The global financial system is currently navigating a complex and precarious situation marked by high hedge fund leverage, substantial exposure of major banks, and significant unrealized losses on balance sheets. These factors are intertwined to create a landscape of heightened financial risk, raising concerns about the stability of the entire financial system and the limitations of central banks in addressing potential crises.

Hedge Fund Leverage and Its Impact

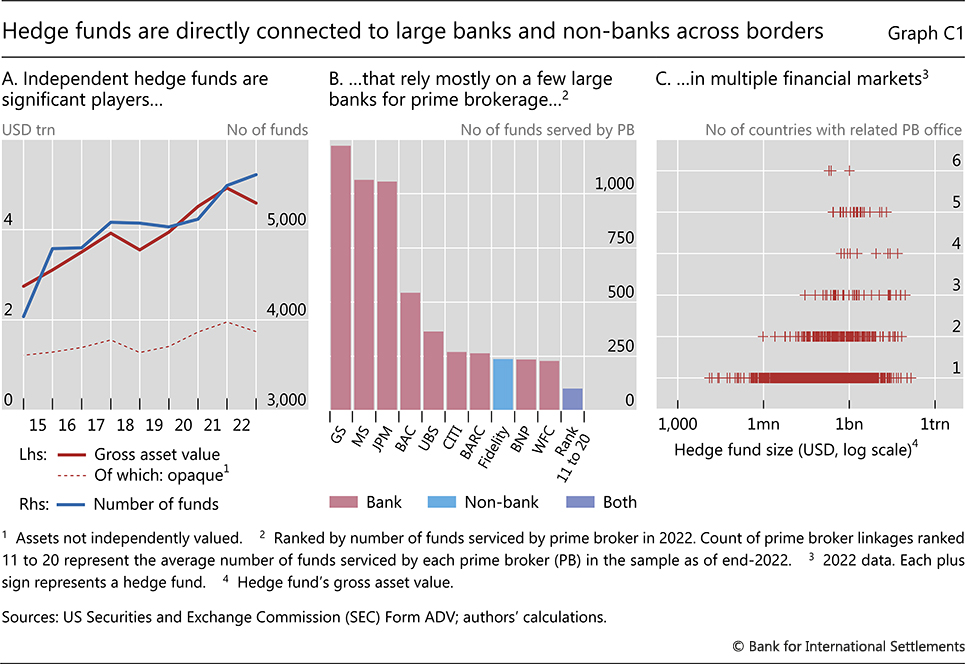

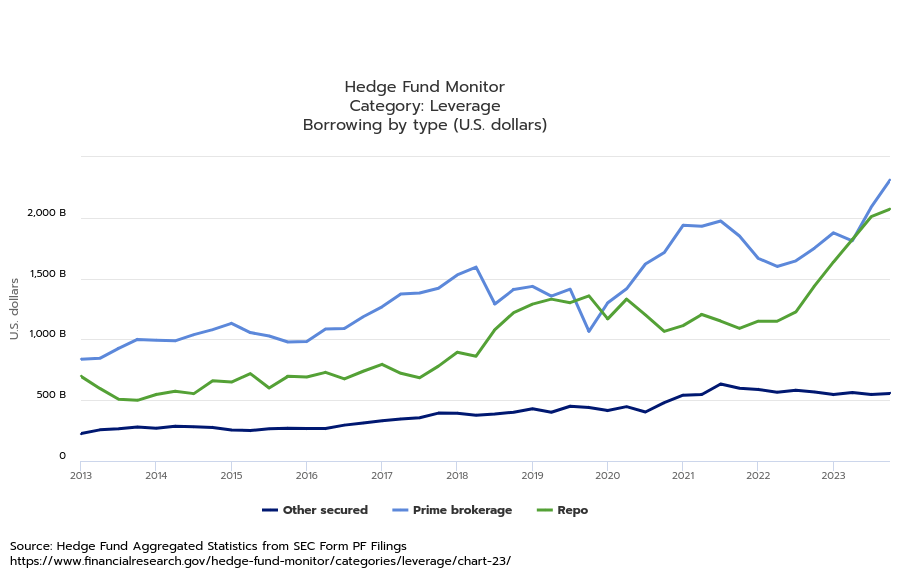

Hedge funds, known for their aggressive and often highly speculative investment strategies, have leveraged their portfolios to extraordinary levels in recent years. Hedge fund leverage has surged to an unprecedented $28 trillion, marking a significant risk factor within the financial system. This massive leverage is fueled by various financial instruments such as Treasuries collateralised margin loans, swaps, and complex derivatives, allowing hedge funds to amplify their positions far beyond their actual capital base. By borrowing heavily against their assets, these funds aim to maximize returns, but this approach inherently magnifies potential losses, making them vulnerable to rapid market changes and volatility spikes. In particular, Treasuries collateralised margin loans and REPO market leverage are a primary source of leverage for hedge funds, where they borrow against the value of their investments to purchase more assets. This “leveraging up” multiplies the exposure of these funds to market movements, both in terms of potential gains and losses. As of March 31, 2024, the combined outstanding loans of the three largest U.S. banks—Goldman Sachs, JPMorgan Chase, and Morgan Stanley—totalled $1.832 trillion to large hedge funds. This level of exposure underscores the high risk of interconnectedness between the banking sector and hedge funds. A significant downturn in the markets or a spike in volatility could lead to substantial financial distress for both hedge funds and the banks that have extended credit to them.

The impact on major banks, which provide much of the credit to these hedge funds, is considerable. As of March 31, three of the largest banks—Goldman Sachs, JPMorgan Chase, and Morgan Stanley—had outstanding loans totalling $1.832 trillion to large hedge funds. This substantial credit exposure represents a significant portion of their lending activities and underscores the interconnectedness between hedge funds and the banking sector. The large scale of these loans highlights the risk inherent in the financial system. Whenever hedge funds experience significant losses and are poised to experience huge losses and unwinding of financial leverage, the banks that have extended credit to them may face financial strain. This interconnectedness creates a potential for cascading effects, where financial difficulties in one sector could ripple through the broader financial system, affecting other institutions and market stability. The risk of a volatility shock, akin to those experienced during market crashes such as in 2008 and March 2020, is ever-present. Historical data shows that during periods of financial turmoil, leveraged institutions, particularly hedge funds, often face rapid liquidation of positions. For instance, during the March 2020 market crash, hedge funds saw a sudden unwinding of leveraged positions, triggering forced sales of assets and exacerbating the downward spiral in asset prices. Should another significant volatility event occur, losses among hedge funds could be catastrophic, potentially leading to massive margin calls that force them to liquidate their positions at fire-sale prices. This, in turn, would not only further discount asset values but also create a domino effect in the broader financial system. The potential scale of losses for hedge funds, and their bank lenders, can be illustrated through the VaR (Value at Risk) and stress-testing models, which analyze risk exposure based on market movements. Under normal market conditions, hedge funds might be expected to lose up to 5% of their portfolio value on a bad day. However, during periods of high volatility or market stress, losses could easily escalate. For example, a stress test simulating a 10% drop in equity markets, a 20% increase in volatility, and a sharp widening of credit spreads could result in portfolio losses exceeding 30% for heavily leveraged funds. These losses would cascade through the system, with banks holding significant funding to these hedge funds facing billions in potential losses.

One of the main challenges in estimating the full scope of these risks lies in the opacity of hedge fund operations and the off-balance-sheet derivatives positions that often don’t appear in public financial statements. Hedge funds frequently use instruments like total return swaps and credit default swaps (CDS), which allow them to take on massive market exposure without having to report the full extent of these positions to regulators. This lack of transparency amplifies the difficulty of assessing systemic risk and increases the likelihood that sudden shocks could catch financial institutions off guard. As hedge fund leverage spikes, so does the risk of forced deleveraging. Banks, particularly those with large exposure to hedge fund borrowing, could face liquidity constraints and capital losses. If a significant number of hedge funds face margin calls, banks would have to absorb losses from their loans, possibly leading to a sharp deterioration in their balance sheets. Given that banks like Goldman Sachs, JPMorgan Chase, and Morgan Stanley already have significant derivative exposures—Goldman Sachs alone holds $54 trillion in derivatives, dwarfing its $151.46 billion in market capitalisation while having $ 1.64 Trillion in assets which in part can be customers’ bank deposits—these losses could lead to a systemic banking crisis. The ripple effects could lead to a severe tightening of credit markets, further exacerbating the economic downturn.

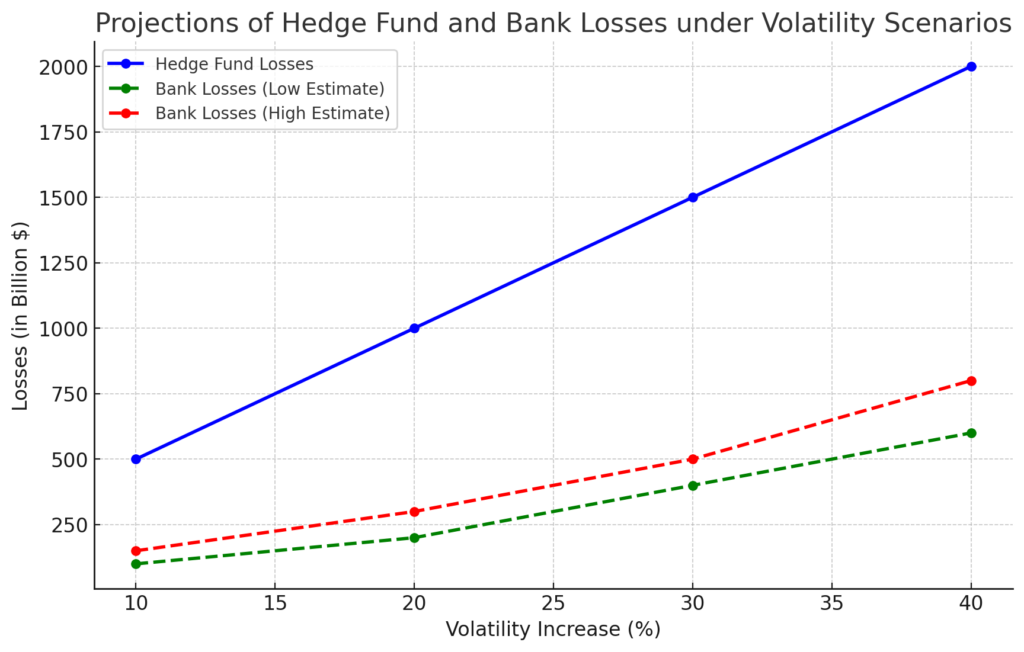

Moreover, historical analysis of periods of extreme volatility, such as the 1998 Long-Term Capital Management (LTCM) collapse or the 2007/08 financial crisis, shows that hedge funds tend to exacerbate market downturns by selling into falling markets. This forced selling can lead to further declines in asset prices, creating a vicious volatility effect where both hedge funds and banks suffer increasingly severe losses. If a significant portion of the $28 trillion in hedge fund leverage were to be unwound suddenly due to margin calls or market stress, it is conceivable that the financial system could experience losses on the scale of trillions of dollars, rivalling or even exceeding those seen during the 2008 financial crisis. In the current environment, where interest rates remain high, inflationary pressures persist, and geopolitical uncertainties, the possibility of volatility events triggering a massive deleveraging scenario for hedge funds is a real unmanageable risk. For banks with massive exposure to hedge fund leveraged funding and derivatives positions, the consequences could be catastrophic. Stress tests and risk projections show that even a modest increase in volatility or a sharp market downturn could lead to losses ranging from $500 billion to over $1 trillion in aggregate across major U.S. banks, severely undermining their capital positions and threatening overall financial stability.

The graphs below illustrate these dynamics, showing projections of hedge fund losses under different volatility scenarios, as well as the potential impact on major banks’ capital buffers. In a worst-case scenario, where volatility spikes by 40% and equity markets decline by 20%, hedge fund losses could easily surpass $2 trillion, with banks exposed to these funds suffering losses in the range of $300 billion to $800 billion.

Reckless Risk of Derivatives in U.S. Large Banks

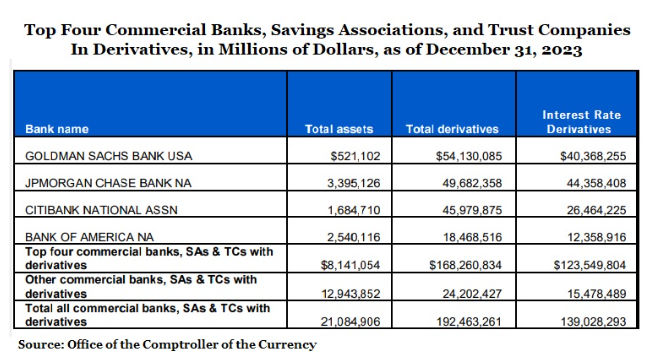

The staggering exposure of U.S. banks to derivatives is a critical point for the financial system. As of December 31, 2023, four megabanks—Goldman Sachs, JPMorgan Chase Bank, Citibank, and Bank of America—held $168.26 trillion in derivatives, accounting for 87% of the total $192.46 trillion in derivatives held by all 4,587 federally insured financial institutions in the U.S. The sheer size of these derivative positions is alarming, particularly when compared to the actual asset base of these banks. For instance, Goldman Sachs Bank USA, with $151,46 billion market capitalisation, holds $54 trillion in derivatives, underscoring an enormous level of leverage concentrated within a single institution. This disproportionate relationship between assets and derivatives demonstrates the extreme level of risk these institutions are allowed to carry, with limited capacity to absorb potential losses. The enormous exposure of the $192 trillion derivatives makes it virtually unsolvable and banks insolvent within the existing regulatory framework. The sheer scale of these positions, many of which involve complex and opaque financial instruments, poses a systemic threat that is beyond the capacity of any central bank or regulatory body to manage. Even in a scenario where a fraction of these positions deteriorate, the interconnected nature of these derivatives across financial institutions could trigger a domino effect, resulting in widespread financial instability. The concentrated risk in a small number of banks further amplifies the potential for catastrophic losses, and despite the lessons of the 2008 financial crisis, reforms such as Dodd-Frank have proven inadequate in curbing this risky behaviour. These financial derivative risks, largely hidden from public scrutiny and challenging to evaluate in real-time and on a marked-to-market basis, pose a significant threat to the stability of the financial system. The amount of potential risks could overwhelm the capacity of central banks to intervene or restore stability and solvency in the event of a major market disruption.

Concealment of Unrealized Losses

Another critical aspect of the current financial environment is the concealment of unrealized losses on balance sheets, particularly by major banks. Bank of America, for instance, has reported unrealized losses on its Held-to-Maturity (HTM) debt securities amounting to $106 billion. This figure represents 34% of the total unrealized losses reported by banks across the industry. HTM securities are recorded at amortized cost on the balance sheet, which means that fluctuations in their market value are not immediately visible in financial statements unless the securities are sold. The unrealized losses on HTM securities highlight a significant issue: while these losses are not realized and do not directly impact cash flow, they affect the overall financial health of banks. For Bank of America, the scale of these losses is particularly concerning. The $106 billion in unrealized losses represent a substantial portion of its balance sheet, an amount that represents 35% of the overall market capitalization of Bank of America, exposing the bank to very large market risk in terms of the bank shares prices and its equity line. Although HTM securities are intended to be held until maturity, the magnitude of these losses raises questions about the bank’s capital adequacy and its ability to absorb potential financial stress. In addition to HTM securities, banks also engage in off-balance-sheet activities and use complex derivatives, which can further obscure the true extent of their financial risks. These practices can create a misleading picture of a bank’s financial position, masking the real risks associated with their investment portfolios and lending activities.

Regulatory Concerns and Systemic Risk

The Bank for International Settlements has flagged significant concerns regarding the opacity of financial bets made by hedge funds and non-bank financial institutions. Trillions of dollars in opaque financial positions, involving complex derivatives and off-balance-sheet activities, pose substantial risks to the financial system. These financial instruments are often difficult to assess and understand, leading to potential underestimation of the risks involved. The interconnectedness of hedge funds, non-bank financial institutions, and major banks amplifies systemic risk. The intricate web of financial relationships means that problems in one area can quickly spread throughout the system, affecting other institutions and potentially leading to a broader financial crisis. The scale of these risks, combined with the complexity of financial instruments, poses a significant challenge for regulators and policymakers. The potential for deleveraging with sudden high volatility and systemic collapse is a pressing concern. The combination of high leverage, concealed losses, and opaque financial practices creates a volatile environment. If hedge funds or major banks encounter severe financial difficulties, the resulting stress could threaten the stability of the entire financial system. Central banks, while equipped with tools to provide liquidity and stabilize markets, may find their capacity to manage or contain such a crisis constrained by the scale and complexity of the risks involved.

The current financial landscape is characterized by high levels of hedge fund leverage, significant exposure of major banks, and substantial unrealized losses on balance sheets. The combination of these factors creates a volatile and risky environment, raising concerns about the stability of the financial system. The concealment of unrealized losses, particularly at major banks like Bank of America, adds another layer of complexity to the situation. The opacity of financial bets and the interconnectedness of the financial system pose systemic risks that could potentially lead to widespread financial instability. As the situation evolves, it is crucial for regulators, financial institutions, and policymakers to address these challenges with enhanced transparency, robust risk management practices, and effective oversight to mitigate potential threats to the global financial system.