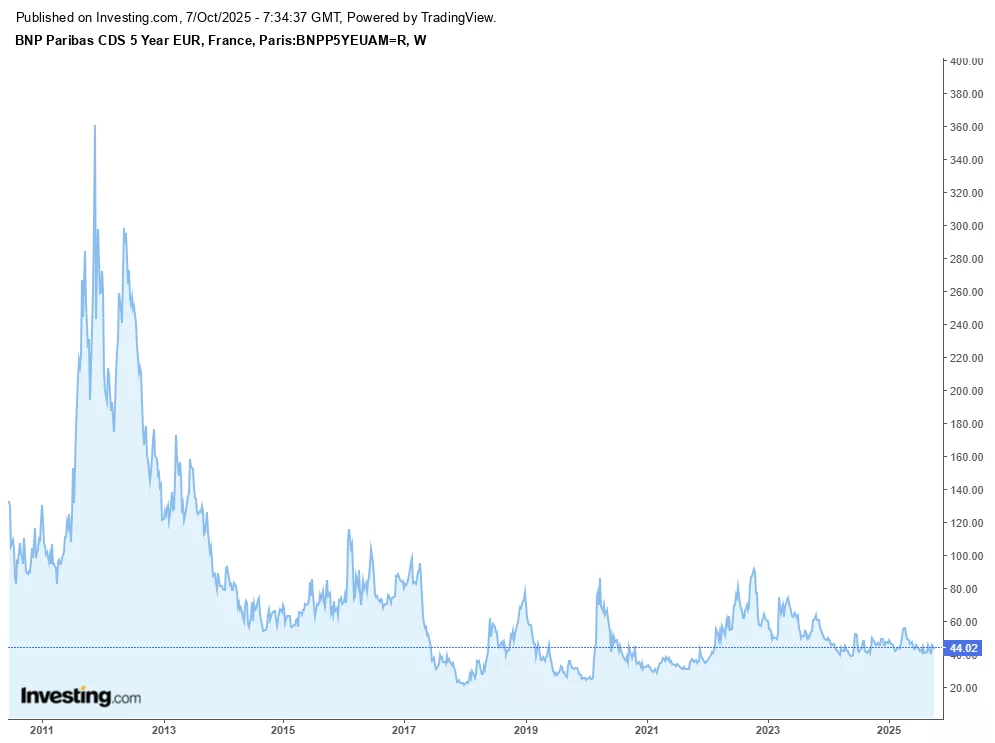

- BNP Paribas: five-year CDS widened by around 40 basis points

While these moves are significant, the overall CDS market behaviour for European banks remains orderly without clear “weak links,” and some banks have even outperformed US peers during recent market stress. The broad average CDS widening for a basket of nine French and German banks tracked was about 19%, reflecting material but contained credit risk concerns. Credit Agricole, Deutsche Bank, Barclays, and BNP Paribas have experienced the most notable CDS spread widening this month among European banks, signalling increased perceived credit risk but not yet systemic distress.

Credit Agricòle 1Y and 5Y CDS

BNP PARIBAS 1Y AND 5Y CDS

Deutsche Bank 1Y and 5Y CDS

Barclays Plc 1Y and 5Y CDS

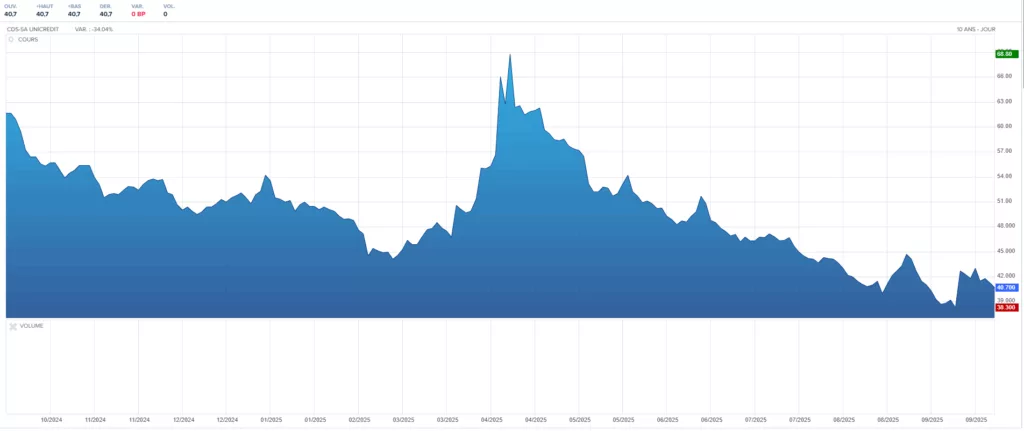

Unicredit Bank 5y CDS

CDS Trends and Threshold Breaches

Threshold Breaches: Among those, Raiffeisen Bank International (RBI) stands out as its 5-year CDS breached the 192.5 bps mark, well into elevated risk territory. Hamburg Commercial Bank (HCOB) and UniCredit also showed persistent upwards pressure on CDS, while Deutsche Bank and Commerzbank edged higher but remain below acute distress levels.

General Picture: Most major European banks saw CDS spreads narrow earlier in the year but experienced episodic widening during bouts of market turmoil, such as in April 2025’s tariff sell-off. Current levels remain elevated above pre-2024, with notable volatility tied to macro-economic uncertainty, regulatory actions, and geopolitical risk.

Banks with Notable CDS Widening: This month, Credit Agricole, Deutsche Bank, Barclays, and BNP Paribas saw the largest CDS spread increases among their peers, with five-year CDS spreads expanding by as much as 40 basis points. The broad average for a key basket of French and German banks saw a 19% spike in credit risk pricing.

| Bank | 5-Year CDS Spread (bps) | Risk Drivers |

|---|---|---|

| Raiffeisen Bank Int. | ~192.5 | Russian exposure, divestiture plans |

| Hamburg Commercial | Elevated | Legal, asset-based lending risks |

| UniCredit | High & volatile | Credit/economic risk |

| Deutsche Bank | Moderately higher | Macro/geopolitical risk |

| Commerzbank | Moderately higher | Market caution |

Equity Moves: Impact of Credit Signals

This indicates differentiated risk profiles, with some banks showing clear signs of elevated credit stress while others remain more stable. Recent key European banks breaching CDS spread risk thresholds include:

- Raiffeisen Bank International (RBI) has 5-year CDS spreads near 192.5 basis points, impacted by its Russian exposure and divestiture uncertainties.

- Hamburg Commercial Bank (HCOB) with elevated CDS spreads signalling investor caution due to legal risks and asset-based lending exposures.

- UniCredit is showing relatively high and volatile CDS spreads, indicating increased perceived credit risk.

- Deutsche Bank and Commerzbank have seen moderate CDS spread widening, reflecting market caution amid geopolitical and economic uncertainties.

- More stable banks include Bayern LB, LBBW, and Helaba, which show significantly lower CDS spreads and stronger credit ratings.

CDS spreads above 150-200 bps for these banks mark elevated credit risk and potential downgrade concerns, highlighting varying risk levels within the European banking sector.

Key Risks That Could Challenge the Rally

- Inflation and Input Costs: Renewed cost pressures, especially related to energy and raw materials, could pinch margins for both sectors.

- Geopolitical/Trade Shocks: New rounds of trade wars, sanctions, or escalations in conflicts can disrupt supply chains, slash demand, and spike volatility.

- Economic Slowdown or Recession: Any pronounced weakening in European or global growth would immediately weigh on cyclicals, banks, and industrials.

- Credit and Debt Market Stress: Surging defaults within the shadow banking sector or a broader credit squeeze would prompt banks to tighten lending, further pressuring risk assets.

- Regulatory and Policy Changes: Unanticipated fiscal tightening, regulatory reforms, or tax increases could suppress profitability and dampen investor sentiment.

- Market Sentiment Shifts: Overvaluation and concentration risk (where rallies hinge on a handful of sectors or names) leave markets vulnerable to sharp corrections.

Actionable Insights for Investors

- Monitor Sector Rotation: The leadership of industrials, pharmaceuticals, financials, and luxury may persist but is sensitive to global growth and policy signals. Active sector rotation may uncover tactical alpha opportunities as conditions evolve.

- Watch CDS and Credit Spreads: Widening CDS is often an early warning for equity underperformance in banks and corporates with stretched balance sheets. Persistent breaches of risk thresholds signal a need for nimble risk management.

- Global Crosscurrents: Stay attentive to macro themes—rate cuts, currency volatility, and political risks—which drive capital flows into and out of key market segments.

- Private Credit Strain: Be cautious with private credit lenders and borrowers showing deteriorating coverage metrics, as liquidity strains may not be fully priced into market valuations.

- Defensive Diversification: Exposure to sectors and geographies demonstrating structural resilience and defensive qualities can help buffer periods of heightened volatility.

While European shares and select sectors continue to attract global capital, vigilance for credit market risk, close tracking of CDS spreads, and a nuanced approach to sector positioning are essential. Market resilience coexists with stress pockets, and successful investors will blend tactical awareness with longer-term macro and policy foresight in navigating the evolving European landscape

- Massively Unprofitable RCS MediaGroup Downgraded to Sell

RCS MediaGroup has presented fiscal year 2025 financials that do not withstand basic scrutiny. The company reported a collapse in gross margin from ~40% to 12.4% , an implausible 98% reduction in SG &A, and a positive net income of €54.8M that contradicts every other operational metric. Our analysis of the balance sheet, income statement, and cash flow statement reveals: We… Read more: Massively Unprofitable RCS MediaGroup Downgraded to Sell

RCS MediaGroup has presented fiscal year 2025 financials that do not withstand basic scrutiny. The company reported a collapse in gross margin from ~40% to 12.4% , an implausible 98% reduction in SG &A, and a positive net income of €54.8M that contradicts every other operational metric. Our analysis of the balance sheet, income statement, and cash flow statement reveals: We… Read more: Massively Unprofitable RCS MediaGroup Downgraded to Sell - Europe at the Crossroads: Why European passivity on Ukraine and Iran is strategically incoherent, and what a coherent Great Moderation approach looks like

Europe faces two converging geopolitical crises that its current leadership is managing as isolated, intractable problems. This analysis argues they are, in fact, structurally linked — and that a coherent dual-track strategy can resolve both simultaneously. On the eastern front, a negotiated settlement with Russia, structured around energy revenue, EU accession, and permanent NATO renunciation… Read more: Europe at the Crossroads: Why European passivity on Ukraine and Iran is strategically incoherent, and what a coherent Great Moderation approach looks like

Europe faces two converging geopolitical crises that its current leadership is managing as isolated, intractable problems. This analysis argues they are, in fact, structurally linked — and that a coherent dual-track strategy can resolve both simultaneously. On the eastern front, a negotiated settlement with Russia, structured around energy revenue, EU accession, and permanent NATO renunciation… Read more: Europe at the Crossroads: Why European passivity on Ukraine and Iran is strategically incoherent, and what a coherent Great Moderation approach looks like - CONSTITUTIONAL ASYMMETRY, ECONOMIC DEPENDENCY,AND THE CASE FOR NATIONAL SELF-DETERMINATION

Wales, Scotland, and Northern Ireland in Historical,Sociological and Economic Perspective This paper examines the structural, historical, and economic contradictions inherent in the United Kingdom’s constitutional settlement as it pertains to Wales, Scotland, and Northern Ireland. Drawing on political theory, economic data, historical sociology, and comparative constitutional studies, it argues that the current devolution framework, while… Read more: CONSTITUTIONAL ASYMMETRY, ECONOMIC DEPENDENCY,AND THE CASE FOR NATIONAL SELF-DETERMINATION

Wales, Scotland, and Northern Ireland in Historical,Sociological and Economic Perspective This paper examines the structural, historical, and economic contradictions inherent in the United Kingdom’s constitutional settlement as it pertains to Wales, Scotland, and Northern Ireland. Drawing on political theory, economic data, historical sociology, and comparative constitutional studies, it argues that the current devolution framework, while… Read more: CONSTITUTIONAL ASYMMETRY, ECONOMIC DEPENDENCY,AND THE CASE FOR NATIONAL SELF-DETERMINATION - The Necessity of a United Nations HQ Relocation to the Hague with a Permanent Nuremberg Tribunal.The Impunity Crisis of Rogue Governments

The world witnesses today an unprecedented crisis of accountability in international law. As the genocide in Gaza unfolds before global eyes, as war crimes multiply across Ukraine, Myanmar, and countless other conflicts, the United Nations stands paralysed, not by lack of legal framework, but by institutional capture that protects the very criminals it should prosecute.… Read more: The Necessity of a United Nations HQ Relocation to the Hague with a Permanent Nuremberg Tribunal.The Impunity Crisis of Rogue Governments

The world witnesses today an unprecedented crisis of accountability in international law. As the genocide in Gaza unfolds before global eyes, as war crimes multiply across Ukraine, Myanmar, and countless other conflicts, the United Nations stands paralysed, not by lack of legal framework, but by institutional capture that protects the very criminals it should prosecute.… Read more: The Necessity of a United Nations HQ Relocation to the Hague with a Permanent Nuremberg Tribunal.The Impunity Crisis of Rogue Governments - The Digital Job Posting Bubble: Quantifying Phantom Demand in Online Labor Markets

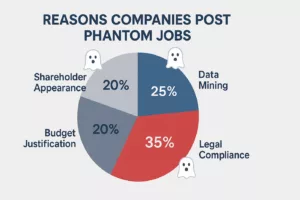

Are businesses and corporates truly hiring ? Has the digital economy become a massive convenience mystification of actual economic activities? How large, systemic and unstable is the assets bubble built by Wall Street financial engineering and gambling addiction? What are the empirical evidence of structural distortions in digital labor markets that represent a significant and… Read more: The Digital Job Posting Bubble: Quantifying Phantom Demand in Online Labor Markets

Are businesses and corporates truly hiring ? Has the digital economy become a massive convenience mystification of actual economic activities? How large, systemic and unstable is the assets bubble built by Wall Street financial engineering and gambling addiction? What are the empirical evidence of structural distortions in digital labor markets that represent a significant and… Read more: The Digital Job Posting Bubble: Quantifying Phantom Demand in Online Labor Markets