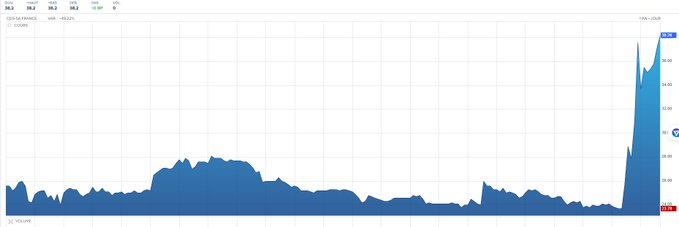

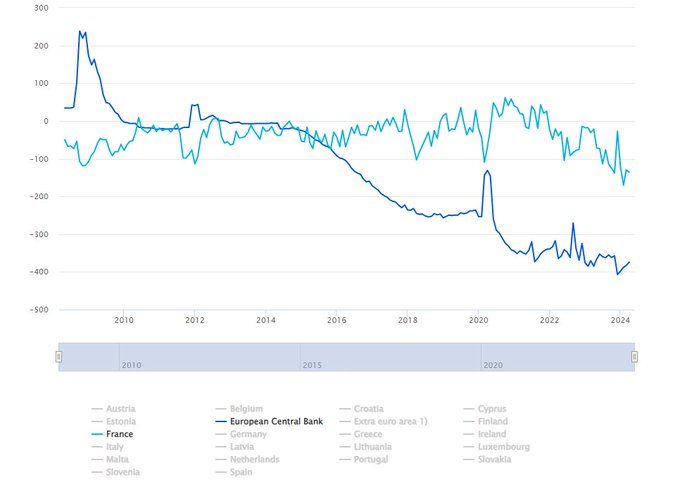

The Euro could be set to become much more volatile in the FX market, considering the interest rates differential with other G10 currencies and the structural idiosyncratic deficiencies in the Euro Area, considering the wider persistent Fiscal Deficits carried on by Italy with 144% debt/GDP and imbalances of many Euro Area countries, where indeed, France could spark a Sovereign Debt Crisis with widening spreads, considering the 110.6% Debt/GDP ratio, a budget deficit of 5.5%, but crucially France is set to become a net borrower in the Target 2 balance, these are the same factors that sparked the 2011/12 sovereign debt crisis.

The FX Euro volatility could and should become much higher, going forward, in the chart below of EUR/USD 1.0684 on a monthly timeframe, it’s possible to see, how the EUR/USD price trendline drifts below the ICH Cloud Span A/B, technical indicator of a bear trend, the pattern seems a clear double top pattern that could flush down to the 2021 lows of EUR/USD 0.95 with a Euro below parity to the USDollar.

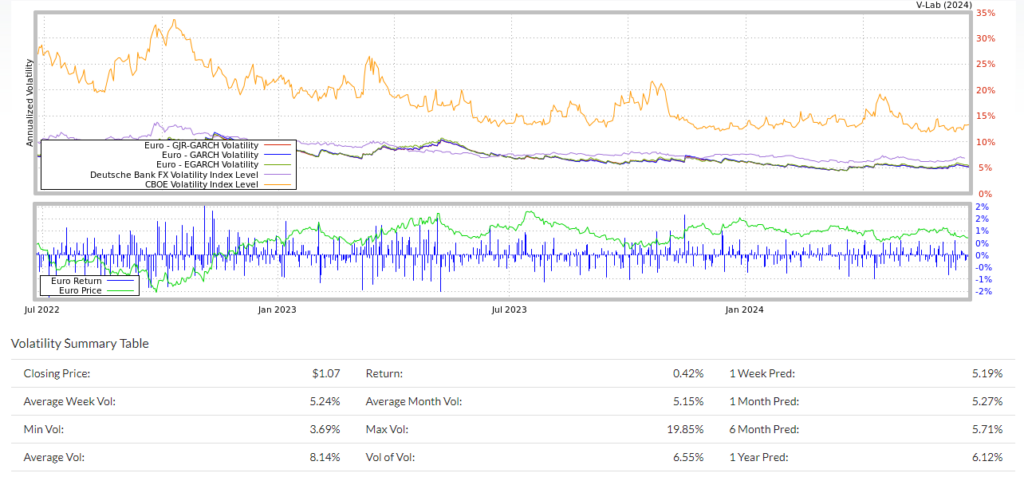

An initial analysis of historical Euro FX volatility suggests that the Euro may converge to higher average volatility levels of 8.14%, aligning more closely with the Deutsche Bank FX Vol index measure. This comparison highlights that FX exchange rate volatility is significantly lower and more contained than CBOE Equities Index Volatility.