Asian markets opened mixed on Tuesday as investors digested a flurry of economic data from across the region, with tech optimism from Wall Street providing some support while various indicators painted a nuanced picture of economic health across the Asia-Pacific. Asian-Pacific markets were set to open mostly higher Tuesday, tracking Wall Street gains on a tech rally fueled by the massive deal between OpenAI and AMD, in one of the most direct challenges to Nvidia’s dominance in the AI chip space. This technological optimism helped offset concerns raised by some of the weaker economic data points released overnight.

Indonesia: Consumer Spending Shows Resilience

Indonesia’s motorbike sales climbed 7.3% year-on-year to 567,173 units in September 2025, following a 0.7% rise in August. This marked the second straight month of annual increase, following a 150 basis points interest rate cut by the central bank since last September. The motorbike industry is often seen as a proxy for consumer confidence in Southeast Asia’s largest economy.

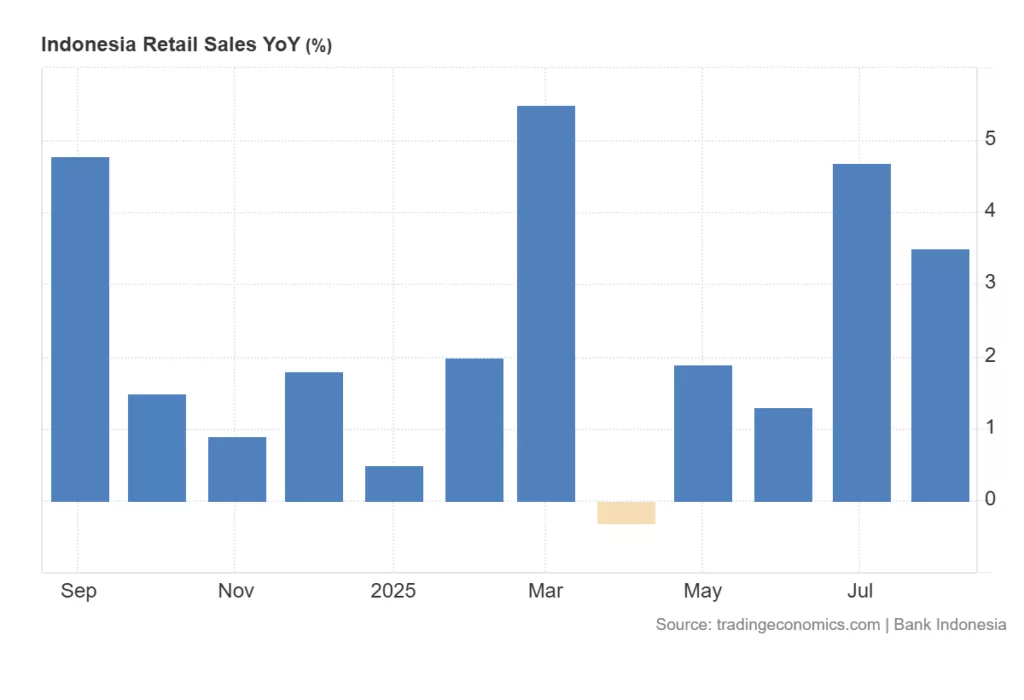

However, Indonesia’s retail sales growth eased to 3.5% year-on-year in August, down from 4.7% in the previous month and below expectations of 3.9%. This marked the fourth consecutive month of annual growth, though at a softer pace, supported by ongoing government stimulus measures aimed at maintaining household purchasing power.

Japan: Foreign Investment Flows Shift Dramatically

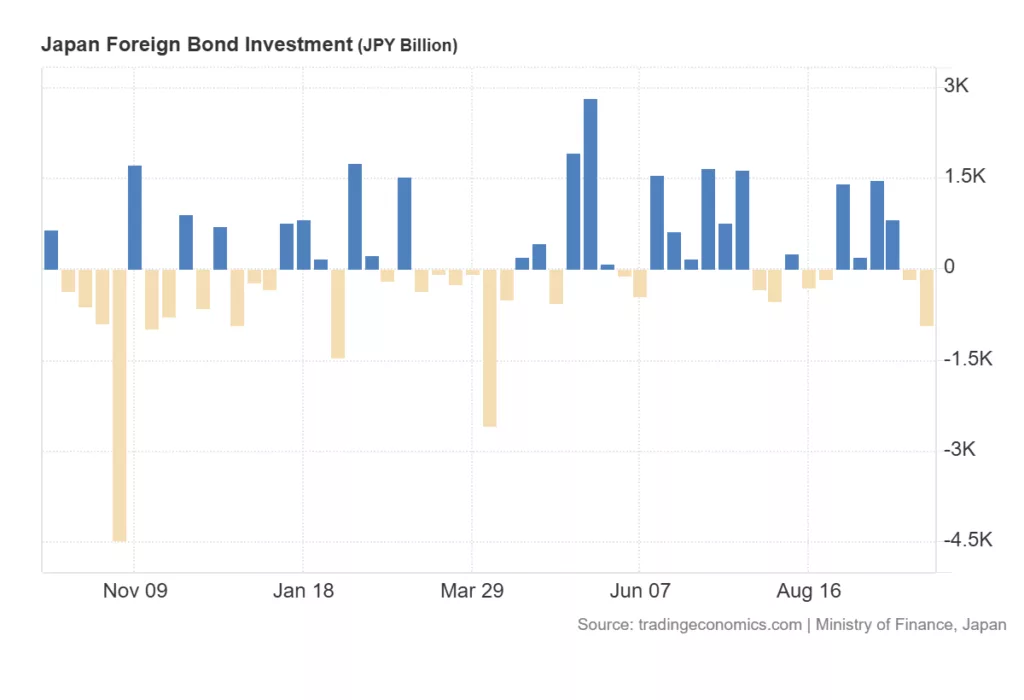

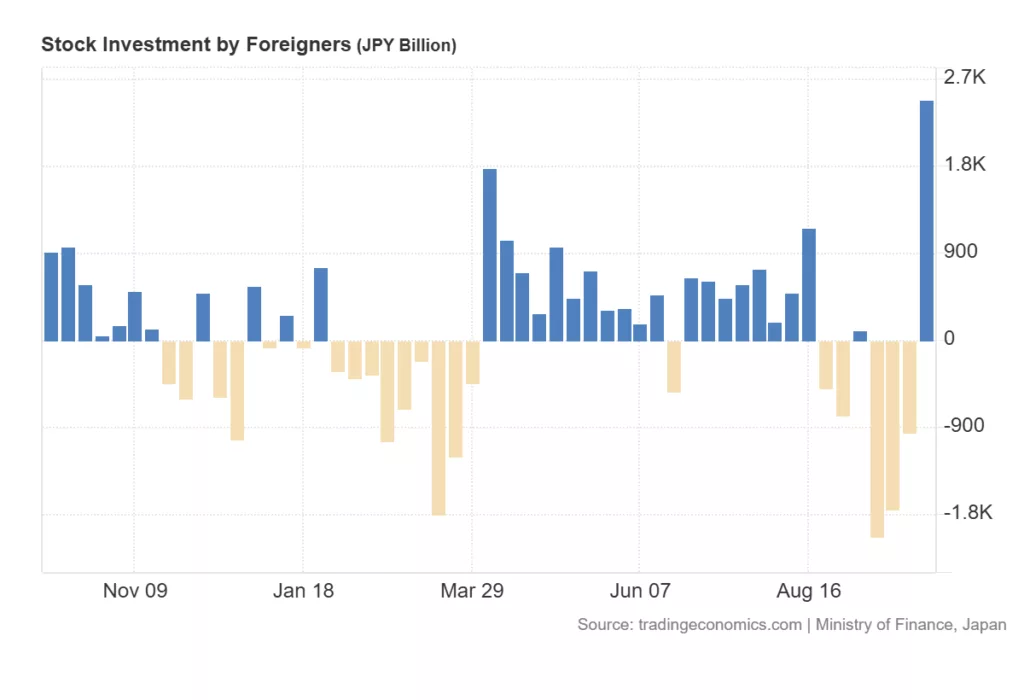

Japan experienced significant foreign investment activity with foreign investment in Japanese stocks increasing dramatically to ¥2,479.9 billion in early October from a previous ¥-963.3 billion. This marked a remarkable turnaround and signalled renewed confidence in Japan’s market. In contrast, foreign bond investment showed a different picture with Japanese investors selling ¥926.6 billion worth of foreign bonds, reversing from the ¥158.7 billion purchase in the previous period. The bond market showed shifting expectations about Japanese monetary policy:

- 5-Year JGB Auction yields rose to 1.233% from 1.119%

- 6-Month Bill Auction yields increased to 0.5933% from 0.5135%

Machine tool orders, a key indicator of capital spending, surged 9.9% year-on-year in September, beating expectations of 8.1% and accelerating from 8.5% in August, suggesting continued investment in the manufacturing sector.

Australia: Inflation Expectations Rise

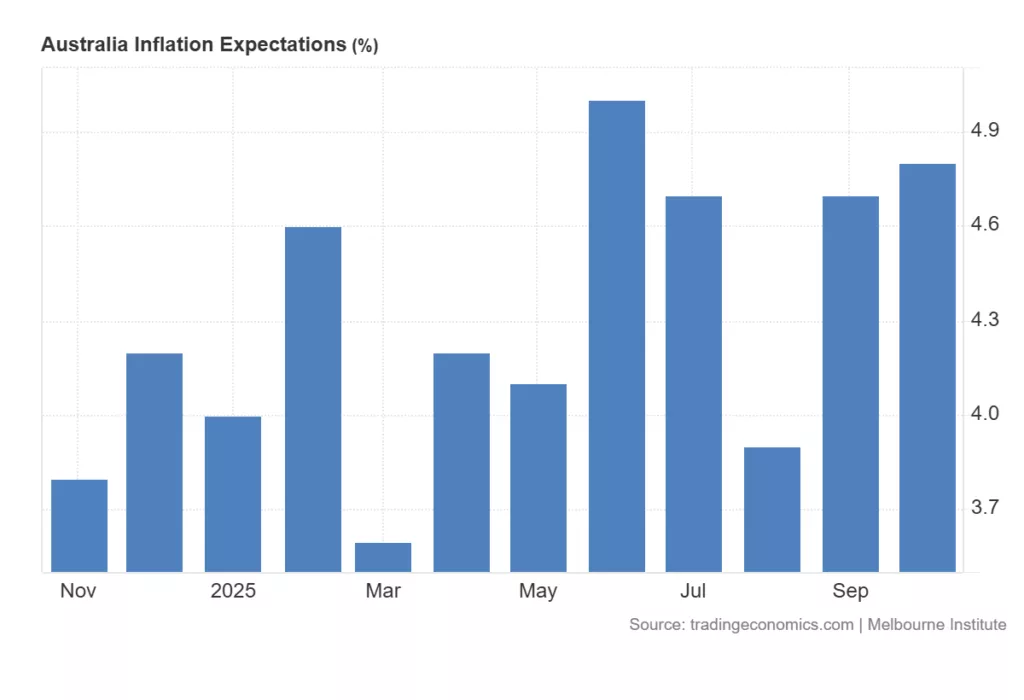

Consumer inflation expectations in Australia edged up to 4.8% in October from 4.7% in the previous month, marking the highest reading since June. The increase suggests mounting concerns that Q3 inflation may exceed forecasts, potentially influencing Reserve Bank of Australia policy decisions. Australian Inflation Expectations have been consistently above 4% for all of 2025, while the Reserve Bank of Australia has tried to slightly decrease the RBA cash rate to 3.6%. The current borrowing cost discounted for Inflation is negative, in that sense risking another Inflationary wave for Australian consumers, who have been dealing with high consumer prices and diminishing purchasing power. In this instance, it would be reasonable to expect the Reserve Bank of Australia to carefully evaluate the Inflation picture and price stability in Australia for Australian consumers going forward.

Singapore: Stable Short-Term Rates

Singapore’s 6-month T-bill cut-off yield stayed flat at 1.44%, unchanged from the previous auction. This stability suggests the Monetary Authority of Singapore is maintaining its current policy stance amid global economic uncertainty.

European Data Impacts Asian Sentiment

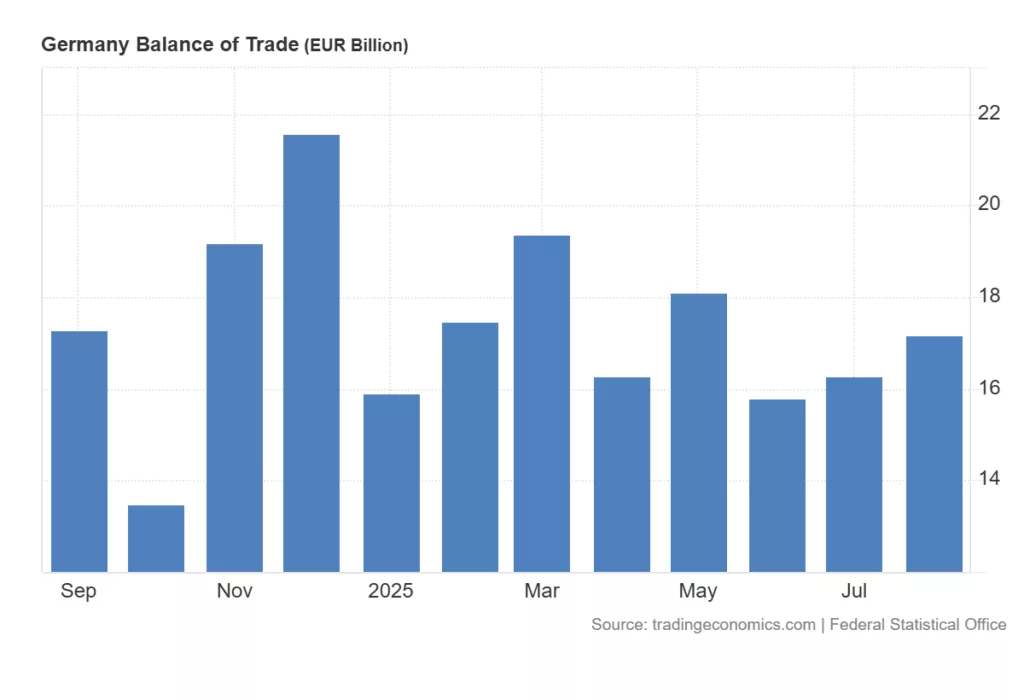

Germany’s trade surplus widened to €17.2 billion in August, up from an upwardly revised €16.3 billion in July and surpassing expectations of €15.2 billion. This marked the largest trade surplus since May as exports fell less than imports. However, the detailed breakdown showed some weakness: Exports MoM: -0.5% (vs. -0.2% forecast), Imports MoM: -1.3% (vs. -0.7% forecast)

Market Implications

The mixed data from Asian markets reflects the complex global economic landscape with varying regional performances. While tech optimism drives market sentiment, traditional economic indicators show diverging trends across countries. For investors, these developments suggest:

- Continued opportunities in AI-related investments across Asian markets

- Interest rate sensitivity in Japanese markets as yields rise

- Consumer resilience in Indonesia despite slowing retail growth

- Trade strength in Germany supports European market stability.

Market participants should watch for further developments in AI partnerships, central bank policies, and trade data for additional direction on regional market trends. The interplay between technological innovation and traditional economic indicators will likely shape market movements in the coming sessions. As one analyst noted, “Asian markets continue to balance global tech enthusiasm with regional economic realities. The divergent data points suggest investors need to maintain a selective approach, focusing on specific opportunities rather than broad market trends