When considering the simple data of United States GDP of $27.3 Trillion Dollars in aggregate compare and contrast with United Kingdom GDP $ 3.34 Trillion Dollars, then with virtue of simple proportion anybody can understand that the United States GDP is 8.17 Times larger, in aggregate GNI, then the UK economy, which equates to roughly a mere 12% of the United States economy ; thereof in light of this simple fact becomes obvious to see how the British Pound is still grossly overvalued across the board and why the exchange rate level toward the USDollar could have to drift below parity in order to reflect the macroeconomic differences between the two countries, and the reliance of the UK economy from dollar investments, these pressures can inevitably generate volatility in FX market and meaningful repricing and depreciation of the Pound, something that the ugly Americans will ask themselves, if and when the UK would like to see more investments, the economic incentives have to be in place, such as a favourable exchange rate and thereof higher purchasing power of the USDollar over the British Pound, and this GBP/USD drift is going to materialise slowly but surely, particularly as Fiscal Deficits shocks will materialise.

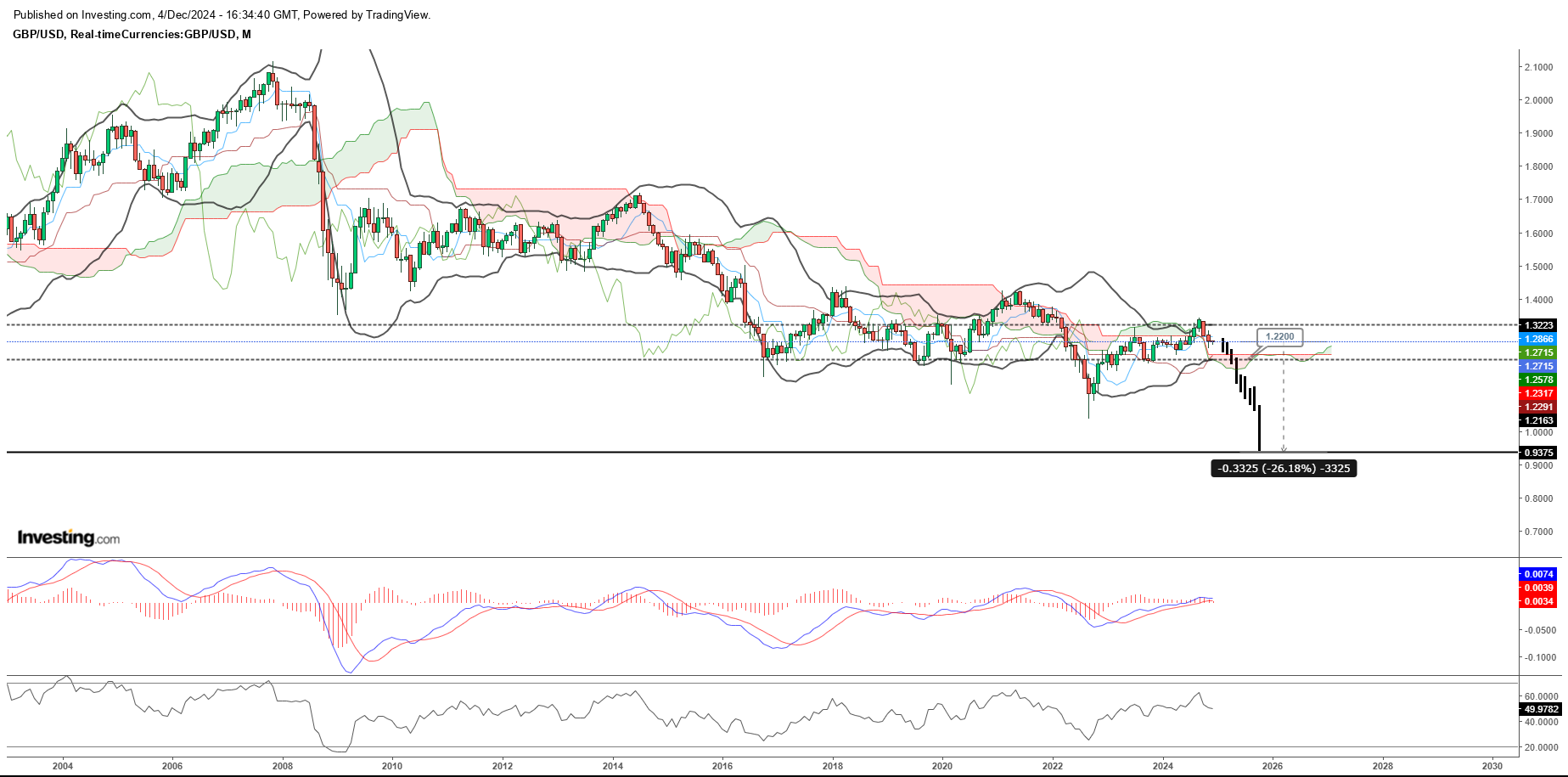

With the chart of the GBP/USD exchange rate, it’s possible to observe the exchange rate drift pattern and it’s a steady stochastic pattern drifting lower, with large shocks of depreciation. At this timeframe in Q4, the chart is on a monthly timeframe and GBP/USD drifts onto the Bollinger Band GBP/USD 1.322 speculative level to in fact then generate a reversal Sell signal drifting lower where the future exchange rate level could have to be GBP/USD 1.22 thereby explaining how GBP was 10cents grossly overvalued. Observing the technical indicators the chart highlights that every time GBP/USD drifts onto the Bollinger upper Bound and Ichimoku Senkou then trend reversal and long periods drifting lower are a mechanistic outcome; in this Q4 time framework, the Bollinger upper Band and IKH Senkou trend reversal have already set in motion, while observing the oscillators as MACD and RSI 49.97 both are tracing the trend reversal and drift downward of GBP/USD, while it’d take a little bit of time to see the MACD moving average line crossing to the downside, but it’s getting there. In the long term, a fair exchange rate level of British Pound/USDollar could have to be GBP/USD 0.935 | 0.92.

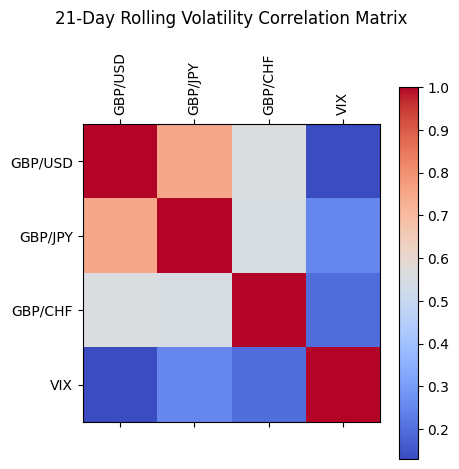

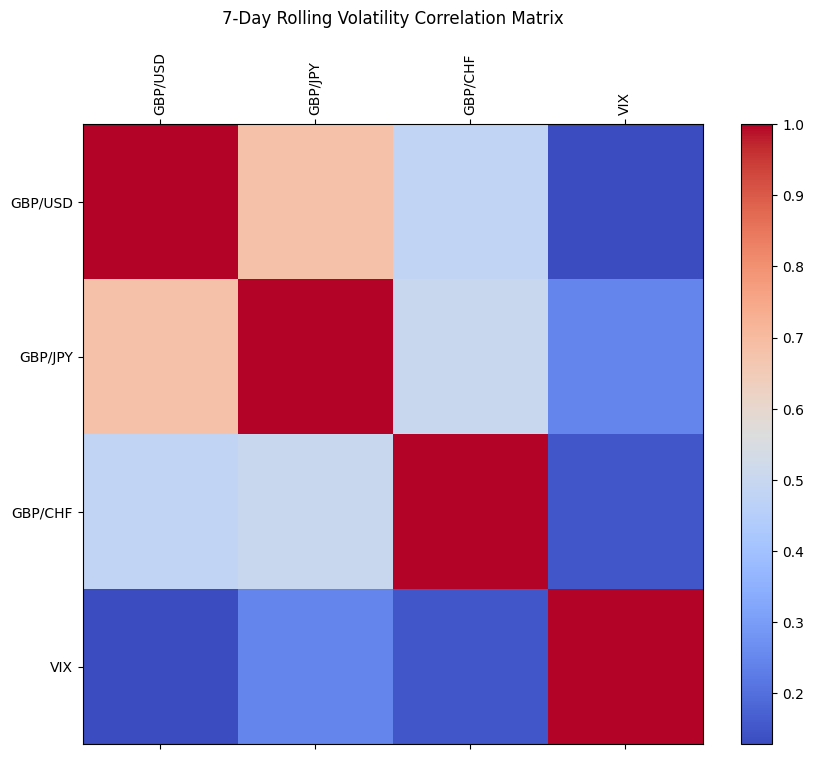

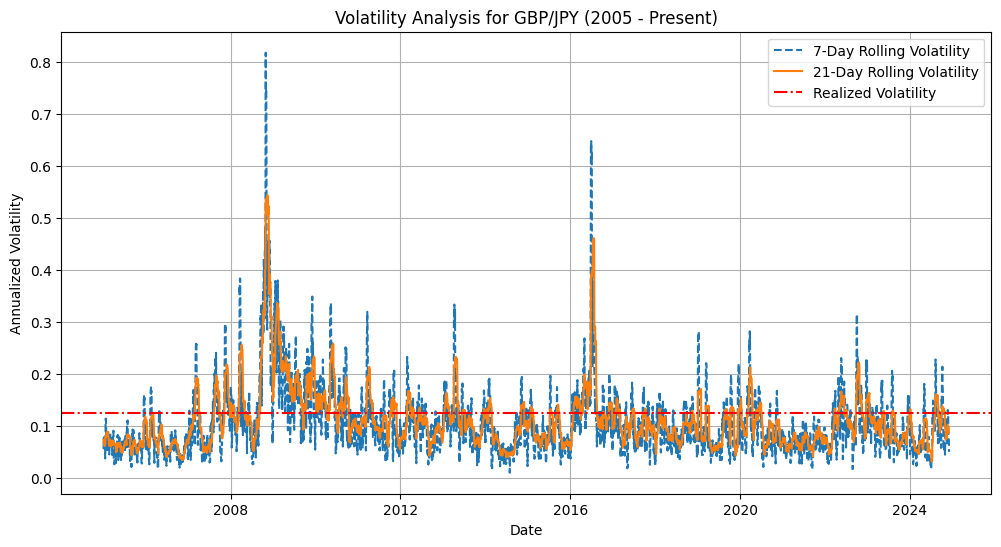

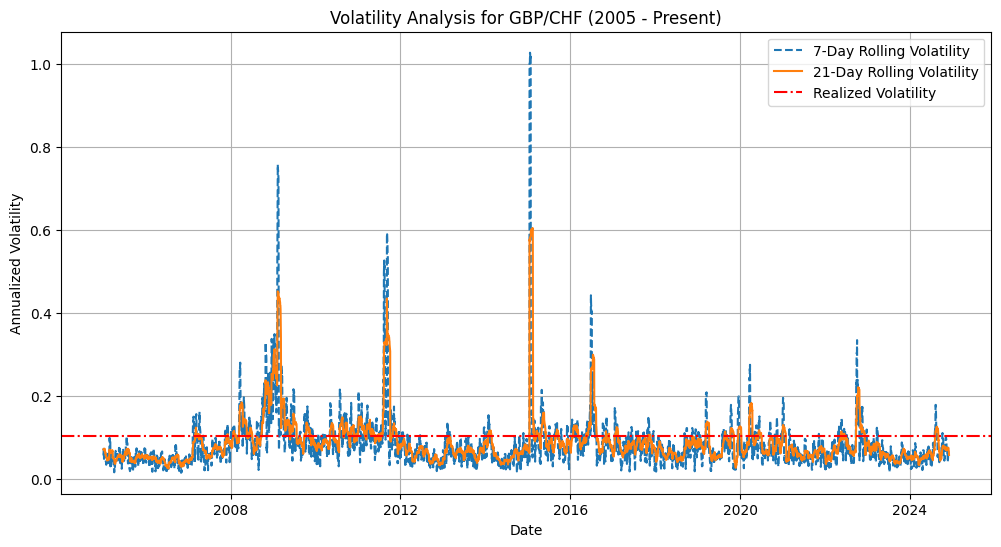

After observing the GBP/USD chart on a monthly timeframe, detailed British Pound volatility research has been made across three major G10 currencies pair, GBP/CHF, GBP/JPY, GBP/USD, in order to have a thorough picture of the volatility risks that carries through the British Pound and below the graphs of the 7-Day and 21-Day Rolling Volatility matrices results can be observed, out of 2005/2024 timeseries, and GBP/USD has moderate to strong correlation with GBP/JPY and a moderate correlation coefficient with GBP/CHF, meaning that market risk in one exchange rate mirrors also in other exchange rates and other G10 currencies.

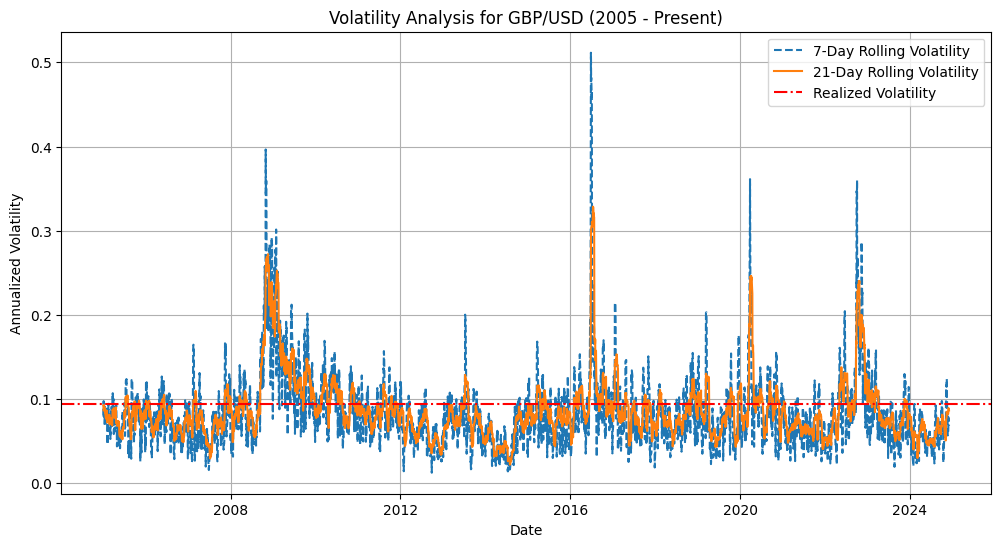

Here we can see the actual data of additional volatility analysis in terms of the annualised and realised volatility thresholds and the 7-day and 21-day rolling volatility average inference, through which it’s possible to see short-term 7-day rolling average volatility has been crossing above the realised volatility threshold as the exchange rates fluctuations reverberate in their volatility averages.

Realized Volatility (Annualized): GBP/USD 0.093830 GBP/JPY 0.124073 GBP/CHF 0.103960

Going forward a thorough volatility analysis has been applied to GBP/USD, GBP/JPY, GBP/CHF time-series 2005/2024, in this framework have been utilised a variety of econometrics tools, such as ARIMA(1,0,1), GARCH(1,1), EGARCH, GRJ-GARCH, and these have been worked through GBP/USD Greeks Option Volatility parameters resulting in consistent striking results of inference between historical time-series volatility and option implied volatility, the variance parameters have been set with a 6-months horizon forward forecast, with utilizing GBP/USD June’25 Option Greeks data in order, as said to compare historical volatility, with forward-looking Greek Option strikes implied volatility.

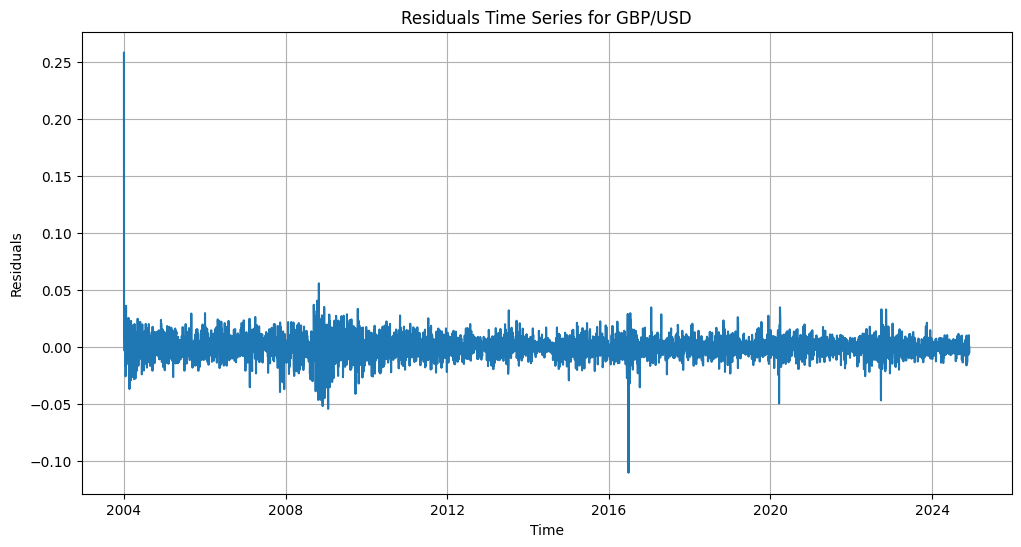

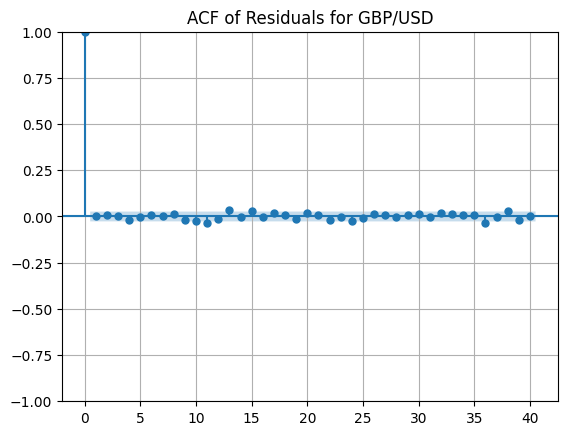

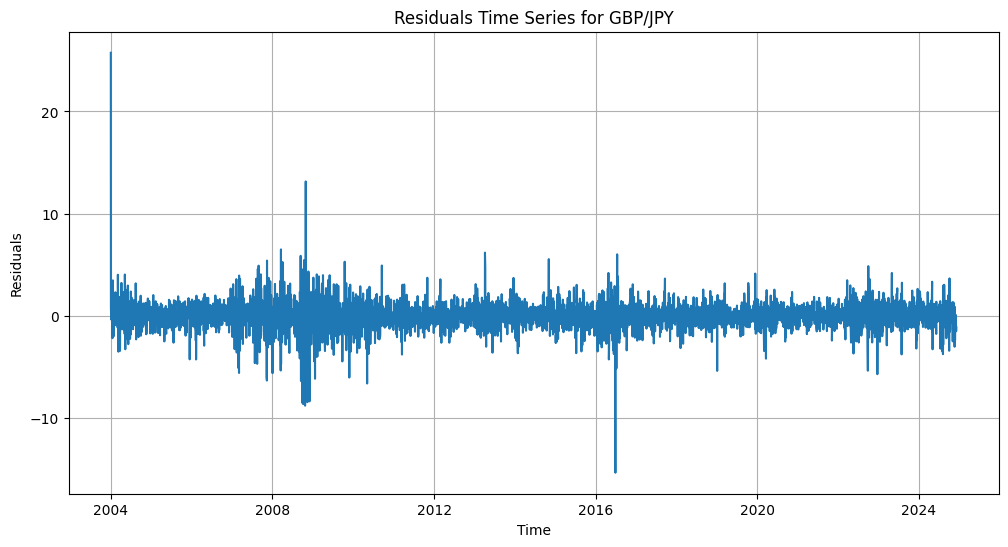

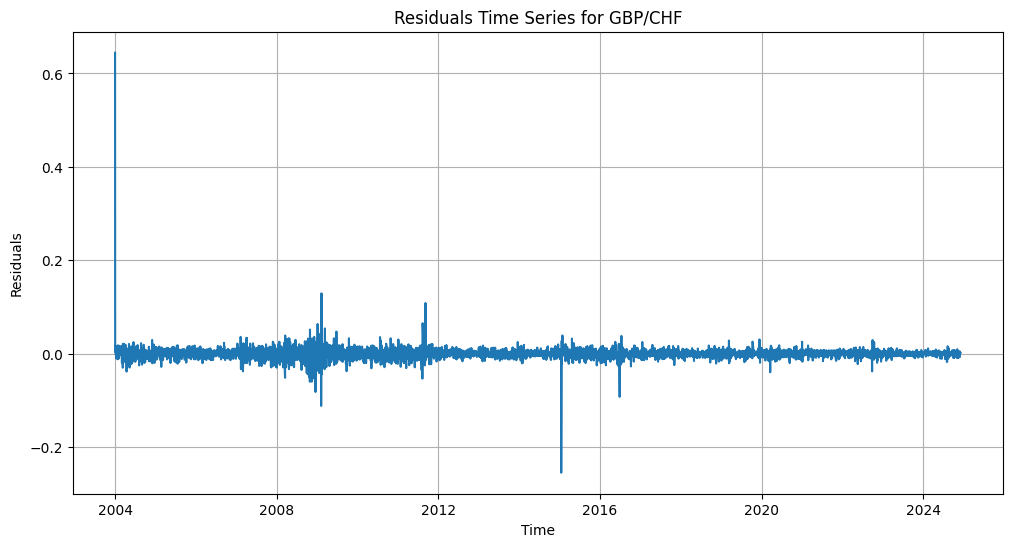

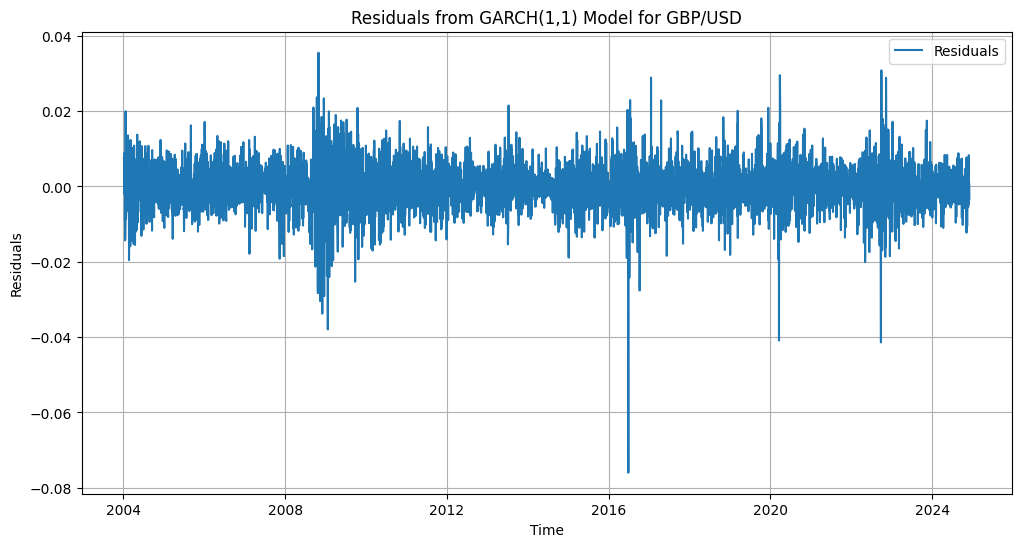

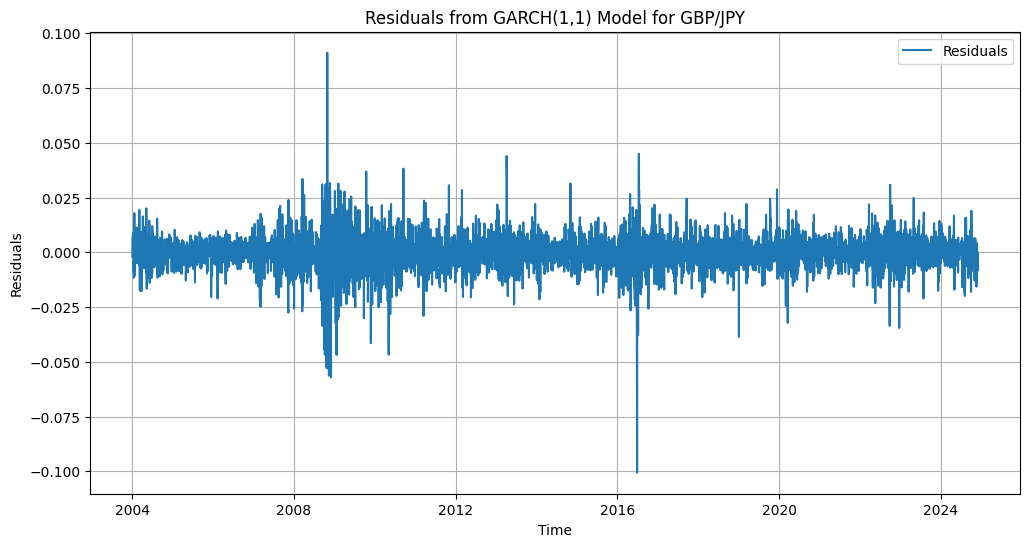

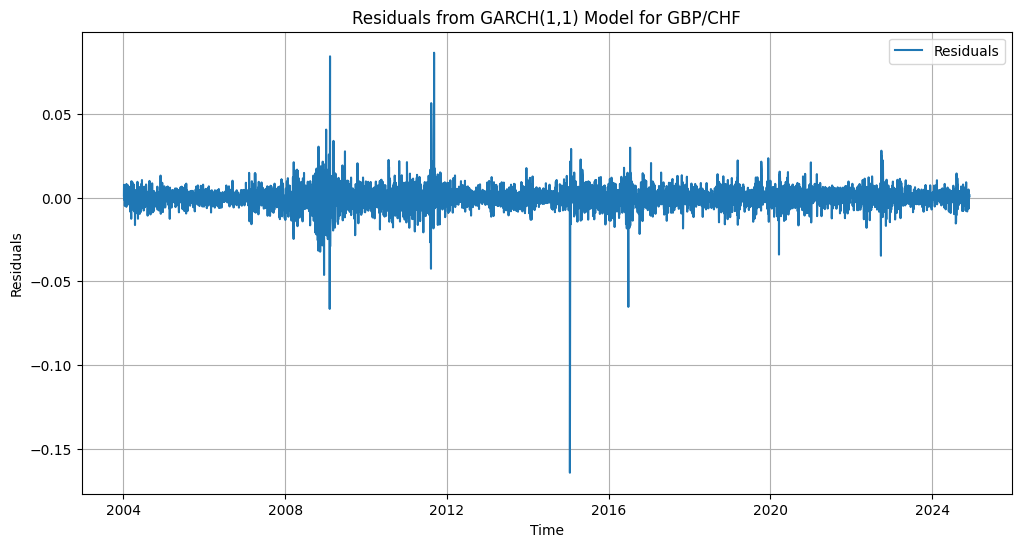

GBP/USD, GBP/JPY, GBP/CHF time-series and their residual variance errors have been tested for stationarity and the relevant graphs, including ACF, in order to extrapolate autocorrelation and confirm stationarity. Residual statistics results of the currencies pair highlight how the mean is close to zero indicating stationarity, also residuals’ distribution, as indicated by the quartiles and standard deviation, is reasonably symmetric, supporting the assumption of white noise. Min and Max values also explain how residuals are larger than most values in the distribution, which could indicate a few outliers and deviations.

Residual Statistics for GBP/USD: count 5442.000000 mean -0.000047 std 0.009642 min -0.110428 25% -0.004824 50% -0.000086 75% 0.004799 max 0.257877

Residual Statistics for GBP/JPY: count 5446.000000 mean 0.004294 std 1.317695 min -15.360604 25% -0.589966 50% 0.035266 75% 0.655113 max 25.744663

Residual Statistics for GBP/CHF: count 5445.000000 mean -0.000093 std 0.013481 min -0.254998 25% -0.004649 50% 0.000057 75% 0.004632 max 0.644361

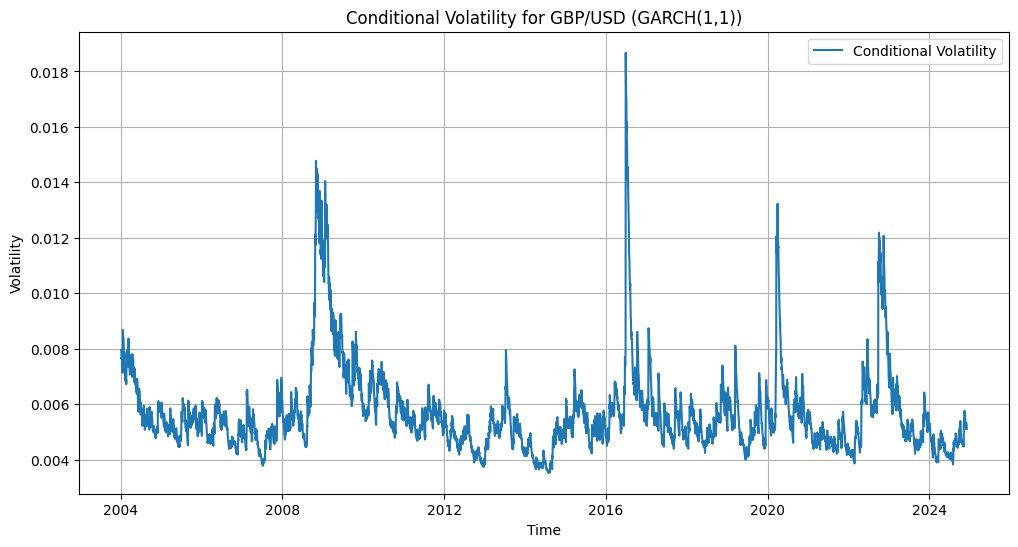

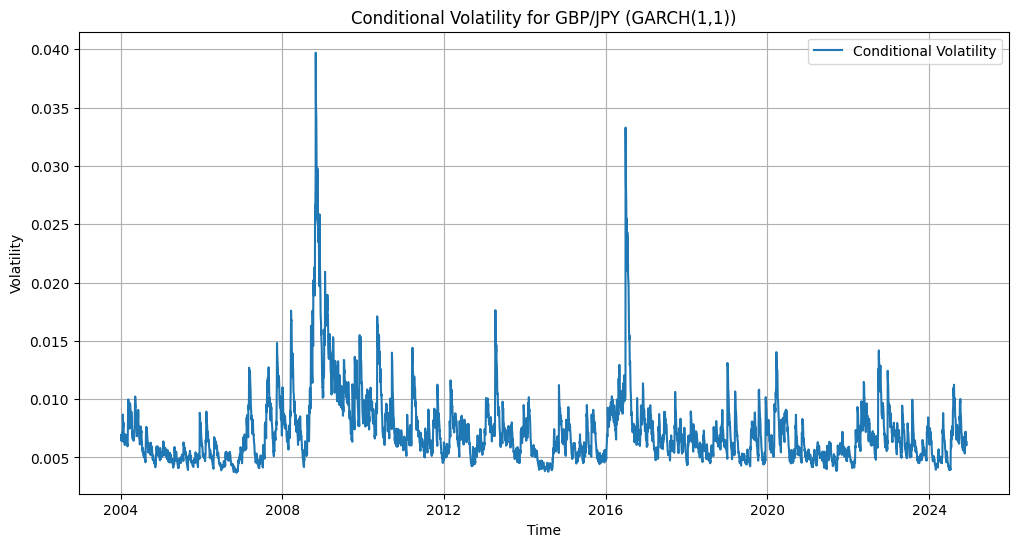

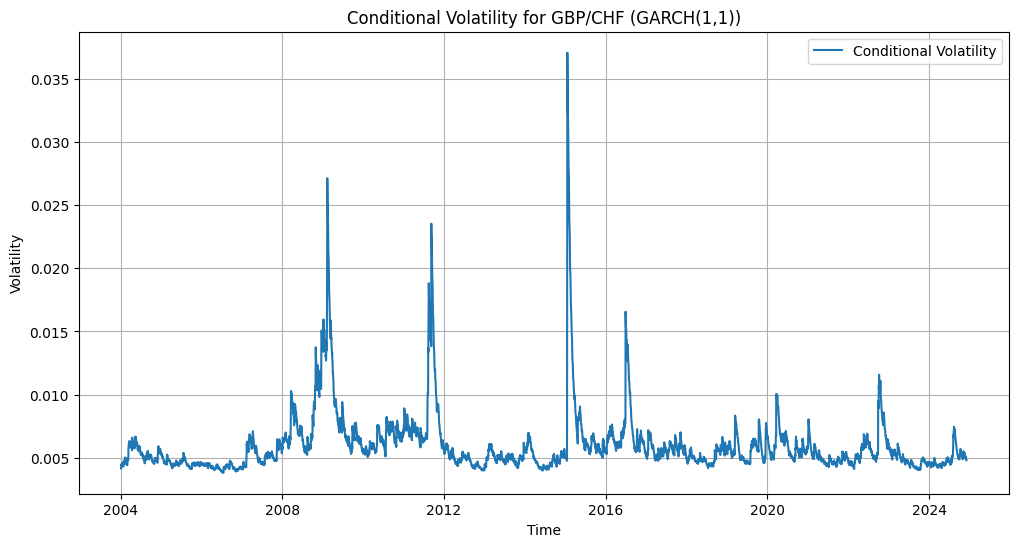

Timeseries volatility study has been implemented with GARCH(1,1) models statistical results have found that GBP/USD, GBP/JPY, GBP/CHF are characterised by persistent volatility according to the Alpha, Beta parameters, AIC and loglikelihood parameters result confirm GARCH(1,1) good fit model, also considering the time-series have been tested for stationarity, only with GBP/JPY The mean return is approximately 0.000192, or 0.0192%, indicating that GBP/JPY is slightly favourable in speculative terms for carry trades. Although these GARCH(1,1) models have provided good fit statistical parameters to understand GBP/USD, GBP/JPY, GBP/CHF, time-series, then to improve the accuracy of the time-series volatility, additional EGARCH and GRJ-GARCH have been implemented to evaluate volatility and GBP/USD depreciation scenario.

News sensitivity Coefficient (alpha): 0.05

Persistence Coefficient (beta): 0.9299999999999999

News sensitivity Coefficient (alpha): 0.1000009063228464

Persistence Coefficient (beta): 0.8800000976412831

News sensitivity Coefficient (alpha): 0.05

Persistence Coefficient (beta): 0.9299999999999999

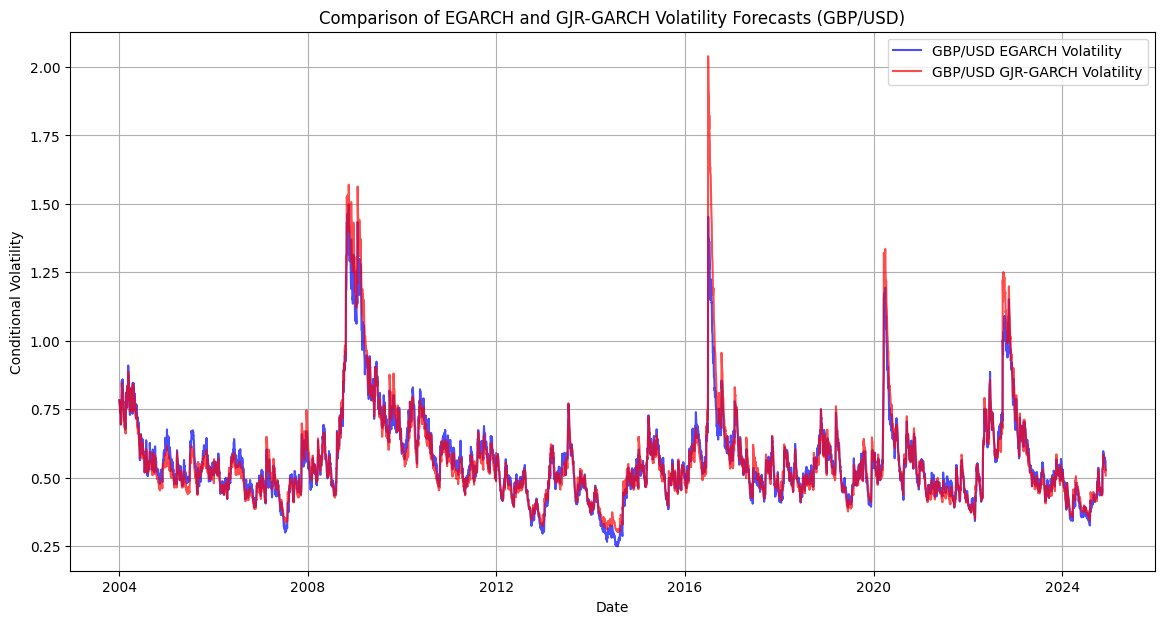

GBP/USD EGARCH and GRJ-GARCH Volatility Forecast have provided additional interesting results, as for example the (mu) parameter (-0.0751) negative mean suggests and reinforces the characteristic downdrift patterns of GBP/USD, FX market returns, while in fact, the Alpha (11.5912) high parameter indicates volatility highly sensitivity to past shocks. While the GJR-GARCH alpha[1] (0.0500) and beta[1] (0.9250): Indicate moderate sensitivity to past shocks and high volatility persistence and very similar to the GARCH(1,1).

GBP/USD Forecast Error Metrics:

Mean Squared Error (MSE): {'EGARCH': 0.34377443321485984, 'GJR-GARCH': 0.3553674343086202

Mean Absolute Error (MAE): {'EGARCH': 0.5627530680540531, 'GJR-GARCH': 0.5656862727236435

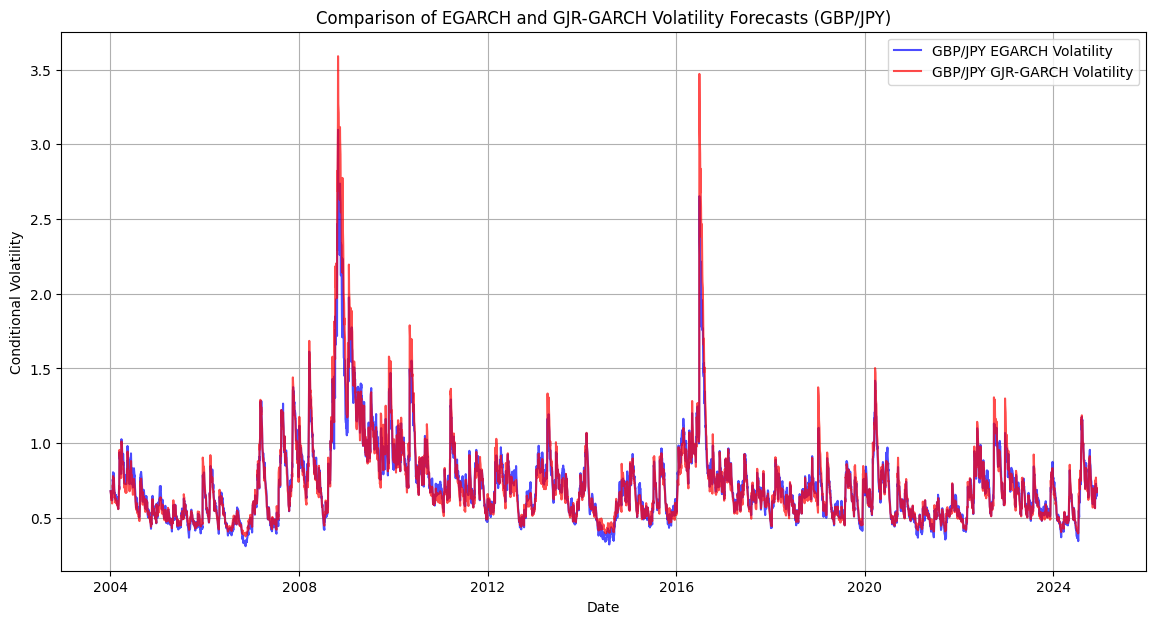

Also, the GBP/JPY EGARCH model results confirm the positive (mu) parameter positive mean(0.0002146) indicates as explained before, that GBP/JPY suggest positive returns for carry trades. Also parameters such as Alpha: Significant and relatively high (0.2407), suggesting past shocks have a noticeable impact on volatility Beta: High (0.9491), indicating persistent volatility.

GBP/JPY Forecast Error Metrics:

Mean Squared Error (MSE): {‘EGARCH’: 0.5942617933829542, ‘GJR-GARCH’: 0.6283851476016759}

Mean Absolute Error (MAE): {‘EGARCH’: 0.7197337544672445, ‘GJR-GARCH’: 0.7257685083498685}

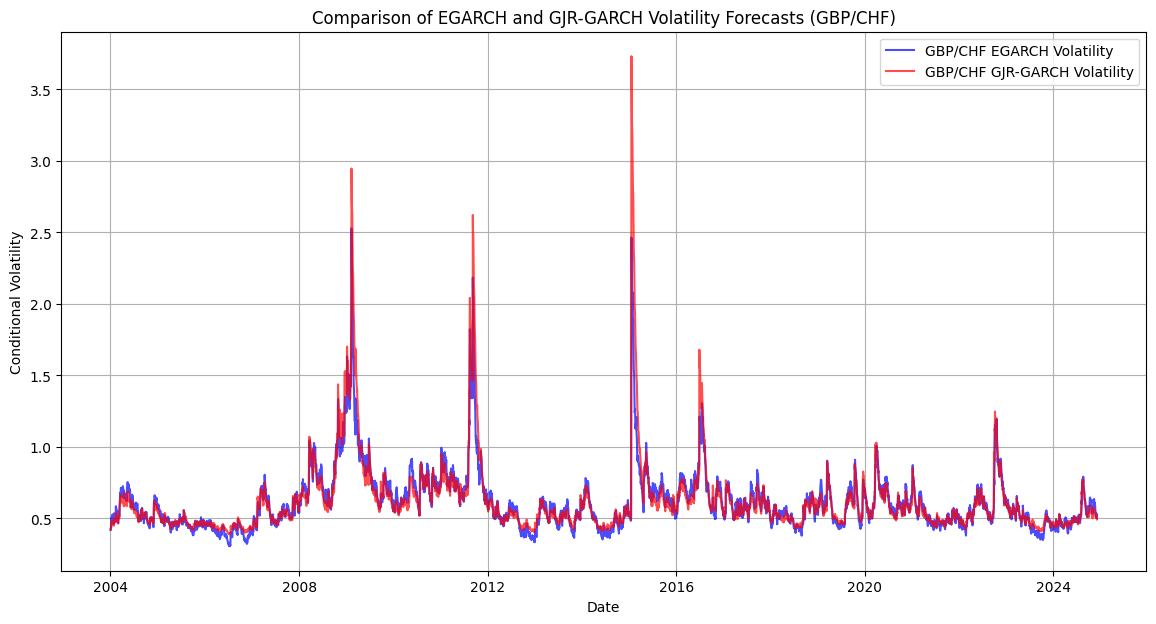

GBP/CHF Forecast Error Metrics:

Mean Squared Error (MSE): {'EGARCH': 0.42515110423157004, 'GJR-GARCH': 0.4623366427814213}

Mean Absolute Error (MAE): {'EGARCH': 0.6157776222005779, 'GJR-GARCH': 0.6239283048188192}

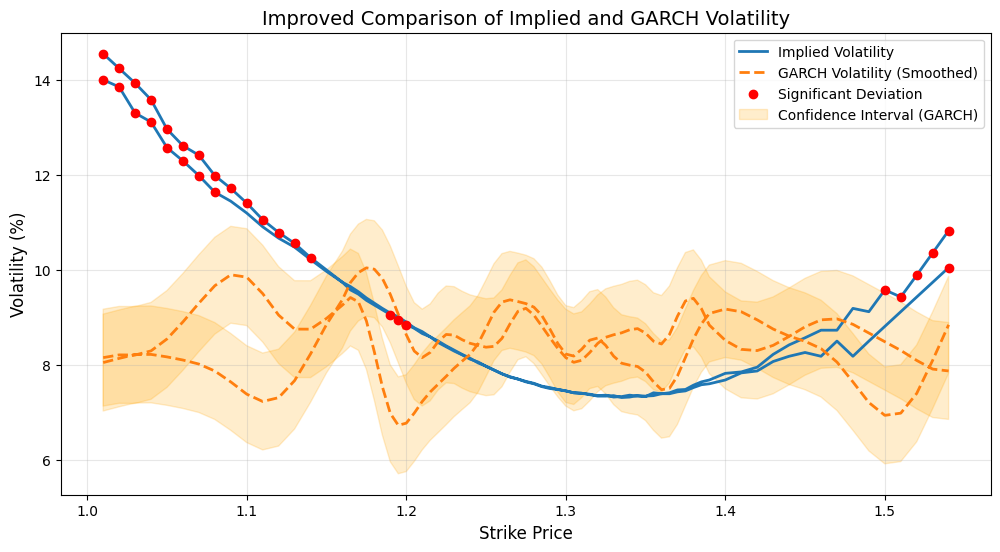

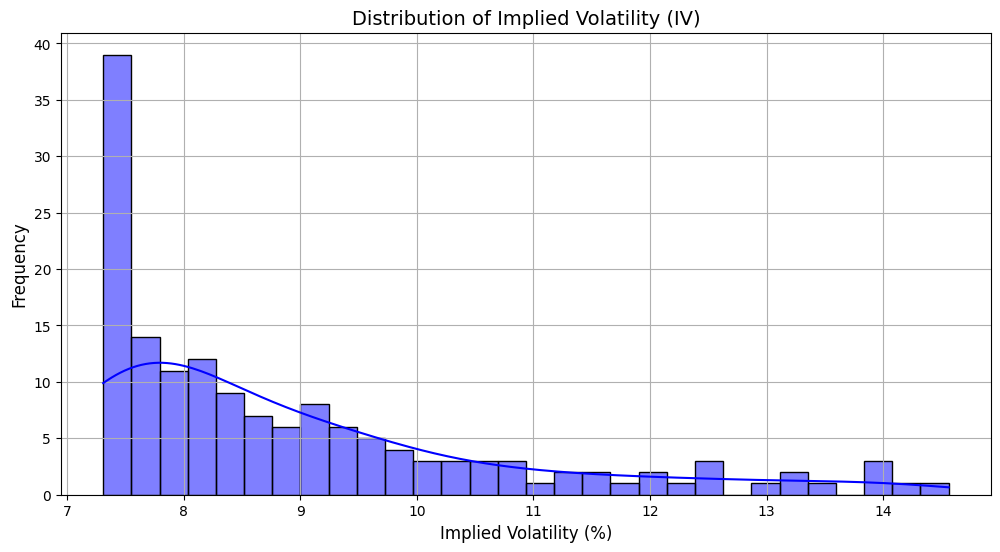

Last but not least, GBP/USD GREEKs of the option chain expiring in June’25 have been worked through to find the divergences between 6 months forward-looking Implied Volatility and the time-series historical volatility. Mean Implied Volatility: 8.94 Mean Smoothed GARCH Volatility: 8.48%. The higher mean IV compared to GARCH volatility suggests that market expectations are pricing in more risk than historical patterns justify, creating opportunities for strategic trades. The disparity between implied volatility and GARCH-derived historical volatility reveals potential mispricing in the options market for GBP/USD. Implied Volatility is consistently higher than historical volatility, particularly at extreme strike prices, indicating that market participants may be overestimating future risks. This misalignment presents an attractive opportunity to sell options or take short volatility positions, as options are likely overpriced. Furthermore, historical volatility patterns, as shown by the GARCH model, indicate that GBP/USD volatility has been stable in the mid-range, suggesting that the recent spikes in IV are more reflective of market panic or speculation than actual risk. The elevated IV makes it profitable to take put positions or short the GBP/USD pair, leveraging potential downward price movements while benefiting from inflated premium prices.

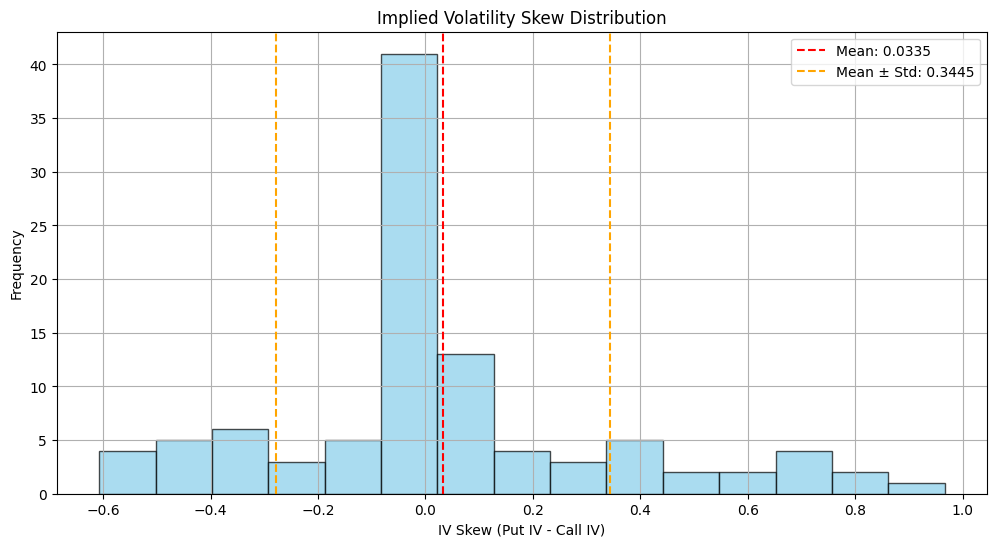

Mean Skew (0.0335): The mean skew is slightly positive, indicating that, on average, put options have slightly higher implied volatility than call options. This suggests the market is pricing in more downside risk for the underlying asset. Standard Deviation (0.3445): The IV skew varies significantly, with some fat-tail extreme positive and negative values evident in the histogram. Skewness (0.6500): The distribution is moderately positively skewed, indicating a bias towards scenarios where puts are more expensive than calls, though the majority of the values are clustered near zero. The positive skew in the IV distribution and the high Z-scores at higher strike prices indicate that the market is pricing puts with much higher implied volatility. This is a common behaviour in bearish or uncertain markets, where downside protection becomes more expensive due to increased demand. The combination of skewness and elevated Z-scores highlights asymmetric risk pricing: traders are more concerned about downside risks and are willing to pay a premium for puts.

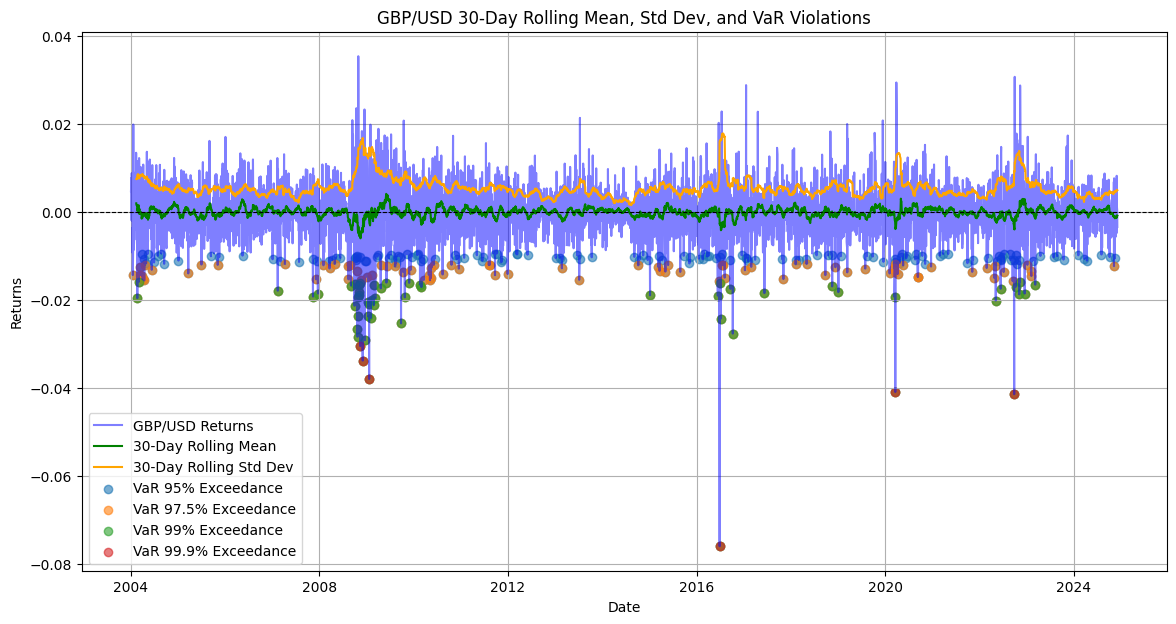

VaR 95%: -0.00943, Exceedances: 272 VaR 97.5%: -0.01180, Exceedances: 136 VaR 99%: -0.01582, Exceedances: 55 VaR 99.9%: -0.02990, Exceedances: 6

The Value at Risk (VaR) analysis highlights significant exceedances at multiple confidence levels, indicating a higher frequency of larger fat-tail volatility than expected under typical market conditions. At the 95% VaR (-0.00943), 272 exceedances are observed, suggesting that losses surpassing this threshold occur far more often than the model predicts. Similarly, for the 97.5% VaR (-0.01180) and 99% VaR (-0.01582), the 136 and 55 exceedances, respectively, exceed what a normal distribution would expect. Finally, the 99.9% VaR (-0.02990) shows six extreme violations, representing rare but substantial tail risks. This pattern of frequent violations implies that the market is pricing in heightened volatility and downside risks, reflecting current market instability or an underestimation of fat-tailed events in the model.

Observing these dynamics, a trading strategy focused on leveraging downside risks in the next three months is prudent. The elevated exceedance frequency aligns with a bearish outlook, making short positions in the underlying asset (e.g., GBP/USD) attractive to capitalize on anticipated price declines. Additionally, deploying options strategies, such as buying puts or constructing put spreads, allows traders to profit from amplified volatility while limiting downside exposure. The frequent tail events suggest that option premiums, particularly on downside protection, may be justified by actual risk, making these strategies both defensive and opportunistic in volatile conditions.

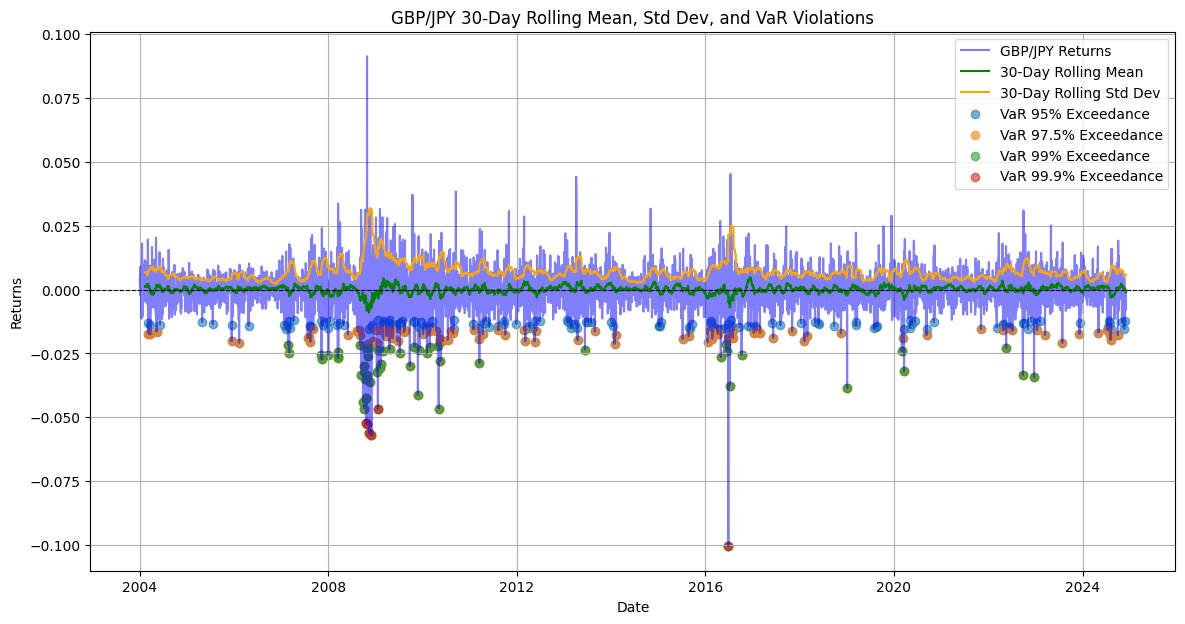

GBP/JPY VaR 95%: -0.01203, Exceedances: 273

GBP/JPY VaR 97.5%: -0.01554, Exceedances: 137

GBP/JPY VaR 99%: -0.02135, Exceedances: 55

GBP/JPY VaR 99.9%: -0.04661, Exceedances: 6

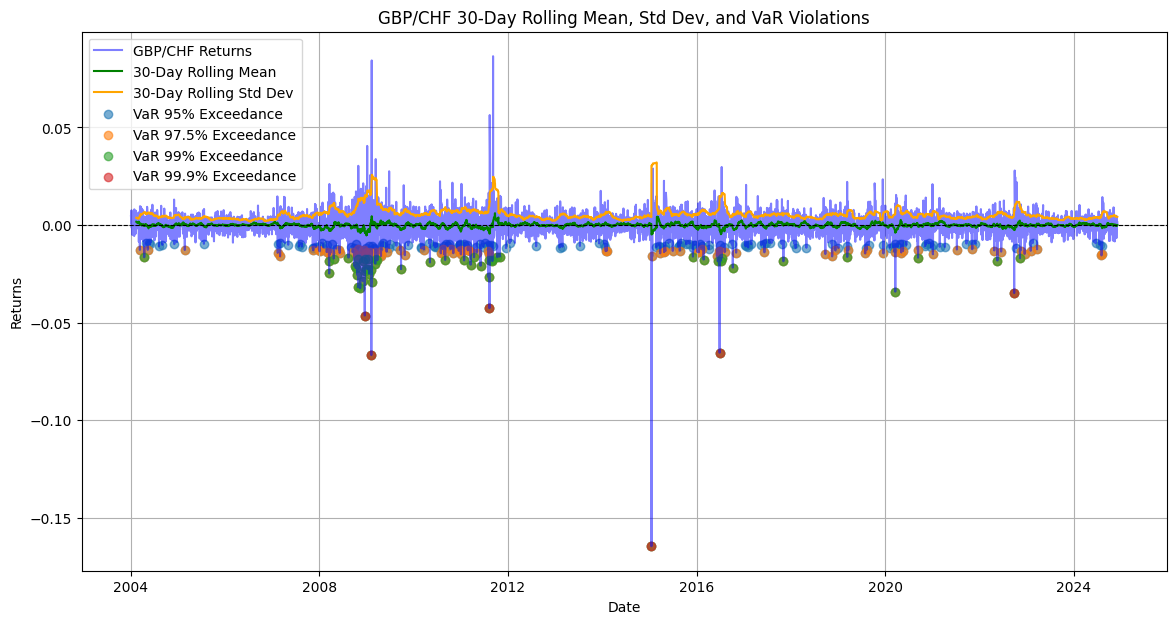

GBP/CHF VaR 95%: -0.00918, Exceedances: 273

GBP/CHF VaR 97.5%: -0.01232, Exceedances: 137

GBP/CHF VaR 99%: -0.01610, Exceedances: 55

GBP/CHF VaR 99.9%: -0.03451, Exceedances: 6

Suggested Data Sources:

https://finance.yahoo.com/

https://www.cboe.com/

https://data.nasdaq.com/

https://www.bloomberg.com/markets