The public is rightly concerned about the rising cost of living, and the dominant economic narrative offers what seem like simple truths: falling prices are a bad omen, and we must accept higher unemployment as the bitter medicine needed to cure inflation. But this conventional wisdom isn’t just wrong—it’s dangerously flawed, leading to policies that inflict pain on households while fundamentally misunderstanding the disease. A deep dive into the hard data reveals a completely different story. The real drivers of inflation and the true preconditions for a recession are not what we’ve been led to believe. The analysis uncovers five surprising truths that shatter the old playbook and demand a new way of thinking about the economy.

The Real Recession Predictor Isn’t Falling Prices, but Persistently High Inflation

The common belief is that disinflation—a slowing rate of price growth—signals an impending recession. The data shows this is backward. Persistently high inflation is the true precondition for an economic crisis, and disinflation is merely the symptom that appears after the damage is done. Look no further than the 2008 financial crisis. A massive inflationary shock, driven by a colossal asset bubble, preceded the collapse. Even as the underlying demand for goods and services became sluggish, businesses financed by inflated debt were forced to keep prices high just to cover their soaring operating costs. The economy was already cracking under the strain of high prices well before the bubble popped. By the time you see negative price growth, you aren’t heading into a recession; you are already in one. When you have persistent high inflation, it’s what leads you into a recession thereafter. So that’s why price stability has to be tackled before, otherwise the posterior distribution, the posterior probability distribution of the effects that propagate into the economy, they are likely to be recessive. This insight is critical for policymakers and the public. The time to worry is not when inflation starts to cool, but when it remains stubbornly high, signalling that a severe contraction may be the only way the system can correct itself.

Why Pushing People Into Unemployment Won’t Fix Inflation

A core tenet of modern economic policy is that to control inflation, you must crush aggregate demand, typically by forcing people out of work. This entire strategy is fundamentally flawed, treating the symptom, consumer demand, while ignoring the disease: structural, supply-side inflation. The evidence from the UK is undeniable: unemployment is rising, yet inflation remains stubbornly above the 2% target. This policy fails because it ignores two realities. First, domestic demand can be substituted by external sources, such as millions of tourists, whose spending props up prices regardless of local hardship. Second, and more importantly, this is an aggregate supply problem, not an aggregate demand one. Businesses are saddled with inflated corporate debt and persistent supply chain costs, forcing them to keep prices high to survive, even when faced with sluggish domestic sales. You can push the whole population unemployed, and you have everyone on benefits. Inflation will not go to 2% because prices are dynamic, and there are so many other things that aggregate demand on its own does not explain the level of prices. Policymakers are inflicting the economic pain of unemployment on households without solving the underlying structural issues driving prices. It’s a strategy doomed to fail.

It’s Not a Price-Wage Spiral; It’s a Financial Asset-Inflation Spiral

Today’s inflation is dangerously intertwined with financial asset bubbles, creating a vicious feedback loop. Inflated assets are financed by inflated debt. Businesses, in turn, pass these higher financing costs onto consumers through higher prices in the real economy. This dynamic is now more pernicious than ever because the housing market cycle has become synchronised with the broader inflation cycle. This means consumption in the real economy is more directly driven by inflating financial assets—a feedback loop that is “trillions and trillions of times more dangerous than a price wage spiral.” The current artificial intelligence bubble is a perfect example: it’s financed by mountains of corporate debt but has yet to produce any tangible aggregate supply improvements that would lower costs for the economy. It is, for now, purely inflationary. Popping this kind of asset bubble doesn’t just correct market froth; it threatens to bring the entire real economy down with it.

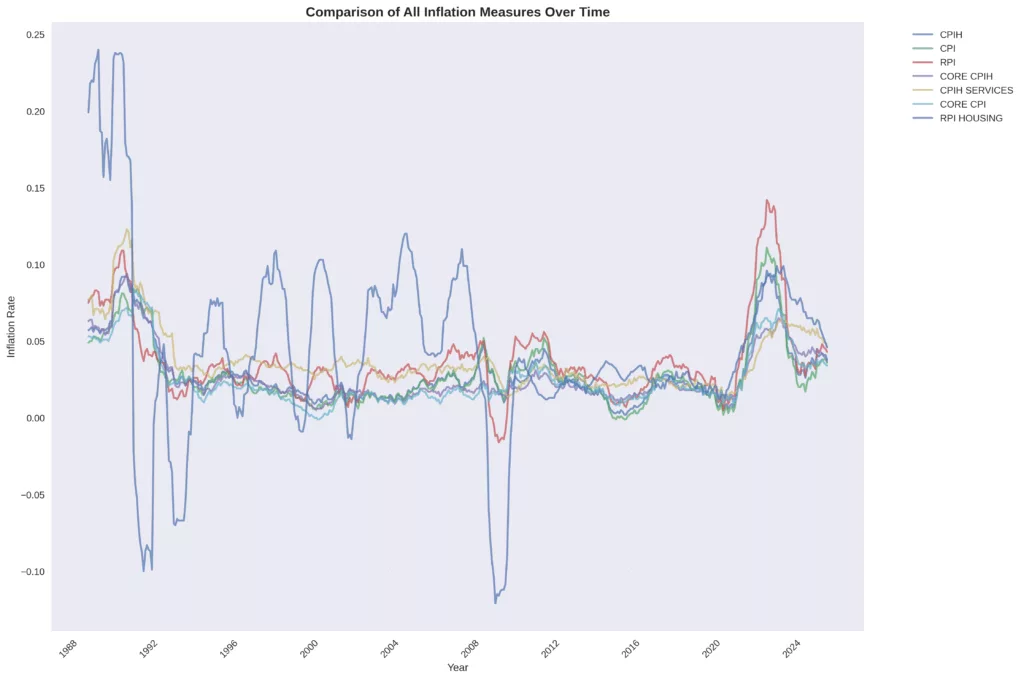

“Temporary” Inflation Is a semiotic fabrication, The Real Inflation Cycles Last a Generation

The narrative that the recent inflationary shock was “temporary” represents a fundamental failure to understand how prices behave over time. Once a significant inflationary pressure enters the system, its effects are persistent and long-lasting. A rigorous analysis of long-term economic data reveals a stunning reality about inflation cycles: The dominant inflationary cycle for broad measures like the Consumer Price Index (CPI) and Retail Price Index (RPI) is 18 years. For services and core inflation, the cycle is even longer at 36 years. Even the shortest cycles identified in the data last for five years. The idea that a major inflationary event is just a short-term “blip” is, frankly, a fantasy. There is no in this world there is no such a thing as temporary inflationary pressures Okay So the Federal Reserve was wrong and uh they have made a lot of effort in uh controlling inflation and I don’t know how they are u how they are doing about that. This long-term perspective is vital. It means that once inflation takes hold, policymakers must be prepared for a years-long battle, not a problem that will resolve itself.

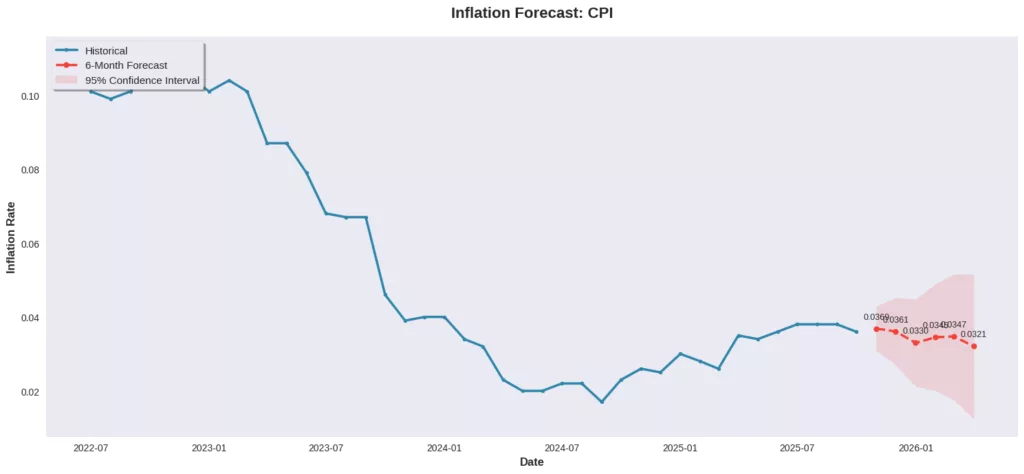

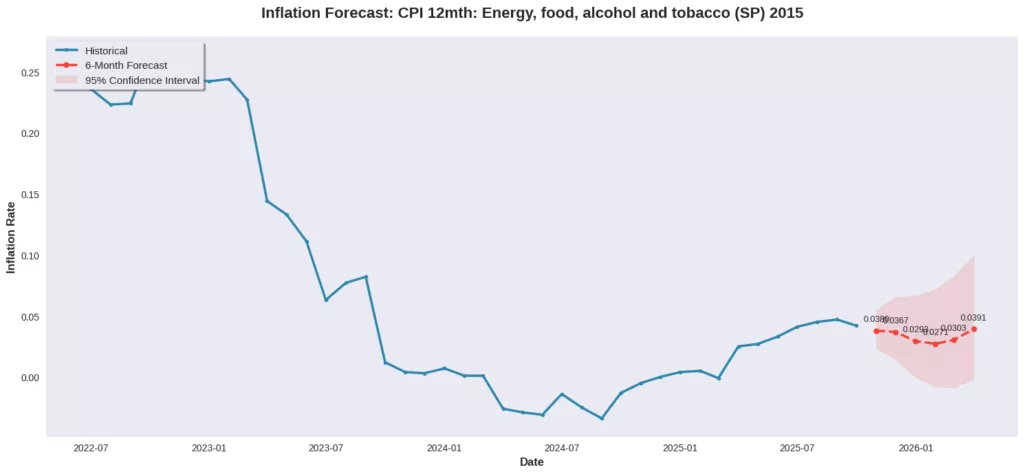

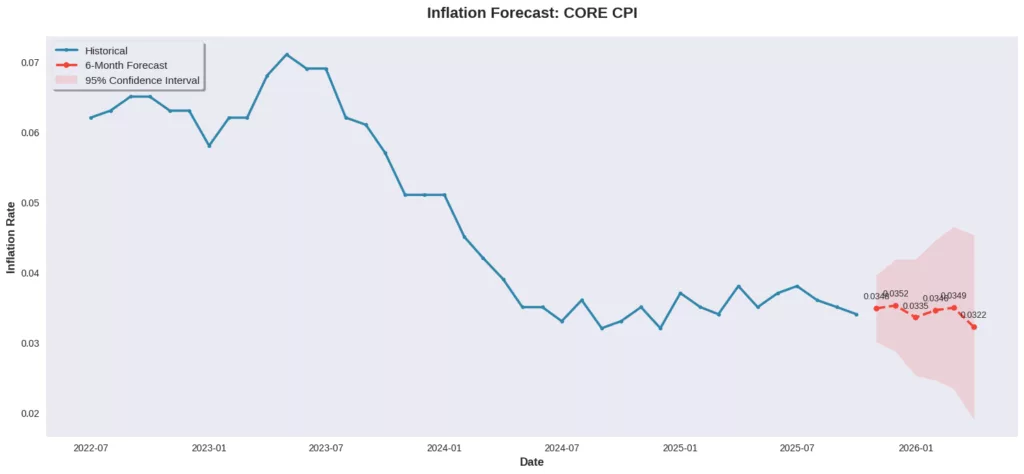

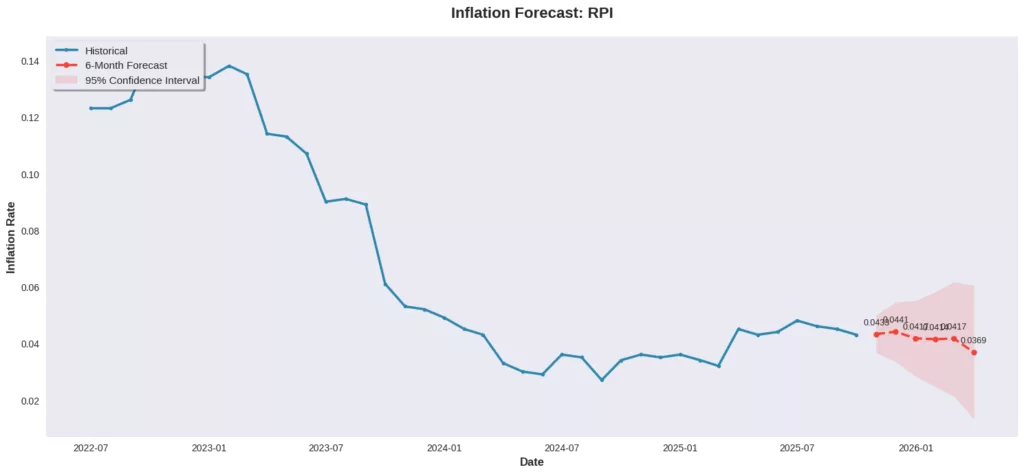

The Forecast: Inflation Will Cool, But Not to the 2% Target

Based on ARMA and SARMA economic models, the forecast for UK inflation is unambiguous. While price growth is expected to gradually decrease over the next six months, it will not converge to the official 2% target. The data indicate that inflation will likely remain stubbornly in a range between 3% and 3.5%. According to the analysis, the only scenario in which inflation would fall to 2% within the next year is a “sharp economic contraction”, a victory nobody wants. The implication is clear: policymakers and the public must abandon the hope of a swift return to the low-inflation environment of the past. We must prepare for a sustained period where prices grow faster than the official target, requiring a fundamental shift in strategy for both central banks and household finances.

A New Way to Think About the Economy

Our conventional understanding of inflation is dangerously outdated. The hard data show that current policies, with their myopic focus on managing aggregate demand and the labour market, are failing to address the real structural drivers: financial asset bubbles, generational price cycles, and persistent supply-side costs. The evidence is clear: our economic playbook is broken. The critical question is no longer if policymakers should change course, but whether they will do so before leading us into the next crisis.